The Fed is channeling higher interest rates: Fed Committee participants anticipating higher rates and inflation already permeating throughout economy.

- 0 Comments

A market addicted to low interest rates is about to get a shock. Today our debt addicted system is accustomed to central banks providing all sorts of easy money. The market is awash with easy credit and inflation is rearing its funky head in all sorts of segments of the economy. Low interest rates have provided a sort of financial buffer for big banks and Wall Street to gain their footing after the global debt crisis beat down. Yet the Federal Reserve, the most powerful central bank in the world is now channeling higher rates in the near future. Fed Committee participants are already expecting higher rates for 2014 with most expecting higher rates by 2015. The Fed is going to have a tough time turning around this low interest rate ship since the market is now addicted to low rates. The Fed has to maintain its credibility and will need to act. The market is like a jilted lover hoping her partner will change and giving multiple second chances. Yet the Fed is now drowning with a $4 trillion balance sheet and Wall Street has developed a taste for single family homes pushing out regular families trying to buy a home to live in. What will higher interest rates do to this market?

The Fed is looking forward to higher rates

First, it should not be a shock that higher rates are simply part of the Fed’s future. The Fed has been running a negative interest rate environment and the implications are spilling over in multiple areas of the economy. Real estate inflation is hitting because of banks trying to find better yields for their money. They borrow cheaply and go off to find bigger investment plays. When the Fed is offering zero percent loans, it doesn’t take a genius to turn a profit. This has created a misallocation of capital in the markets. Banks should be lending to households but people are largely cash strapped. Member banks are the only players in the game that can create money out of thin air. Yet banks are cautious when it comes to lending to the public.

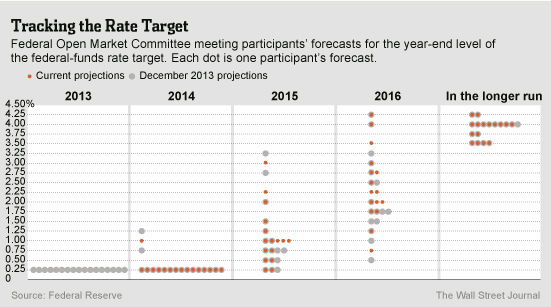

It is interesting to see Fed Committee participants’ forecasts for interest rates:

This isn’t coming from some random analyst or talking head but those actually with the Fed. Higher rates are absolutely in the future. The unemployment rate looks healthy because people are dropping out of the workforce and also, a massive surge in low-wage employment. The current unemployment rate is near the Fed’s targeted rate. Inflation is also starting to show up in the CPI which is always late to the game. However households for the most part are broke and many have no credible plan for retirement.

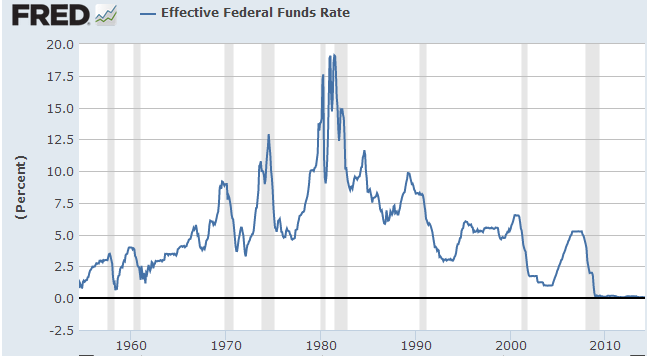

Zero percent for life

Never in the history of the Fed has it held the effective Fed Funds Rate (FFR) near zero percent for any long duration:

That is, until this crisis hit. The Fed has been holding the FFR near zero since 2008. Who really can tell what the long-term ramifications of this will be since we’ve never been in this territory before. And what about the $4 trillion balance sheet the Fed is carrying? There is no credible plan to unwind these assets in the future. The Fed has bailed out banking members and it has worked for this group. Yet slowly but surely inflation is eroding the living standards of Americans and many realize the Fed is not looking out for their best interest.

Higher rates are all but a certainty for the Fed to maintain credibility. Holding rates near zero for close to six years is unheard of. The only other large economy to go down a similar road is Japan but demographically we have many differences. Yet their QE adventure didn’t turn out so well with two solid lost decades of growth.

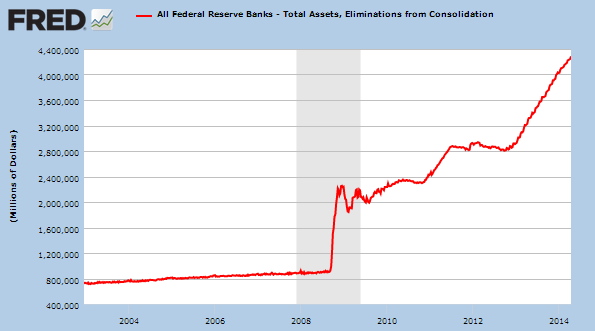

The Fed has shown no sign of unwinding their balance sheet:

At a certain point market participants will lose trust and you are seeing this with large banks taking easy money from the Fed and basically going big on real estate crowding out regular buyers. They realize the Fed is simply eroding purchasing power and would rather dump this debt into a tangible asset class. Yet this is simply a system of banks helping banks out. The middle class continues to shrink and very few in power seem interested in reversing this trend. Why would they reverse the trend if the current momentum is in favor of boosting their bottom line?

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!   Â

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!   Â