What is the Federal Reserve’s end goal? Follow the money and you will find no intention of tapering, out of control public debt, and financial steroids for stocks. Fed balance sheet up $55 billion in one week.

- 1 Comment

The Federal Reserve is known for producing convoluted and purposely hard to decipher messages. The media is driven by what the Federal Reserve says but fails to analyze what is truly happening. The Fed is driving in a car with no brakes. This is clear given that the Fed balance sheet increased by $55 billion in one week (or a rate of $220 billion in one month). Not only is the Fed not tapering but it appears to be accelerating Quantitative Easing. Follow the money and you are led down a path of no return. The Fed is juicing the stock markets and is perfectly fine with Wall Street creating another real estate bubble. Many poor and working class Americans are still deep in what appears to be a recession. Those with the ability to access the digital capital of the Fed are given an opportunity to gamble and speculate while low wage capitalism engulfs the middle class. What is the end goal for the Federal Reserve?

Fed balance sheet up $55 billion in one week

The Fed’s balance sheet is now up to $3.9 trillion:

I thought it was going to take longer before breaching the $4 trillion mark but we are not far from hitting this. The housing market is already showing signs of massive overheating. The main drive of QE is to provide artificially low rates in the market but all this has done is recreated mass speculation. It is hard to see how this is actually improving the underlying economy.

The increase of $55 billion came from:

Increase of $21 billion in bank reserves

Increase of $32 billion in other Fed liabilities

The bulk of the other liabilities are largely from QE. The Fed is betting on the law of large numbers. People will simply glaze over when they hear $4 trillion. In fact, on the other side of the aisle, we have our public debt that completely blasted through the $17 trillion mark without skipping a beat:

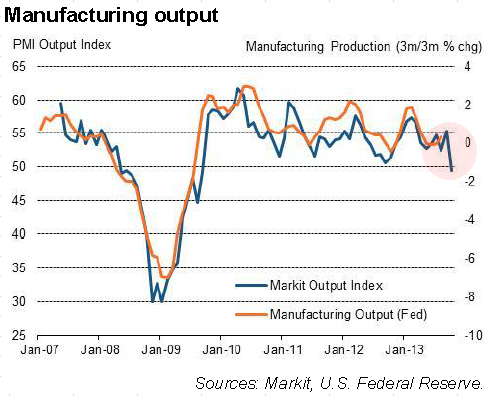

The US has no way of avoiding a soft default via a slow and methodical inflation. The costs of the bailout and the current artificial market are being supported by the working and middle class while a very small portion of the population continues to extract wealth from the real economy. If you needed any more proof that the current recovery is facing challenges US manufacturing had its first real contraction going back to 2009:

This is not a positive sign. The Fed has made it appear, at least in their statements that the current end game involved slowly moving away from QE. Yet the exact opposite is happening. So what does this mean for you? The dollar is going to have pressure on the downside. Look at the cost of housing, cars, college, and healthcare and ask yourself if things are really getting cheaper. Wages are stagnant so you see how this rebalancing is going to play out. The Fed is favoring stocks and banks at all costs. Yet this isn’t necessarily a winning strategy for the overall economy. In other words, massive risk is rampant in the current economy.

We will never payback that $17 trillion in public debt. In fact, shifting to the Fed balance sheet it is unlikely that $4 trillion in liabilities will ever be unwound. Where will the liabilities flow to? The entire reason QE is in place is because the natural market has absolutely no desire for long-term debt with absurdly low rates. The Fed doesn’t have an end game that includes helping the working and middle class. This is basically a debt spiral and a game of confidence. If we truly follow the money we can put our money on a few things:

-The Fed is not going to taper anytime soon (i.e., the Fed Balance sheet will continue to grow)

-Public debt will never be paid back. In fact there is legislation pending that tries to avoid any debt cap

-The Fed is looking out for banks, not the public

It was stunning to see the Fed balance sheet jump up by $55 billion in one week. At this rate, we’ll be over $4 trillion before Christmas. Taper? Yeah right.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

1 Comments on this post

Trackbacks

-

therooster said:

The mission statement for the dollar is to support the real-time valuations of commodities and in particular, precious metals that now float against the dollar in real-time. Precious metals are a limited and finite resource, so monetization would require that they have scalable liquidity (weight x trade value) in order to support growing economic activity. If PM’s were ever going to serve us as good responsible currencies with scalable liquidity, the FIXED peg of Bretton Woods had to be abolished. That stage was set in 1971. The dollar’s role as a currency is but a stop-gap measure in an apprenticeship to emerge as part of the real-time bridge of USD/oz. The real-time trade value of USD/oz to migrate from FIXED gold to flexible gold with necessary evils in-between is the prize. Follow the script.

November 2nd, 2013 at 6:49 am