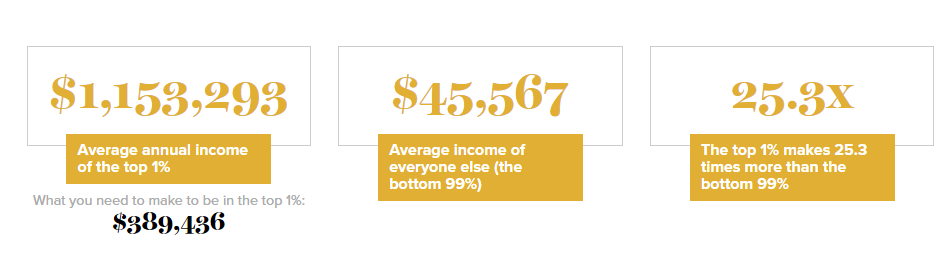

The math on income inequality: Average annual income of the top 1% is $1,153,293 while that of the bottom 99% is $45,567.

- 3 Comment

Part of the challenge with distorted income distributions is that it hollows out the middle class. The middle class in the United States is now a minority. We have more people making higher incomes and more people making way less and this group is growing much faster. Our economy has taken a bimodal distribution with extremes on both sides. We have a record number of people on food stamps but also a record number of higher income households. The only problem is that the low range of the ladder is growing much faster than that at the top. For every person that makes it into the upper income brackets you have three that fall out of the middle class and into the low income wage trap. Part of the political anger we are seeing in the US and other parts of Europe is that the elites are simply ignoring the needs of the masses. In many cases this purposeful ignorance is because their wealth is built on keeping many stuck on a perpetual hamster wheel where productivity gains only go to a small section of society.

The math on income inequality

There was a time when extreme wealth inequality led to eras like the Gilded Age. While we don’t have the soup lines of the Great Depression, we have other challenges that accompany mass income inequality including high housing costs, rising college tuition, and being one medical emergency away from bankruptcy. These are all challenges that come when you have extreme wealth inequality.

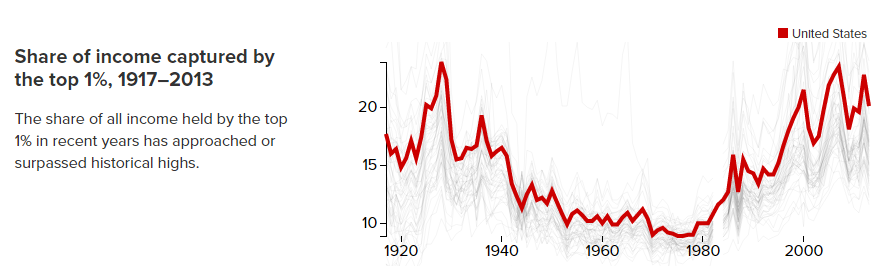

First, how unbalanced are we?

Source:Â EPI

The current level of inequality rivals that of the years leading up to the Great Depression. It is of course no coincidence that during the glory days of the US middle class that income inequality was less extreme meaning the middle class actually had a larger share of total income earned. That is no longer the case.

It is interesting to hear the media continually harp on the notion that $250,000 a year is somehow middle class. This is a lie. The median US household income is around $52,000. Someone making $250,000 a year puts them in the top 2 to 5 percent of all income earners. In fact, let us look at the figures even more closely:

To be in the top 1% you need to make $389,436. The average annual income of the top 1% is $1,153,293 while the average income of those in the bottom 99% is $45,567.Â

These are interesting figures. It also highlights how distorted the media’s view is on income since most in large TV networks essentially represent the connected class. They live in an echo chamber bubble.

There is obviously going to be income inequality in any market system. That is understood. But some of this gap is being brought on by a modern day plutocracy that is simply rigging the system in their benefit. One obvious way is the housing market. Homeownership, the traditional means of most families building their wealth is now becoming harder to do so because many big banks and investors have crowded out regular families who are unable to afford inflated prices. Each year this trend goes on is a year where average families are not building equity. This is also not “free market†based since the bailouts largely have helped big banks and investors while working class families have seen a shrinking idle class. A decade later, the facts are clearly showing the end result.

This is where the inequality argument takes a path down cognitive dissonance. Many of the banks that had massive handouts like to believe they are rugged free market individualist that can stand on their own two feet yet they are the biggest recipients of political and corporate welfare. While receiving large sums of money, they rail against the poor for not doing enough or for not working hard enough. As if taking in zero percent interest loans and finding something to buy with a slightly higher yield is difficult. Building a computing OS is hard. Finding new treatments for cancer is hard. Trying to make an electric car with style is hard. Making rockets is hard. Taking handouts from the government at zero percent and raiding single family homes in the market and collecting rents is not hard.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! Â

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!  3 Comments on this post

Trackbacks

-

Mike said:

Redistribute the wealth! Seize the 1%’s wealth and means of production and give it to the proletariat! We deserve it because we exist 🙂

July 1st, 2016 at 4:15 pm -

daniel de said:

Send updates on Wages and Medium and Median Health Care Costs for Individual and Families of 4 in America.

Thank You

August 24th, 2016 at 10:41 am -

Alissa said:

I guess you saw a Trump victory coming.

November 27th, 2016 at 5:49 pm