A Gilded Age built on debt for modern day financial aristocrats: Fed reports record for household net worth only problem is that most people do not own financial assets.

- 0 Comments

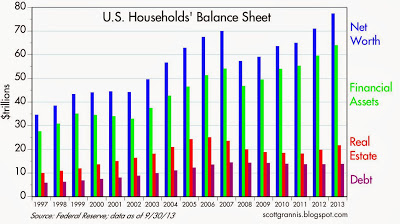

The Fed recently reported that US households reached an all-time record high when it comes to their net worth. A record $77.3 trillion net worth figure was reported with $7.65 trillion of this growth occurring over the last 12 months. The only issue here is that most Americans do not own any financial assets. The bulk of the gain has come from the juiced up stock market courtesy of mega Quantitative Easing. Yet at the same time, we have a peak in food stamp usage and the real estate market is largely being driven by Wall Street speculators. The Fed is creating a modern day Gilded Age that is favoring a very small portion of the population. The vast majority of the population is leveraged into debt with high rates while those with premiere access continue to increase their balance sheets. It is no coincidence that the top 10 percent of households control 75 percent of all wealth in the nation. This is why sentiment for most households is negative. For the majority to participate in this party they need to go into massive debt yet again to pretend they are still part of the middle class.

The rise in financial assets

The rise in net worth is largely being driven by financial assets and the mega-stock market run:

Financial assets make up over $60 trillion in the asset column. Real estate is above $20 trillion but most of the recent real gains have gone to investors since they are dominating the housing market buying up single family homes to rent out or flip. In other words, a significant extraction is happening in the real economy via the Fed’s mechanisms.

For the very poor, the safety net includes food stamps and other income tested programs. For the middle class however, they are dealt a troubling hand of massively inflated college tuition, higher rents/home prices, rising healthcare costs, and stagnant wages:

So much for these massive gains trickling down to the public. It is interesting to read the financial press and how they are “baffled†as to why Main Street USA is still feeling as if this were some kind of recession. The reason of course is that there is growing divide between the connected wealthy and the rest of the country. There doesn’t seem to be any concern that the middle class is slowly beginning to look like the hollowed out manufacturing plants that litter the landscape of Detroit.

No cheer since very little is invested

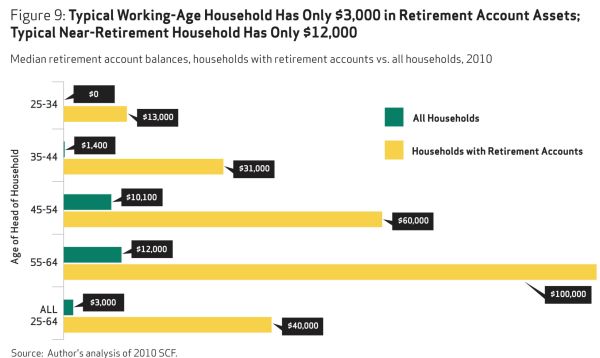

1 out of 3 Americans have nothing saved. So for this group, the stock market is merely a sideshow. Even for those with retirement accounts the story isn’t so pretty:

Source:Â Pew Research Center

The typical working-age household only has $3,000 in retirement account assets. Great. This 25 percent run in the stock market boosted their portfolios by $750 assuming they were all in stocks. This is enough for a couple months of groceries or one semester of books for your kids. The picture isn’t so pretty for those nearing retirement either. Those near-retirement age have only $12,000 to their name. You can understand why household sentiment is not so happy about this recovery.

Much of the stock market gains are coming at the expense of massive central banking manipulation. The Fed’s balance sheet is now close to $4 trillion. There was a shadow banking bailout that has now allowed banks for the last few years to pick up real estate on the cheap from battered down American households. Now they are renting these same homes out for higher rents and flipping them for massive gains. This is how it works. The public bailed out the entire banking system (by force) and now they are being taken to the cleaners yet again. Half of our Congress is run by millionaires largely bought off by lobbyist. The edifice of a new Gilded Age is fully in place. Is it any wonder why only 13 percent of Americans actually approve of the job Congress is doing?

Good jobs and real income gains are the real way to make households feel better financially. Yet the Fed is mainly concerned with protecting the financial sector so it is no surprise that we now see a record in the stock market, a record in food stamps, and a record in net worth. The odds are it isn’t the typical American that is benefitting from these gains.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!