Americans are about to get poorer in 2016 as the wealth effect reverses: 63 percent of Americans have no emergency savings.

- 1 Comment

The year is off to a tumultuous start. Markets around the globe are quickly realizing that hot money is going to hit a wall at some point. Many Americans are coming to the stark realization that the recession that ended in 2009 never really ended for the middle class. In fact, it might have been the nail in the coffin for the middle class. Much of the fragile gains really went to a small fraction of Americans and the financial system is predicated on siphoning off wealth from the working class. Many Americans are still living on the financial edge. A recent survey found that 63 percent of Americans have no emergency savings. Forget about having a robust nest egg.  The retirement plan for many Americans is to work until they fall over dead. While the last few years brought in spending with debt this of course was set to reverse once the market had its first tiny correction since 2009. Americans are about to feel and become poorer in 2016.

The old and young will feel the pain

Having an emergency fund is basic financial planning. But most Americans simply do not have a fund because they are too broke after paying basic bills. After all, we have nearly 46 million Americans on food stamps and this is happening during a time that we are supposedly in recovery. What will be the case when another recession hits? And for most Americans, the old recession never left. We have a record number of people not in the labor force making the unemployment rate seem artificially low.

The wealth effect will reverse and the stock market already had a dismal 2015. 2016 is off to a horrible start. Markets in China had to be halted twice because of steep drops already and we have yet to even hit the middle of the month. The US market is also feeling the pain.

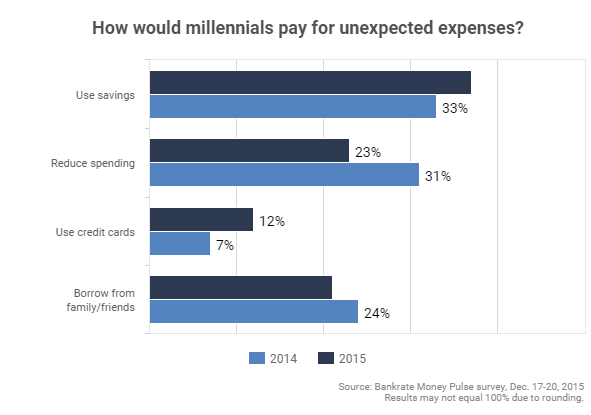

The young workforce of America is largely broke. Take a look at how Millennials would deal with an unexpected expense:

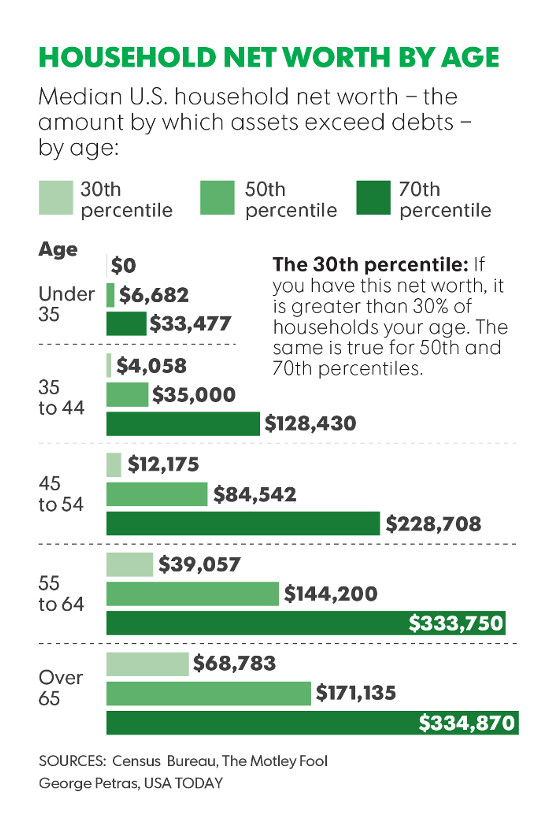

In other words, spend future funds to deal with needs of today. This is why most Millennials have nothing saved for retirement. But older Americans aren’t doing so much better:

To summarize, most under 35 have $6,682 or less. Those 35 to 44 have $35,000 or less. Those 45 to 54 have $84,542 or less. And those 55 to 64 have $144,200 or less.

But that data is misleading. Why? Because the vast majority of net worth figures are derived by equity in real estate and as you know, you can’t feed yourself through equity. How many older Americans are going to sell their homes to pay for food? And for younger Americans the net worth figures are dismal because they have been crushed out of the housing market as investors push prices up. The homeownership rate has crumbled for young Americans and this cuts into their ability to build up equity for later years in life (not that this is a silver bullet for older Americans either).

Now that the stock market has hit a wall, real estate is sure to follow. After all, housing is tethered to the health of the economy which supposedly is reflected in the stock market. This reverse in wealth is sure to ripple through the economy. We are already seeing hits being taken:

“(USA Today) Capping a disappointing holiday season, Macy’s (M) will eliminate more than 4,500 positions as part of a restructuring plan to turn around the department store’s slumping sales, the company said Wednesday.â€

And as many of you are aware, spending is the heart of the economy. So 2016 isn’t off to a great start and many Americans are going to feel poorer in 2016. Gear up for austerity for the working class and social welfare for the financially connected on Wall Street.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! Â

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!  1 Comments on this post

Trackbacks

-

Beano McReano said:

Cash is king! No wonder they print it like there’s no tomorrow!

January 7th, 2016 at 3:27 pm