The return of irrational exuberance to Las Vegas: The growing worries of another Las Vegas housing bubble.

- 0 Comments

It is rather clear that large institutional investors are diving into investment real estate once again. This time these investors are supplanting individuals but are targeting very familiar markets in Arizona, Nevada, and Florida. One of those markets is Las Vegas. Las Vegas had one of the most spectacular real estate bubbles that we have seen in this generation. The housing bubble was not evenly distributed. You had places across the nation that barely saw the signs of a housing bubble and then you had places like Las Vegas. The glamour and lights in the Southwest Desert.   You had home values rising close to 140 percent from 2000 to their peak in 2007 like some sort of real estate Icarus. The bust was equally spectacular. Today you are seeing the same kind of fervor in the market but this time it is being driven by hungry institutional investors. There are clear signs that Las Vegas real estate is in some form of bubble albeit different from the last one.

The rise in prices

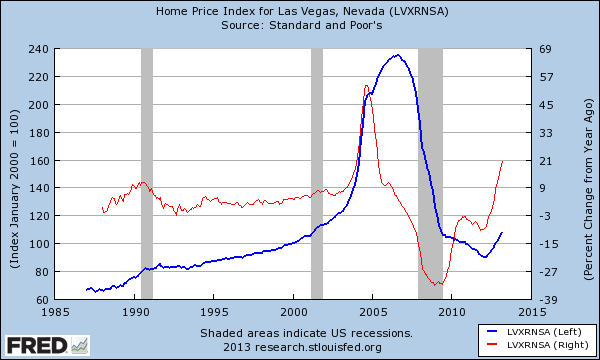

This chart gives a good perspective as to what has occurred with Las Vegas real since the 1980s:

The red line tracks the annual percent change in prices and you can see that according to the Case Shiller Index home prices are moving up at an annual rate of 21 percent. The market in Las Vegas is being driven largely by institutional investors using the Fed’s ultra low interest rate environment to speculate on residential real estate. Unfortunately it looks like this move is crowding out the average home buyer in those markets.

It is hard to track institutional buying since they purchase under various names and organizations but from some of the data we have we can see that the trend is very clear:

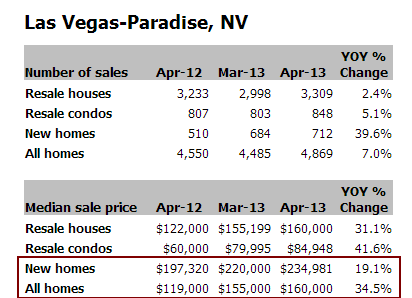

Many will buy homes in bulk here. This massive demand from investors is causing prices to move up:

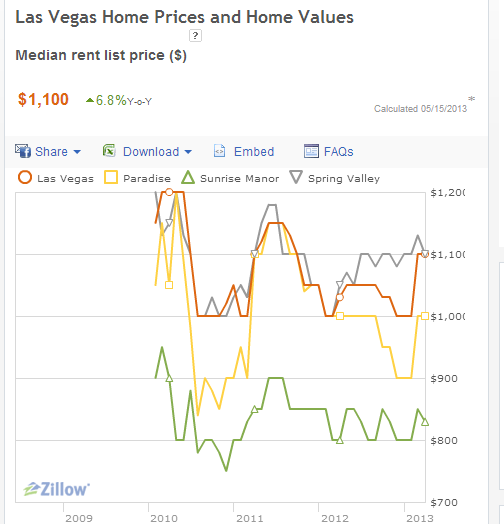

The median sale price in Las Vegas is now up by 34.5 percent over the last year. What is interesting is that although the economy is recovering albeit slowly, there is little justification as to why home prices should be moving up this quickly based on underlying fundamentals. Many of these buyers are purchasing homes as rentals. Yet the rental market is not seeing any major price movement:

For the last three years rents have been stable or falling in many of the Las Vegas areas. One of the reasons could be the glut of rental houses hitting the market but also, rents need to be paid by those in the local economy and wages are not exactly rising in this area. This isn’t lost on people:

“More traditional buyers and sellers are sitting out of the market and investors are bidding up prices for foreclosed homes and [homes] at the lower end of the market,” Quinn Eddins at RadarLogic tells Business Insider.

How big is investors demand?

“(DataQuick) Cash buyers purchased 56.6 percent of the Las Vegas-area homes that sold in April — the highest level since a record 56.7 percent of sales were to cash buyers in February 2011. Last month’s figure was up from a cash-buyer share of 54.5 percent of total sales the month before and up from 53.6 percent a year earlier. Cash purchases are where there is no sign of a corresponding purchase mortgage in the public record. Cash buyers paid a median $135,000 in April — the highest since it was $139,900 in December 2008. Last month’s cash median was up 50.2 percent from a year earlier.â€

Cash buyers ended up buying 56.6 percent of all homes that sold in April. This isn’t your regular family using the Fed’s low interest rate market to get into a home via a traditional mortgage. These are large banks with access to easy capital buying homes in bulk with suitcases full of cash and either trying to flip them to other investors or trying to use them as rentals.

The Las Vegas market is exhibiting all typical signs of a bubble again. First, rental prices are weak relative to the price jumps we are seeing. Second, you are now seeing investors selling homes to one another in a game of musical chairs.

Should we be surprised? The Fed dealt with this housing crisis like it did to the economic crisis of the early 2000s that resulted in the first housing bubble. This time it is different but all bubbles do not look alike.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!