Why inflation matters: How the Fed is creating real estate inflation and hiding behind inflation data to continue their expansionary ways. OER and Case Shiller divergence.

- 2 Comment

Inflation matters. It matters a lot. Contrary to what you may hear in the mainstream press the Federal Reserve has done everything to stoke the fires of inflation. The reasons for this include creating asset inflation that is understated in CPI data and also setting up a system where consumption is almost forced upon consumers. How so? With negative interest rates consumers are losing money by simply having their money in a savings account. Even a modest rate of inflation will erode purchasing power when banks are paying zero percent on your hard earned deposits. Yet this is all part of the design. Inflation matters because it does encourage spending. You want to spend today given that your current dollars will lose value tomorrow. The Fed likes inflation so much that it has reignited the housing market once again while it has expanded its balance sheet to over $3.3 trillion. Inflation absolutely matters.

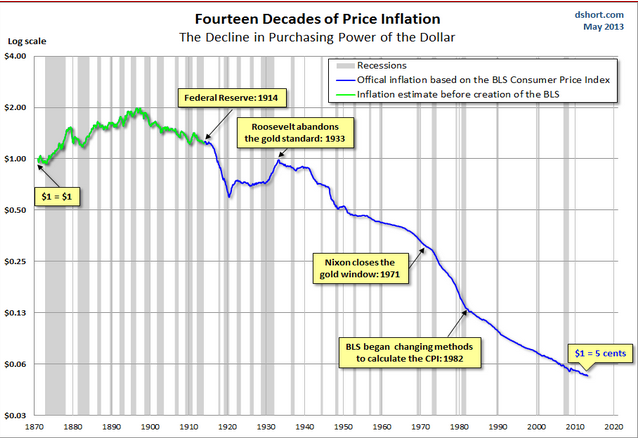

A brief history of inflation on the dollar

What is interesting is the US dollar held steady for nearly 60 years between 1870 and 1933:

Once the gold standard was abandoned, the US dollar has been on a steady decline since the 1930s. It is an interesting trajectory including the era when Nixon closed the gold window. We are merely making an observation of the data here. Without a doubt the US dollar has lost its purchasing power over the decades. This matters because it has also had a major impact on wages and the standard of living especially for the US middle class.

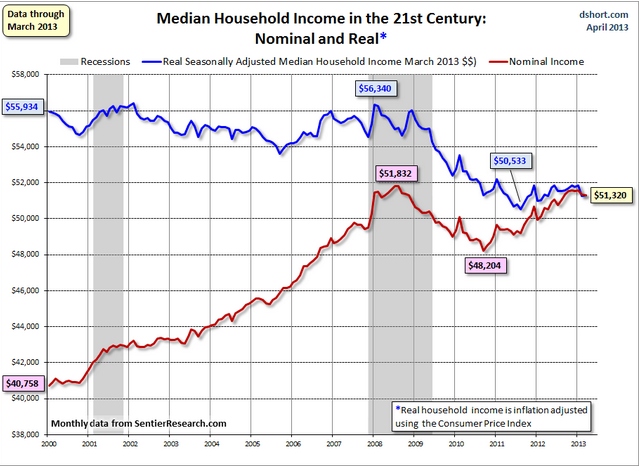

Adjusting for inflation household wages are back to levels last seen in 1995:

This matters because gas is no longer $1 a gallon and no longer can you work part-time at a minimum wage job and put yourself through college. Those days are gone. The cost of living for most Americans has gotten more expensive. We found out this week that home values are increasing at their fastest pace since 2006. The annual increase in prices is over 10 percent. Of course much of this is not coming from wage growth and this should be obvious because of the previous chart. This is largely coming from the actions being taken on by the Fed which is funneling trillions of dollars into the housing market via negative rates and encouraging the financial sector to speculate once again in housing.

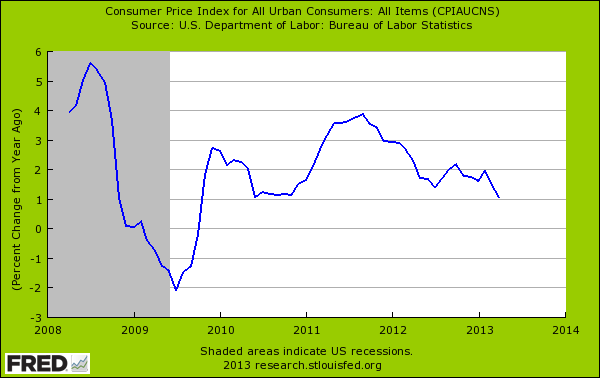

The Fed which relies heavily on CPI data is likely to continue on this road given that inflation as measured by this metric is looking rather timid:

According to the latest data the annual change in inflation is only moving at 1 percent. But if housing is the biggest line item for Americans and just went up by 10 percent, why is this not reflected in the CPI? Once again we run into the problem of the CPI using the owners’ equivalent of rent (OER) measure. This measure missed the last housing bubble and is going to miss it once again.

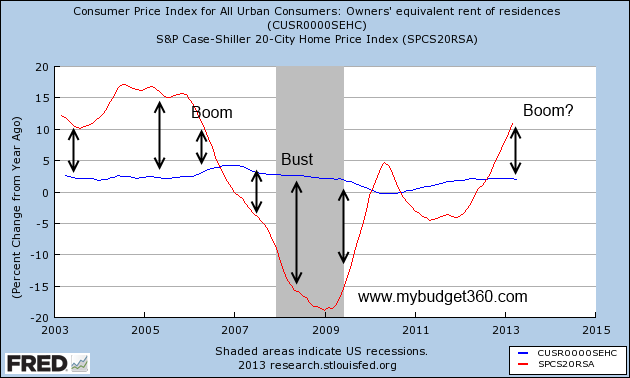

Just to exemplify how poorly a job OER does on measuring price changes in the housing market let us examine annual changes of OER versus those in the Case Shiller Index:

As you would expect, rents are fairly stable over time since they reflect the actual ability of someone to pay out of net income. Yet home values can be manipulated by the Fed by the tweaking of interest rates to make housing payments more affordable yet home prices more expensive. Or in this case, a flurry of investors from Wall Street buying up rentals. At the end of the day, you are paying more for less.

Inflation absolutely matters and you need to know where to look to see these changes. The fact that the Fed is pushing on the housing angle again yet is ignoring the divergence between OER and the Case Shiller is troubling. The lessons should be clear and housing is the biggest expense for Americans. They fully understand this and continue to stoke the fires of inflation.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!2 Comments on this post

Trackbacks

-

D Ross said:

What might be missing here is the monumental growth of production and commerce during the compilation of these dollar comparatives. There was a time, a time when Henry Ford introduced the five dollar a day wage, that it was considered a heresy by the Wall Street capitalists.

A better benchmark might be the amount of work hours needed to secure the fruits of one’s labor.May 29th, 2013 at 6:07 am -

therooster said:

Gold is money, especially now that it’s dollar value has been set free and it can provide unlimited liquidity based on its trade value….. and can support economic stimulus, debt-free.

May 30th, 2013 at 7:53 pm