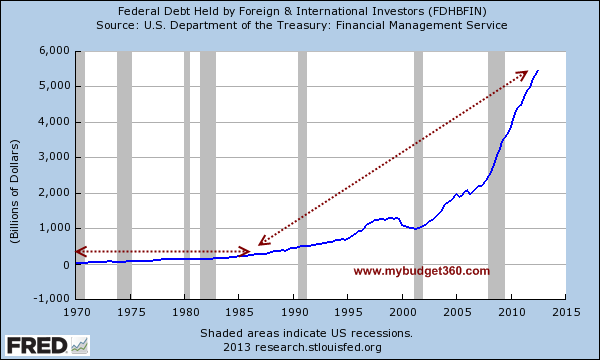

Crossing the debt Rubicon. Does debt even matter? Over $5 trillion in Federal debt now held by international and foreign investors.

- 2 Comment

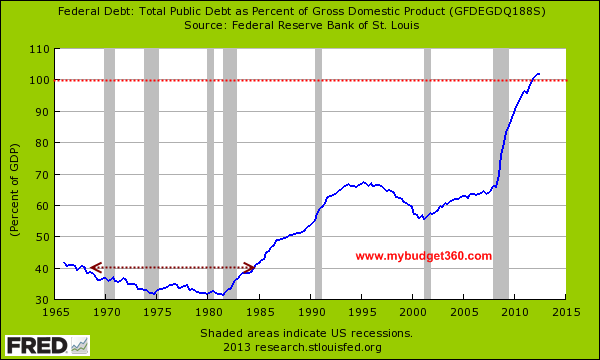

In most economic literature there seems to be a tipping point at which a nation enters a precarious state in which too much debt has been taken on. A typical point occurs when a country hits a point where annual GDP is surpassed by total outstanding debt. We recently crossed that threshold. Another long-term trend we are living with is depending on the lending and willingness of international investors to put their money into the US. Today over $5 trillion of Federal debt is now held by international investors. In essence, we need their money to keep going at our current rate. While the economic contraction has put the albatross of austerity on the necks of most households, banks and the government continue to spend as they once did. Speculation is rampant again. If you listen to some you would think that debt simply does not matter anymore. If that were the case, we wouldn’t be jumping from one crisis to another dealing with our level of obligations. At a certain point there is no more can kicking.

The financial Rubicon

Spending more than we earn is actually a modern thing as a nation:

From the 1960s to the early 1980s GDP-t- debt hovered around a 40 percent ratio. That is, if we had a GDP of $100 we would have a debt of $40. All of that started changing in the 1980s when deficits supposedly didn’t matter. Even here, we plateaued in the high 60 percent range all the way into the 2000s. This is where you see the major shift in attitude towards debt.

It is interesting to examine the first chart in context to how much debt is being financed by international investors. We also see a big correlation here. Starting in the 2000s we saw our Federal debt held by foreign investors jump from $1 trillion to now it being well over $5 trillion:

The trend is unmistakable and we continue spending more than we earn. If you look back at GDP, a big part of the GDP gap brought on by the deep financial crisis has largely been made up by government spending. But not in the traditional sense of a growing economy in the private sector. Most of this money was given to banks to essentially fire up other financial bubbles. We are seeing bubbles in higher education and now once again with real estate.

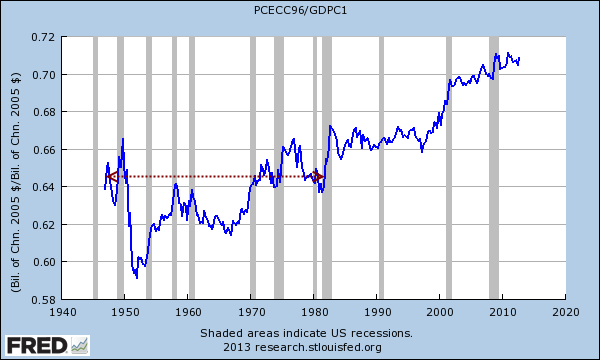

The government feels the need to spend more than it earns because it realizes that households simply cannot fill the current gap based on current household incomes. Consumption is still a big part of our economy:

Consumption still makes up over 70 percent of our economic growth. So the austerity on households is being made up by giant spending from banks and the government. Yet how much of this has leaked down to regular households? Not much.

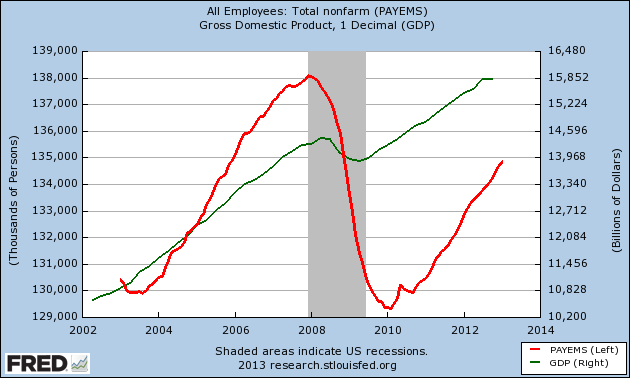

If you really want to put this in perspective, take a look at GDP growth versus the number of Americans employed:

GDP itself is at its highest level yet we are doing it with 4 million less American workers. It is no surprise that the top 1 percent have captured 121 percent of all gains since the recession ended and the rest have seen incomes decline when adjusted for inflation. Why is that? At the core, nothing has really changed and our government is largely controlled by big financial interests. Congress has the highest number of millionaires so they have a tough time relating to the typical American worker that makes $25,000 a year.

In the end it appears, the solution is more of the same. Continue to spend more than we bring in but history has been rather clear in terms of what occurs to nations that cross this debt based Rubicon. It is also clear that the impacts are already being felt by working and middle class Americans with the standard of living falling and sticking the bill to younger Americans. Does debt matter? It obviously does otherwise we wouldn’t have these countdowns that now seem to occur every other month.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

2 Comments on this post

Trackbacks

-

Gringo Bush Pilot said:

Many sources hold that if US debt held the promise of eminent failure, the financial system would have already collapsed. The concept of money and debt is a notional idea – tested 24-hours a day.

It is a fact, that at any given nanosecond, trillions in monetary and spec money is circling the globe in cyberspace. In essence, every digitized penny is simply imagines wealth. In reality, this representation of wealth exists only in the minds of the manipulators. In short, it doesn’t exist, it doesn’t materially exist at all.

So … as long as the US controls the World Bank; The IMF; Wall Street; and the Federal Reserve, the game will continue … in-spite of debt.

Finally, the final arbiter appears: the awesome might of the US Military Machine. As long as The Empire holds the spear, its coin and marker will be honored.February 21st, 2013 at 4:27 am -

Chris said:

Great info, as usual. What I can’t seem to find anywhere is a breakdwon or estimation of duration of the debt held by foreign investors (ie, are they moving to short end or long end of duration and how does this compare over time).

Seems if they are moving to short end while Fed, SS and other domestic holders buy all long end…this would be an ominous sign. Any ideas or suggestions where this info may be available?

February 24th, 2013 at 12:13 pm