Collection nation: One out of three consumers have debts in collection over the past year. A total of 77 million Americans are having problems managing their debt. 22 million consumers have zero credit.

- 1 Comment

A recent report by the Urban Institute and Encore Capital Group’s Consumer Credit Research Institute has found some rather startling news about consumer debt in the United States. Over one third of consumers had some sort of debt in collection over the past year. Of course this coincides with the struggling employment growth that many are facing or the stagnant wages families are encountering. For a nation so reliant on debt, this is a big problem. Many people mistake access to debt as some form of wealth. Many working class families go deeper into debt to keep up the pretense that they are securely in the middle class when in fact, inflation is simply eroding their purchasing power. The data also shows that Americans are juggling a multitude of debt from mortgages, student loans, credit cards, auto loans, and other debt that once was rare. Now it would seem that debt is simply a way to keep buying things one cannot afford. So what does it say when 77 million Americans are having a tough time staying current on their debt payments?

Debt addicted nation

Most studies that I have seen show a middle class that is dwindling and many are trying to keep up a middle class lifestyle by simply going deeper into debt. The debts range from trivial to large:

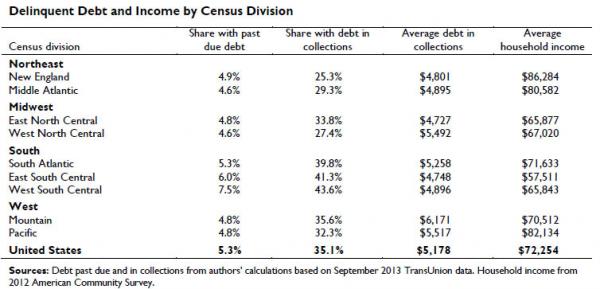

“(Washington Post) The debts sent to collections ranged from $25 on the low end and to more than $125,000 on the high end. Many consumers were burned for relatively small amounts — about 10 percent of the debts were smaller than $125, Ratcliffe says. But the median debt, $1,350, is still pretty substantial, she adds.â€

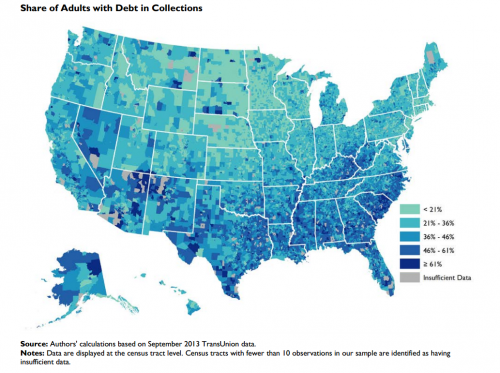

The median debt size in collection of $1,350 is large given that one third of Americans have zero dollars to their name. More importantly, we also know that half of this country is living to paycheck to paycheck treading on a financial high wire act. This problem spans across the nation:

What I find interesting is that the average household income here is rather high compared to the median household income of $50,000. What this tells us is that many people are once again living beyond their means. If you live in a household making $80,000 and buy a $400,000 home you are very likely living beyond your means. But the study also found that a large number of Americans are simply off the credit radar:

“Researchers relied on a random sample of 7 million people with data reported to the credit bureaus in 2013 to estimate what share of the 220 million Americans with credit files have debts in collection. About 22 million low-income adults who did not have credit files were not represented in the study.â€

Another 22 million Americans simply have no credit history at all. In a country where debt is your key pass into college, housing, and cars this will keep some of our country’s poor in a perpetual cycle of poverty.

The fact that so many Americans had debt in collection over the past year is startling especially when we consider that the stock market is near a record high and our unemployment rate continues to drop. A couple of points here. Much of the job growth has come via the low wage employment sectors. While wages are stagnant or falling, the cost of living is surging thanks to inflation induced by very generous banking policies. These policies have assisted in widening the gulf between the working class and a very small number of Americans that are cornering a large part of wealth in the nation. Next, the unemployment rate dropping is a sort of magicians trick since we have millions of Americans simply dropping out of the labor force.

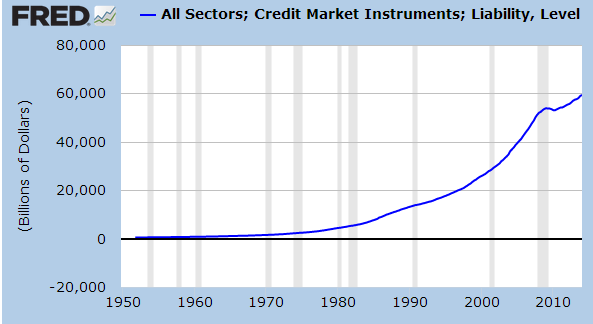

Is this surprising? The total debt market in the US is now approaching $60 trillion:

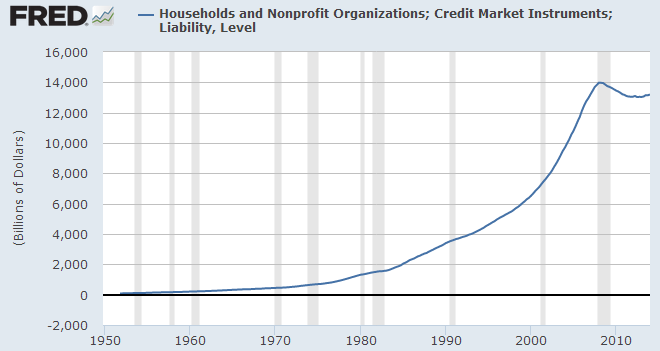

Of this, total household debt is well above $13.1 trillion:

$1.2 trillion of this is student debt. Another large chunk of this is being made up of auto loans, many in the subprime category. So it should be no shock that this nation is having a tough time keeping current with their debts. Unlike large banks that can freeze accounting rules, the public is not afforded these privileges. Yet because of the public’s support or apathy, the banking system has been fully bailed out. Interestingly enough it is the same banking system banging on your doors to collect that $25 late payment. Shouldn’t we be knocking on Wall Street’s door for the same thing?

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!1 Comments on this post

Trackbacks

-

Dan said:

Thank you for your website. I am a loyal reader.

There is one thing you never mention. And that is medical debt. It is not like you have much of a choice in this area unless you just decide to not get help when you need it. This is very difficult to do when you are very sick.

Dan

July 30th, 2014 at 7:17 am