U.S. Treasury and Fed Determined to Destroy Dollar and Force Savers to Spend: Investing in a Government Hoping for a U.S. Dollar Collapse.

- 18 Comment

Tuesday’s action by the Federal Reserve has placed us into the history books. The Fed cut the federal funds rate to an unprecedented 0.25% and gave a rather firm statement that they are prepared to keep the rate at this low level as long as the markets deem it necessary. When asked why they didn’t cut rates down to 0 a Fed official replied that it would help the credit markets run more smoothly. The markets don’t believe that. In fact, the markets have been trading near the zero percent mark for some time now.

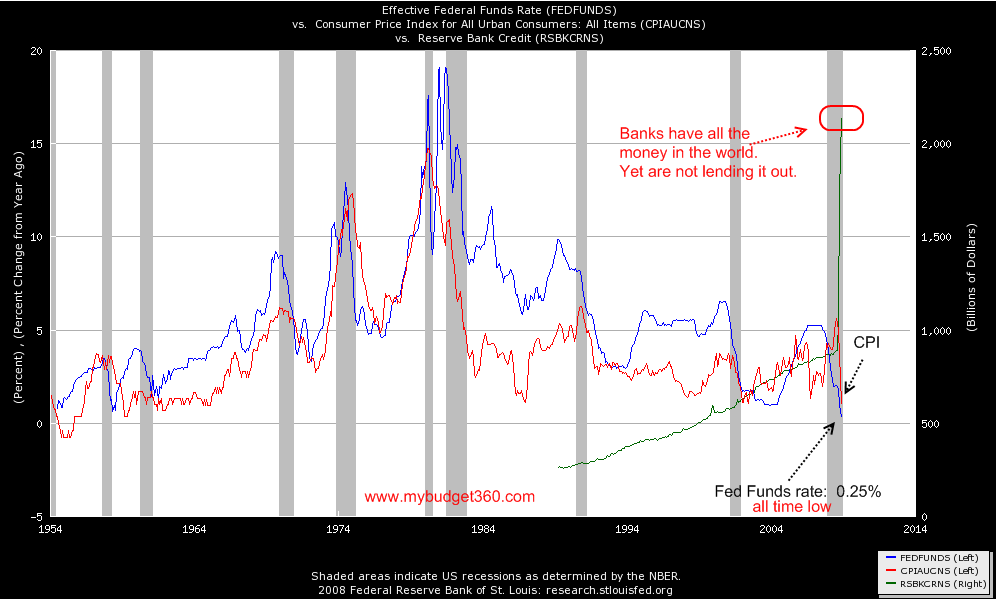

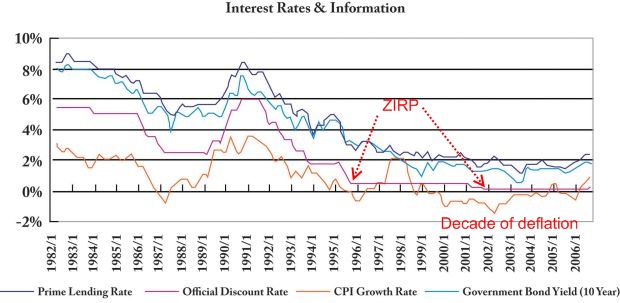

As the market volatility has increased causing 2008 to be one of the most volatile years on record, we are seeing some historical action occur. First, let us look at 3 key economic indicators:

*Click for sharper image

Let me try to walk you through a few things here. First, the federal funds rate is now sitting at a historic low. We are now seeing a zero interest rate policy regardless of what the Fed is saying. The fact the rate was left at 0.25 is merely symbolic. What the move signals is the Fed is basically done with monetary measures. It has no choice. It has reached the bottom of the barrel.

What led it to the bottom of the barrel is how quickly the red line on the chart above is shooting lower, consumer inflation. Some are trying to call it “dis-inflation” but let us be honest, this is deflation. This is scaring the Fed into doing unprecedented things. So why is this deflation? Let us count the ways:

(a)Â Housing market is imploding taking prices down

(b)Â Employment is skyrocketing keeping wages stagnant for many and wiping out income for others

(c) Stock markets are tanking across the globe. With nearly $50 trillion in global wealth lost in one year.

There is nothing remotely close to calling this inflation. In fact, the CPI released fell the most on a monthly basis in 61 years. In fact, this was off the charts since the BLS started keeping track of this data point in 1947. It dropped 1.7 percent in November. Compound that with the 1 percent drop in October and you can quickly see that we are quickly approaching a year over year percent drop on the CPI. The last time the CPI dropped on a year over year basis was in the early 1950s as you can see from the chart above.

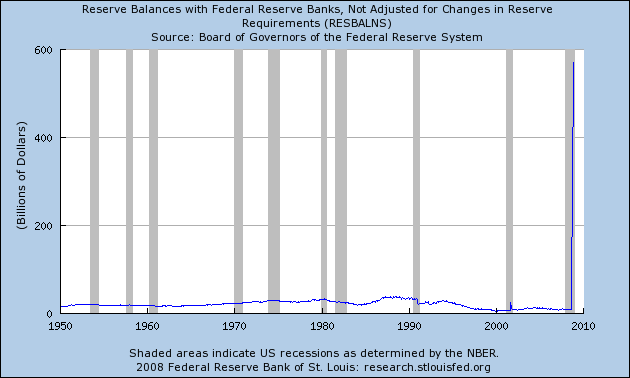

The other point on the chart is the reserve bank credit which is over $2.2 trillion. Now some may argue that this is inflationary. It is only inflationary if it makes its way into the hands of Joe and Susie public and that is not happening. How can we tell? Because when we look at reserve bank credit which includes much of the bailout funds, banks are pouring them into treasuries and sitting tight:

This is unprecedented. Banks are scared witless to lend because of the grim reality of all the losses they will face in subsequent quarters. In fact, most banks are simply gearing up for a long economic winter and bailout funds are being used as a cushion. The blame does fall with banks but what did one expect with the Treasury lending banks money and at the same time expecting banks to lend with stricter standards? It was a losing proposition from day one. Why? First, the massive credit boom of the last 30 years was dependent on a healthy employment base and lax credit. Now, we have the exact opposite. We have a quickly deteriorating employment picture and banks are expected to be more strict in lending money.

The only way credit will flow again as it once did is for someone to become the large non-prime lender. Wall Street and foreign banks took up that role gladly during this decade. Now, the only entity with enough power to fill that role is the government. The Federal Reserve in conjunction with the U.S. Treasury are attempting to become the biggest non-prime lender of all time. Consider that 0.25 a teaser rate for a future of economic trouble.

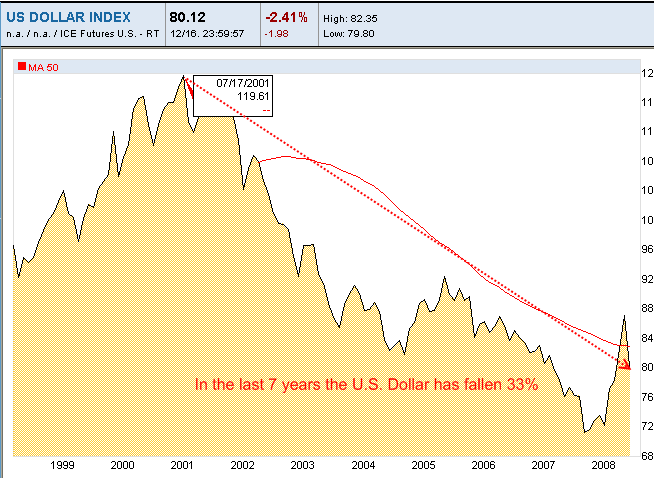

It sometimes helps to see what is being sacrificed here. The first major casualty is the U.S. Dollar which got pummeled by the Fed rate cut:

The U.S. Dollar has been in a steady decline. That is, until early summer of this year when it started a ferocious rally. What occurred near this time? A few things. Global decoupling was laid to rest and the oil bubble burst. Massive deleveraging led investors to a common resting spot. The U.S. Dollar. Keep in mind the one thing we are not hearing anyone talk about is a strong dollar policy. Why? Because it wouldn’t sound too good to the American public if the Fed stated that they were systematically trying to destroy the value of the U.S. Dollar on the global exchange markets. Why? Well, unfortunately the massive amount of debt which amounts to approximately $49 trillion in the U.S. is simply back breaking. The Fed is desperately going to do anything it can to bring back inflation even if it means an all out war on the U.S. Dollar. You need only look at the chart above to see what is happening.

Anyone that has traveled abroad realizes the destruction of the U.S. Dollar. Let us take a longer view of this and you will understand why:

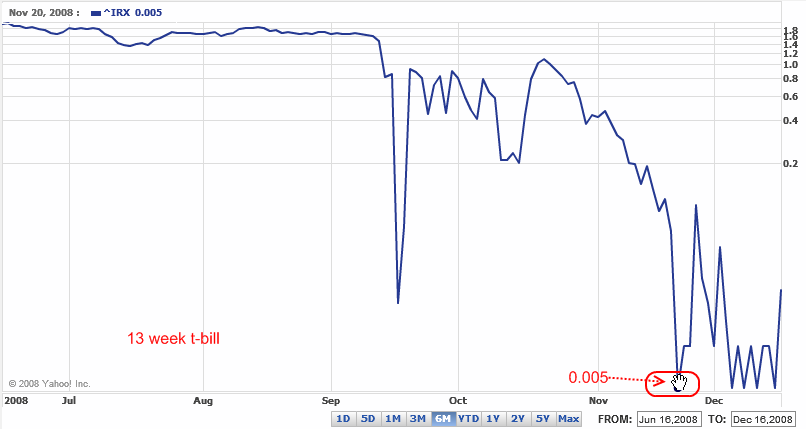

In the last 7 years the U.S. dollar has fallen a stunning 33 percent. In global terms we are steadily getting poorer and poorer and the Fed and U.S. Treasury are happy to oblige. You need to remember that it would be very easy for the Fed to strengthen the dollar. All they need to do is increase the fed funds rate to encourage saving. Yet the only people that are saving right now are foreigners and many are happy to invest at 0 percent rates of return:

Is this even good for our country? It depends if you enjoy a weak dollar that is systematically being attacked. The Fed is desperately trying to engineer inflation to get us out of our massive debt. Remember that in deflation debt is the worst possible thing to have. The reason for this is asset values are declining while the face value of the note remains the same. Housing is a perfect example. Say you bought a home for $500,000 and took out a $450,000 mortgage. The home is now worth $300,000. A current buyer purchase a similar home for $300,000 today and takes out a $250,000 note. You have a $450,000 mortgage still and the new buyer has a mortgage $200,000 cheaper than the one you have. Now multiply that over thousands of times. Deflation is to be avoided at all cost because it renders the Fed a wizard behind the curtain (at least that is what they hope to avoid).

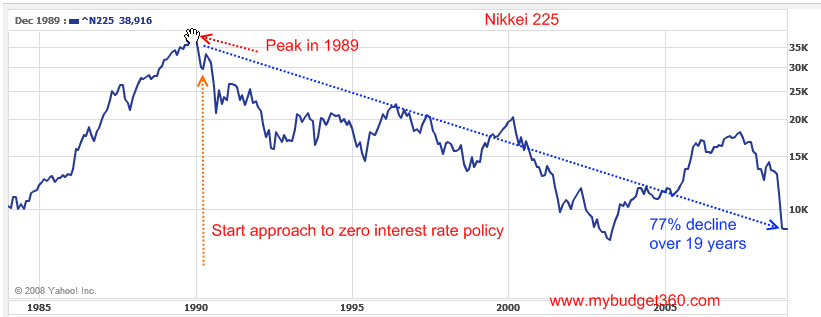

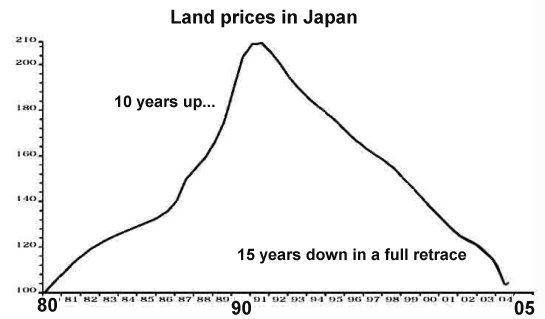

It may be worthwhile to take a look at Japan since they went down a similar path:

They followed a zero interest rate policy and injected billions into their banks after their real estate market bubble collapsed and their stock market burst. If you take a look at the chart above, the Bank of Japan systematically started cutting rates in the early 1990s and has held them low ever since. Nearly 2 decades after. How did this help their stock market and real estate market?

I remember when this argument was made in the initial days how quickly it was brushed off. We are not Japan echoed the argument. That is true. We are different in many ways. Yet we have similar circumstances especially in our financial markets. Let us outline at least the similarities and you judge for yourself:

(a)Â Massive unsustainable real estate bubble

(b)Â Lax lending standards

(c)Â Over building

(d)Â Massive stock market bubble

(e)Â Stock market and real estate bubbles burst together

(f)Â Japanese government injects liquidity into banks

(g)Â Bank of Japan cuts official discount rate to near zero

(h)Â Start of deflation

We’re playing out the same scenario above. Sure, Japan is different culturally and in many other ways but a through h above are essentially what we are living. That is simply a fact. We had a real estate bubble and stock market bubble burst together. We had horrifically bad lending standards. There was massive over building in real estate. Our government is now injecting capital into banks. Our Federal Reserve is approaching the zero interest rate policy. We are now seeing a taste of deflation.

The only ace in the hole is that the Fed is trying all these other creative instruments to get credit going again. You know what is the only thing that will work? The only way this will work is if the Fed and U.S. Treasury nationalize all banks and enforce lax lending standards and bring back the bubble days. That way, they can directly oversee how the funds are being disbursed. Otherwise, banks privy enough to get a cut of the bailout funds will sit comfortably looking for deals as banks not on the bailout list implode. Next year we know that we will be seeing massive fiscal stimulus and it is hard to say how the market is going to react to an aggressive Fed while the government becomes the number spender. We’ve never been down this road before.

Yet the major losers here are those who are prudent and savers. If you look at savings rates at your local banks, you are looking at another zero interest rate policy. The notion of dollar cost averaging into the stock market has gone out the window for probably a generation. If we were to go back to historical rates of 5 to 6 percent many savers would start storing money especially given the current economic shock. Yet we are doing the opposite. The Fed now is trying to make rates so low that banks will be forced to lend. Yet here is the kicker. A bank would rather have a 0 percent rate of return than a certain loss to a bad borrower.

I mourn for the U.S. Dollar primarily. It is a very tough time to be a saver with our current Fed and U.S. Treasury destined to annihilate our once mighty greenback.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!18 Comments on this post

Trackbacks

-

debt relief said:

I have similar (though not necessarily as thorough) explanations and examples. One person put it this way – the feds have not been able to service interest on past debt. The bailout money will make it impossible to service. Something has to give. One person I read suggests the bailout will prop things up for a little while. But they predict a collapse in a year to year and a half. Scary stuff.

December 17th, 2008 at 3:55 pm -

andy said:

A very thorough analysis. I think saving the economy, rather than the US dollar is more importnant now. Unfortunately America is not a nation of savers, and credit/debt is why we have the problem now. US dollar should still be strong for the next few years thanks to its safe haven status. Long term though you must have international exposure.

December 17th, 2008 at 8:09 pm -

Bill M said:

Short term this will be very good for people to pay off their debts as it will become more affordable to do so… My HELOC is already down to 4% as of last month, with the 3/4 I’ll be paying 3.25% on my HELOC which is good short term. Long term everyone should have their money on a well balanced portfolio of index-based ETFs. Interest rate this low also is irrelevant without inflation, usually the higher the interest rate, usually higher the inflation.

December 18th, 2008 at 2:45 pm -

Bill said:

“US dollar should still be strong for the next few years thanks to its safe haven status”,yes,sure.

And-what-happens-when-it-no-longer-has-that-status?December 18th, 2008 at 8:06 pm -

Mike D said:

Doesn’t it seem evident to everyone that we are being manipulated into a more socialistic government. With Bush we had a Constitution that he ignored and now we have a black Democrat from the other side of the fence who will lower our standard of living even more with increased government and spending. Our leaders seem to like the idea of allowing our country to be bought up by foreign interests who had nothing to do with making it the greatest, strongest, and freest Nation in the world. We have become a disposable, here today, gone tomorrow,society. All at the expense of middle class families trying to increase what they and their fathers and forefathers accumulated and built. There must be some underlying cause why our citizens do not revolt against this. It is almost like people are being manipulated to feel hopeless and powerless over this. Is this the end of America as we know it?

December 19th, 2008 at 5:56 pm -

faanunu said:

It will be the certain end of the US if we don’t attempt to save the Constitution… there is no promise that our country (as it is today) will survive but those of us who want to remain freemen will have a choice.

“During the next decade, the American people will become poorer & less free. While they become more dependent on the government for economic security.”

“Price inflation, with a major economic downturn, will decimate U.S. Federal Government finances, with exploding deficits and uncontrolled spending.”

“The Congress and the President will shift radically toward expanding the size and scope of the Federal Government. This will satisfy both the liberals and the conservatives.”

“Major moves will be made by China, India, Russia and Pakistan in Central Asia to take advantage of the Chaos for the purpose of grabbing land, resources and strategic advantages sought after for years.”

“Policy changes could prevent all of the previous predictions from occurring. Unfortunately, that will not occur. In due course, the Constitution will continue to be steadily undermined and the american republic further weakened” Ron Paul (April 26th 2002)What happens now is up to us…

Chile had a brutal dictator Pinochet, he was notorious for his regimes brutality and it’s ability to make people disappear. He gained power through the actions of the CIA (its debated whether it was purposely or “blowback†of its actions). Pinochet held “elections†and always won. I have seen how people can win their freedom and take control of their government. There was no bloody revolution or revolt in Chile. There was no secret CIA movement. The Chileans persisted in an outcry for fair and honest elections. Pinochet agreed because partly he believed people loved him and that they also feared him. There was much fear among Chileans of retaliation when he would lose. There was talk of a possible civil war because everyone knew the dictator would not win if people’s vote truly counted. The people had the courage to vote their conscience to elect a President. There was a real fear that the dictator would not respect it and kill people but they had the courage to stand up. Complete freedom wasn’t won over night but gradually because of their persistence in their outcry for freedom. Pinochet gave up the Presidency and eventually the military and fled the country.

December 21st, 2008 at 3:57 am -

JJ said:

People are too stupid to realize anything that is going on.

December 21st, 2008 at 7:21 pm -

Johnny said:

First US will experience deflation. The FED 0% interest rate policy will not prevent it. Why have your dollars in an unsafe bank at zero interest? Many people will pull out there dollars from the bank and for every dollar they pull out of the bank, the bank has to reduce it’s credit with 20 dollars. This is starting to happen now.

The idea that FED will take controll over all banks and lend money for 0% to everybody is interesting and everybody will lend and pay off there old interest bearing debt and then the banks will make no money at all at 0% interest rate and go bankrupt.

When this deflation spiral is over and savings are good and credit starts to become available again and the psychology of people change from negative to positive inflation will start again, but it will take time. That is my understanding anyway.

December 22nd, 2008 at 3:54 am -

Shannon Melton said:

Ahlgren Predicts Dollar Failure and Collapse of U.S. Treasuries Bubble

Markets and Investing

December 27, 2008 — 9:51 AMIn his award-winning, critically acclaimed novel Discipline (Greenleaf Book Group Press, 2007), Paco Ahlgren predicts a Soviet-style breakup of the United States, resulting from the simultaneous collapse of equity markets, the failure of the dollar, and its ultimate replacement by competing private global currencies.

I read a pre-release copy of Discipline in late 2006, and I enjoyed many aspects of the book — most notably the way the author subtly weaves everything from subatomic physics, to drug-abuse, to finance, to eastern philosophy into a heart-pounding thriller. But I also remember chuckling at the preposterousness of the failure of the dollar and the demise of the Unites States.

I’m not laughing anymore.

Mr. Ahlgren is a senior analyst at The Copernican, LLC, and counts himself as a proud proponent of the “Austrian School” of economics. Recently, I was able to catch up with him in Austin, Texas for a conversation about his book, and the chilling events he predicted which seem to be unfolding around us.

TB: Although you published Discipline in mid-2007, you actually finished the first draft in early 2001, is that right?

PA: Yes.

TB: And did that version contain the dollar-failure scenario for which Discipline has gained so much attention lately?

PA: It did.

TB: But the book is fiction. Did you know your predictions were going to be so accurate?

PA: I’ve been elbow-deep in economics for two decades now, and if you read the work of Hayek, Mises, or Murray Rothbard, among so many others — and you really get it — it’s hard not to see how the dollar is in a long-term decay. The United States is essentially broke.

TB: So you knew, when you wrote it, that you were seeing the future. That is, after all, a big part of Discipline…

PA: [Laughs] Look, first of all, the dollar hasn’t totally failed yet. I mean, we have a long way to go — this is a long-term process. Maybe the Fed and the Treasury can work some magic and fix it all, like they have in the past, but I obviously don’t think so this time.

But the other important part of this is that Discipline is supposed to be a thriller that introduces people to some fairly complex topics they might otherwise ignore. It’s supposed to educate them to the possibility that their government is corrupt, and that their currency is almost certainly headed for failure. I could have written a non-fiction piece, but Discipline is for the masses. It’s supposed to be something that reveals to as many people as possible what is going on. So the “thriller” aspect shouldn’t be compared to the predictive, philosophical/economic aspect. Discipline, as a story, is just a vehicle.

TB: And are people getting that?

PA: I think so. Unfortunately, I’m also getting some pretty crazy feedback from the fringe — people who believe that the characters are real.

TB: Are they?

PA: [Smiles]

TB: The dollar had a pretty good rally for about five or six months, the last half of 2008. Were you worried that you might have made a mistake about its direction?

PA: No. The recent rally in the dollar — which I believe has turned, by the way — was caused by massive deleveraging. I mean, every single asset-class collapsed this year as companies and individuals scrambled to reduce debt and raise cash. The only thing that didn’t seem to go down was Treasuries. People were parking their dollars, looking for safety — which is so counter-intuitive if you think about it.

TB: Treasuries have had quite a year.

PA: Sure, but the party’s over. I know a lot of people who got burned shorting them this year. I even thought about shorting them in the spring, but I didn’t. Despite the inflationary environment earlier this year, I had a funny feeling everything was going to fall apart. I also knew the Fed would mislabel the collapse as deflationary, and that they’d drop their target, although I didn’t think we’d go to zero. So I held out.

TB: Did you eventually short Treasuries?

PA: After the last Fed move, I did.

TB: Did you use futures, or ETFs?

PA: I used TBT — the Proshares ultra short ETF. It’s double-leveraged, and I want a lot of bang. I just hope the timing is right.

TB: As crazy as it sounds, some people are actually arguing that there is some more upside in the long end of the curve — especially if the Fed keeps buying.

PA: I know. Believe me, I’ve seen the arguments. The future looks absolutely bleak. Short term rates went negative! How much more upside can there possibly be in Treasuries — even on the long end of the curve? This bubble is more ridiculous than the oil bubble; at least oil isn’t bound by zero interest rates! I mean, I was looking at oil at about $135 and thinking, “I should be shorting the hell out of this.” But there was this little voice inside my head saying, “The upside is infinite, at least theoretically.”

But the upside to Treasuries is not unlimited. I guess you could make the argument that, as the long end of the yield curve gets lower, its relationship to price is asymptotic, but that’s just academic. Even if the Fed does start buying the long end, how are they going to sustain the policy? Nobody has the firepower to drive long-term yields much lower. The Fed is talking about it, but I just think they’re trying to get a reaction. I don’t think they’re really going to do it. I think they’re much more interested in targeting mortgage-backed securities — to tackle the housing crisis directly — because the wide belief is that there can be no turnaround without stabilizing housing.

TB: Still, the historical low yield for the 10-year is something like 1.5%. Using that as a barometer, it could still go a lot lower, right?

PA: I don’t think so, because our situation is so different now than it was when the yield went that low. Back then, relatively few foreigners held our debt.

There are so many factors at play here. Let’s say the Fed makes good on its threat to buy the long end, to hold rates steady at these levels — or even bring them down further. How are they going to do that? They’re going to have to print dollars, and that’s just inflationary. I don’t care what kind of spin the Keynesians try to put on it. It’s inflationary. We’re getting into a situation where our government is printing currency and then loaning it to itself. It’s just laughable.

A lot of the TARP money went to institutions that dumped them into Treasuries, but how long will that last? How long are managers going to accept these absurd rates of return from a bankrupt government? And how long are they going to perceive Treasuries as safe? The U.S. has pledged $8.5 trillion to bailouts — more than all other programs and wars in our history, in real dollars, combined! We’ve gone from being the biggest creditor nation to the biggest debtor nation on earth. We’re consuming everything, and we’re not making anything! We’re a nation of spoiled rich kids who sit around and watch television all day. How long do you think the rest of the world is going to continue to lend us money?

TB: A lot of people would say that sounds almost conspiratorial!

PA: [Laughs]. Yeah, well I might have said that a year ago too — about everything from the failure of Bear Stearns to Lehman Brothers, to the nationalization of AIG, Indymac, and Freddie and Fannie. By now though, it’s not conspiratorial. It’s just math.

The government is printing dollars, and it’s nationalizing everything. And try to remember that I’m not getting my research from fringe websites whose members bury guns and potable water in their back yards. I’m getting my information from places like Bill Gross over at PIMCO, Bloomberg, CNBC, and even the Fed and the Treasury. This stuff is really happening, and some very smart people are noticing. Credit markets are frozen. Investment real estate is dead. Consumers can’t consume anymore. Where’s the long-term growth going to come from?

Look, the Chinese are sitting on $1.6 trillion in Treasuries. Do you think they’re going to be willing to lend to us indefinitely, considering how irresponsible we’ve been with our money? And especially at these rates? On top of all that, Treasury prices are sitting at historical highs. It wouldn’t surprise me if the Chinese started selling our debt to fund their own initiatives, like the $600 billion stimulus they announced not long ago.

TB: So the Fed may be buying Treasuries, and the Chinese are going to be selling them?

PA: Assuming the Fed is that stupid, and they really do attack the long end of the curve, I could actually see something like that happen — if it isn’t happening already. If I was in the Chinese finance ministry, I wouldn’t be able to find much downside to selling Treasuries at these peak historical levels. It would give them cash, and essentially set them up as the world’s strongest economy — if not now, then very soon.

In the meantime, the Fed won’t be able to hold the long end of the yield curve down. They’ll be printing money, causing inflation, and the world will be getting hit with the simultaneous sale of foreign holdings of Treasuries, along with a massive flood of new Treasuries from the U.S. government, which needs to borrow as much as possible to pay for all the programs it’s planning. It’s such a mess.

And it’s not just the Chinese. It’s the Saudis, and the Japanese, and a whole list of people who probably won’t be buying new Treasuries — and may very well dump the ones they already have.

TB: But if the Chinese help with the destruction of the U.S. economy by selling Treasuries, aren’t they just shooting themselves in the foot? Don’t they need to export to us?

PA: I don’t think so — not so much anymore. The Chinese are getting a very strong middle-class. They are likely getting to the point where they can consume a lot of what they make, and that’s a strong place to be. I’m not saying it isn’t going to be hard for them too. Everyone’s going to suffer. But I think the Chinese selling Treasuries now would mitigate their pain.

It makes a lot of sense, actually. To be honest, I can’t think of a reason why they wouldn’t. There may be a reason, but I haven’t thought of it. This situation reminds me of the transfer of economic power from the British Empire to the United states a century ago. Now we’re losing it to China. They have a strong work ethic, tons of resources, an inexhaustible labor supply. Why do they need us, anymore than we needed the failing British Empire when we took the reins?

TB: Okay, now that we’re in the midst of the collapse — that is, the thing you predicted — what do you see going forward?

PA: A lot of people are saying things like, “If Obama cuts spending, and reels in the deficit, and cuts taxes, we can get back on track.” I don’t even bother thinking about stuff like that, because there isn’t one person in Washington — except Ron Paul — who wants to cut spending right now. In my mind, we’re going down this road no matter what. The American people have borrowed insanely and used the proceeds to consume massively. We’re going to have to go through a lot of pain, and when it’s over, we’ll see what happens.

TB: And what do you think might happen?

PA: It’s hard to say. Maybe people will demand a return to sound money and rugged individualism, but I tend to doubt it. Spoiled brats look for handouts and paternalism, and politicians facilitate that process. Washington will keep promising more and more, and we’ll probably move ever-closer to a completely socialist state. At some point, Texas, or New Hampshire, or somebody else will say enough is enough and get out.

TB: Like in your book.

PA: Yep.

TB: And the United States response?

PA: I don’t know. This isn’t 1861. Can people from Iowa point guns at people from Texas and pull the trigger? That’s going to be an interesting moment. I hope it doesn’t come to that, but unless something changes, it just can’t last. The Roman Empire crumbled because of fiscal irresponsibility. So did the British Empire. So did the Soviets. People think we’re immune, but just take a look around you.

And there are other things to think about. Texas could probably aim a nuke at Washington, D.C. pretty easily. The thought terrifies me, but it would almost certainly result in a stalemate. Also, the predication here is that the U.S. is totally broke, and already fighting several wars. Will it be able to fund another war against separatists? Probably not. And even if they try, it won’t be popular at all.

And, of course, I can’t think of anyone on earth who would relish fighting a war against Texans. [Laughs]

TB: Okay, even if it’s as bad as you say, why can’t we just spend our way out of it, just like we did during the Great Depression?

PA: For several reasons. First, we got out of the Depression by issuing debt, which was bad enough. But this time, we’re going into it with massive debt. Also, during the Depression, our debt was absorbed domestically, almost exclusively. Today, our debt is held by foreigners to a very large extent, and our ability to get out of this mess will be dictated not only by how much they continue to lend to us — which I believe won’t be much — but also by what they ultimately do with the debt they currently hold. I think they’re going to sell it, driving interest rates higher, and killing the dollar.

No matter what happens, inflation is the logical conclusion. And I can tell you that the United States is not going to be able to borrow domestically, exclusively. That’s just not in the cards, and I hope nobody is delusional enough to think it is.

Look, in order to get out of the inflation caused the last time we tried this — in the ’70s and ’80s — we had to drive interest rates above 20%. We were lucky it worked. How many times can we use that trick before it doesn’t work? Think about the Weimar Republic or any of the countless other nations that have experienced hyper-inflation.

Our biggest enemy right now is our inability to accept our vulnerability. We believe we are entitled to everything, without producing much of anything. We’re fighting multiple wars around the globe. We’re hated — or at best, not respected — by a large part of the globe. Social Security is bankrupt, along with Medicare and Medicaid. The government has its fingers in everything. Look at our debt, our GDP, and our trade deficit. No, it’s very different this time.

TB: So what are you doing to prepare?

PA: Well, like I said, I’m short Treasuries. I’m also watching commodity prices carefully — especially oil.

TB: Why oil?

PA: I’m actually bullish on oil if it pulls back to $20 or $25. The problem with oil is that, unlike gold, it has such a huge practical aspect to it. Gold is nothing more than a store of value. It has almost no industrial application, so its supply isn’t affected as much, cyclically. Oil, however, is tied directly to economic activity, so I think we’re going to need to see a little bit of a turnaround before it increases in price. But I think it will go higher.

TB: To previous levels?

PA: I don’t think so — not for a long time. That had nothing to do with supply and demand. That was a mania. But if it gets to $25, it’s going to be oversold, and I think it will have a lot of upside at that point.

TB: So what about gold?

PA: I like it, but it’s all about timing right now, and I don’t think gold is oversold. Of course it didn’t make a bubble like oil did, so its retreat wasn’t as pronounced. Shorting Treasuries is a no-brainer, and probably buying oil and gold right now would be smart. But my biggest concern is timing. What’s the saying? “Markets can stay irrational a lot longer than you can stay solvent?” Actually, I think Keynes said that. I guess he was good for something. [Laughs]

TB: That brings up a good point. A lot of people are talking about how the Fed, through this new use of so-called quantitative easing, could hold down rates for an extremely long time. One very scary example is Japan, whose interest rates have been almost zero for many years. Could that happen here?

PA: I don’t think so. First of all, Japan was using QE at a time when people could borrow in Japan, and reinvest elsewhere — like the U.S. — at much higher rates, with almost no risk. So that put a lot of pressure on rates in Japan, and it caused massive mal-investment in the rest of the world. In fact, I’d say that Japan — this little island that has been printing incomprehensible amounts of currency — has a great deal of culpability for the bubble that got us where we are now. I have a lot of doubts about their future too.

But I’ve already made the case that I don’t believe the Fed and Treasury will be able to maintain this shell game for long. Japan was a creditor nation with a huge savings rate. People had no problem lending to them — even though their credit rating slipped.

The U.S., on the other hand, has no savings at all to speak of. If the Fed’s objective is to create inflation — and by its own admission, that’s exactly what it intends to do — I don’t think they’re going to have any trouble at all, unlike Japan. In fact, I think it’s imminent, it’s coming soon, and when it does come, it’s going to be hell to stop — if it can be stopped at all.

Treasuries are going to collapse, and anyone stupid enough to have bought the 10-year, or even worse, the 30-year, at recent levels is going to see massive capital losses. It’s going to cause absurd liquidations, and yields are going to skyrocket. It’s going to happen fast, and it’s going to be just as scary as the collapse in equities we just went through.

Probably the most frightening aspect of it, though, is that so many people pulled money out of stocks and put them into Treasuries for safety. Now they’re going to lose most of that too. It’s going to damage U.S. credibility immensely. I don’t see how the government will ever get it back.

TB: You’ve mentioned Rothbard, Mises, and Hayek. Are there any contemporary figures you’re paying attention to right now?

PA: Oh yes. I absolutely love Peter Schiff. I think he’s brilliant, and his track record speaks for itself. I also Love Jimmy Rodgers. I’ve been following his career for years. I constantly scour YouTube for any interviews I can find from these two.

Jimmy Rodgers cracks me up. Some of the things he says are priceless. I’d give anything to follow his lead and move to Singapore, but unfortunately circumstances are going to keep me in Texas for a while.

TB: Mr. Ahlgren, thank you very much for your time. It has been a pleasure speaking with you.

PA: Likewise, and thank you.

January 1st, 2009 at 5:26 pm -

alf lan don said:

JBR/soros says 1/9 get out of pounds sterling. . . but

hold what currency?January 21st, 2009 at 2:53 pm -

Surviving A Recession said:

i believe costs have become way out of line with reality and have been for years. Although deflation may be bad for the economy, and even worse for us because of our debt load, i think it is bitter medication that we will be stuck with until expenses and income reallign.

February 24th, 2009 at 1:40 pm -

Rom said:

This did not happen by accident….all of our major politicians and heads of all Gvt. Depts. going back 7 Prersidential Administrations are filled with the bankster elite. Their affiliations are well known. This stretches to both sides of the political fence, all the way down to the local level in larger cities. The top three affiliations are the Bilderberger Group, Council of Foriegn Relations and the Trilateral Commission. (Also Gatt8). I know what your thinking, but look at the numbers. 98% of Obama’s cabinet post belong to these three groups, even the Kansas Govenor he just appointed. Same level of numbers with Both Bush administrations (Sr. and Jr.)It is a strange coinincidence that since 911 all of this economic upheaval has been “allowed” to happen. Gaithner and Bernake both belong. All of Washington are following their Bankster masters orders. Where is the logic on why has all this been allowed to happen. All of our mass-media is owned and run by the most prominent elitist within these groups. Ask yourself one question, why would they go through this much trouble (one world currency and system), or is it all a mere coinincedence and I’m a nutcase. Just seems too eloquent and sophisticated to me, economically speaking of course.

May 5th, 2009 at 1:40 am -

Ed said:

I think it is too late to save the dollar now. Just as taxpayers bailed the failing financial institutions out and paid the price via higher interest rates, they will once again pay the price in the form of a hidden tax called INFLATION.

November 25th, 2009 at 8:53 am -

Barry said:

By the end of 2010 the US Banking system will have collapsed. My understanding is that once that happens, the US banking infrastructure (including branches and buildings) will be taken over by Chinese banks.

May 31st, 2010 at 2:46 am -

Joe in JT said:

To simplify the U.S. financial system and the problems we are having you can say the following.

“You can’t have a country just print money without the money being backed by something of value, like gold or silver.”

Maybe for a while, honest men print off the money. But in the end, greed takes over and to many people are in the kitchen trying to cook the soup.

August 1st, 2010 at 5:24 pm -

Deserwest said:

The gold standard has been tried over and over again, it too fails each time. Why? Because goverments have learned that it too can be influenced by interest rate policy. The great depression of the 1920’s – 1930’s was made worse by trying to support the gold backed currency. People forget, we were under the gold standard at the outset of the depression.

The scenario we have right now is this … the goverment prints the money and routes to the banks, who buy goverment debt, to fund the goverment… repeat cycle.

Following the money trail leads us right back to the goverment.

One does not need a degree in economics (any school of thought) to grasp the simple answer … STOP THE SPENDING that is in excess of a balanced budget.

September 17th, 2010 at 12:24 pm -

therooster said:

Of course the dollar is being destroyed. What folks have yet to wake up to (99.999%) is that the dollar’s ultimate role is not that of a currency at all ….never was. It’s ultimate role is to act as a real-time measure for gold-money where the dollar bridges the divide between items priced in a fiat currency , yet are paid for in gold weight. By inflating the currency supply, the elite are “carrying the stick” to move people over to gold , one person at a time. It must be a market driven process because in any migration , it’s absolutely imperative that neither system crashes, the old and/or the new.

Real-time gold is here and now and being used on a daily basis. Wake up ! Before gold could be a very viable , very liquid form of money, two things had to take place. Gold had to flloat in trade value (real-time) because of its limited supply fundamentals. This is why the FIXED peg had to be severed, ultimately. Once that took place, a simple method of “splitting the enhanced value of gold weight” had to be developed for the sake of liquidity. We’ve had that market solution since the advent of gold backed digital currency (1996) where the actual ownership title of bullion acts as the currency. Debt-free store of value has married with instant global liquidity in the twinkling of an eye. How on earth could anyone ask any more of a currency ? Wake up and never forget the gifts of the Magi !

May 26th, 2011 at 3:32 pm -

Brandon said:

The economy is in shambles? I can’t believe the founding fathers didn’t plan for this! Ignorant men, all of them. Oh… wait… never mind:

“The central bank is an institution of the most deadly hostility existing against the Principles and form of our Constitution. I am an Enemy to all banks discounting bills or notes for anything but Coin. If the American People allow private banks to control the issuance of their currency, first by inflation and then by deflation, the banks and corporations that will grow up around them will deprive the People of all their Property until their Children will wake up homeless on the continent their Fathers conquered.”

-Thomas Jefferson“Banking establishments are more dangerous than standing armies.”

-Thomas JeffersonOctober 28th, 2011 at 2:12 am