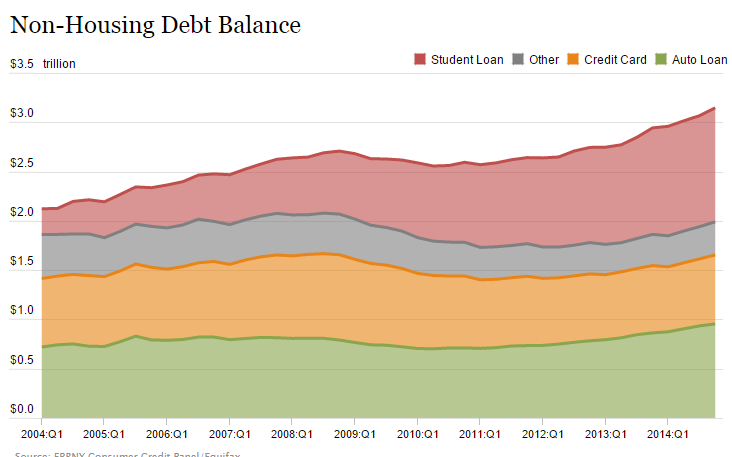

The revival of the American debt machine: auto loans, student debt, and credit card debt surge in latest report. Total non-housing debt now at $3.15 trillion.

- 0 Comments

Last week while going through mountains of credit cards offers, it felt as if we were in 2005 and 2006. Even last year, the cold calls started and it seemed like the debt machine was back and alive. This is helpful news for consumers given that half of Americans are living paycheck to paycheck. Now that the bailouts have aided the very small portion of financially connected, it is time to shower the public with auto debt, credit card debt, and student loan debt to get the party fully going. I’ve covered over the last few quarters the surge in subprime auto debt since practically all Americans have some sort of auto debt. With all those with OK credit being tapped out, it was time to search for a wider market. The last quarter saw auto debt go up by $21 billion, student debt by $31 billion, and credit card debt by $20 billion. Non-housing debt continues to make new highs while housing debt is still off the peak since big banks and investors now own a good number of single family homes. The debt machine is back on.

The debt flows from the mountains

Most of the non-housing debt goes into items that really pull people back from being financially wealthy. Auto debt? That car starts losing value the minute it goes off the lot. Credit card debt? The interest rate on credit cards will make a $500 television cost $1,500 if you simply make minimum payments. Student debt may be a good play if you actually pick the right school, career, and mix this in with your own ability to hustle and find a job. But if you go to a paper-mill for-profit you might as well go to a community college, and use the rest of the money to play at the tables in Las Vegas.

Non-housing debt has made another interim peak:

Total non-housing debt is now at an astonishingly high level of $3.15 trillion. What makes this a bigger issue is that household incomes have gone stagnant while debt continues to serve as a bandage for those trying to hold onto middle class living. The largest occupations in the US all come from low wage positions (only one of the top 10 positions, nursing, pays what we would consider a living wage). And nursing requires a college education so you see how this can become circular. You need some level of debt to play in this debt game.

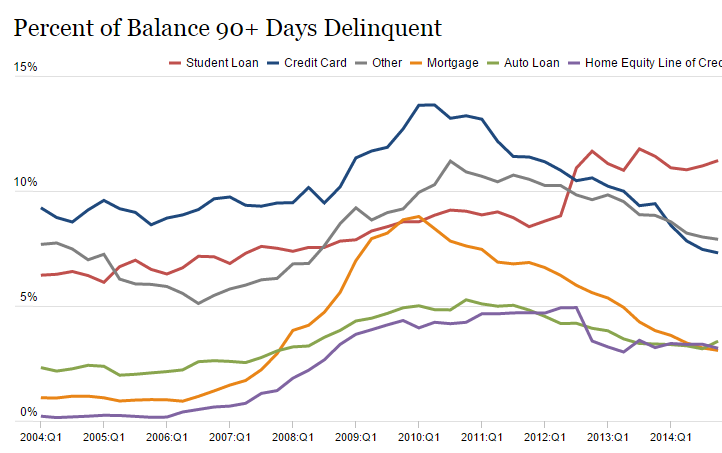

Some would argue that all of this debt is fine so long as people are able to pay it back. That was the argument back in 2005 and 2006 until the entire economy imploded because people took on too much debt. There is a certain tipping point when households taken on too much debt and become insolvent. We are already seeing major issues in the student debt market:

The most delinquent form of debt is student debt. That is a big problem. Think about what is happening in this market. First of all, you can’t discharge student debt in bankruptcy which is simply astonishing. You can buy a car out of your reach and if you miss payments, you will get it repossessed. Simple enough. Don’t pay your credit cards? Your credit will get hit and good luck getting more cards. Bought a house that is too big for your budget? You’ll lose it in foreclosure as millions of Americans did during the Great Recession. But somehow with college, you can go into massive debt and you are on the hook even if you can’t pay it back. This is a modern day debtor’s prison and we are seeing the issues flow through the data.

Ultimately, people are now going back into debt to keep the party going. Like with most things however, using debt wisely is something very few people manage to do and many end up in big trouble. This is another reason why half of elderly Americans would be out on the streets if it were not for Social Security. Instead of saving, people are spending future income for immediate consumption. Given the volume of solicitations I am seeing and I’m sure you are seeing and matching it up with the data, the debt machine is running at full speed again.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!Â

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!Â