The Great Income Divide: IRS data shows 50 percent of households make less than $35,000 per year. Top 10 percent pay 68 percent of income taxes.

- 2 Comment

A major theme throughout 2013 revolved around a booming stock market and real estate sector. Alongside this theme however was also the one of growing income inequality. The stock market generated one of its best years but only a small portion of the population benefitted since most Americans do not own stocks outright. The real estate boom was largely driven by big money investors leveraging the unprecedented Quantitative Easing machinery from the Federal Reserve. Yet most households have little access to this debt since deleveraging is still occurring for households. The only consumer debt sectors to boom in 2013 came from student loans and auto debt. Not exactly two sectors to build up your wealth portfolio. We see how the great income divide is splitting the nation even when it comes to paying income taxes. The adjusted gross income for half of households in the US is less than $35,000. This group pays 11.55 percent of all income taxes. The top 10 percent pay 68 percent of all income taxes. This is an expected trend when wealth inequality is at levels last seen since the Gilded Age.

The growing income divide

The IRS tax data is one of the best sources to mine for information since all US households are required to file a tax return short of a tiny group. This is no survey data but actual raw data based on real incomes. It helps to shine a light on what is really being generated in the US economy based on income.

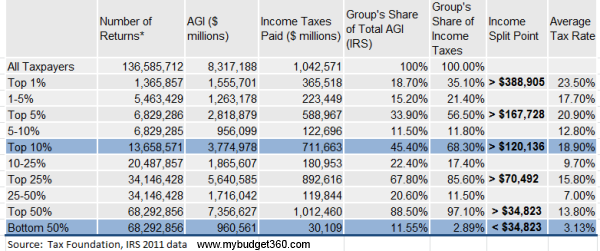

The data highlights a complicated tax system that doesn’t really show the entire picture. The below data is a reflection of income taxes and does not capture the full scope of taxes including FICA, state taxes, sales taxes, and property taxes that tend to be more regressive. Income tax by its nature is a progressive tax; the more you earn the bigger your share:

The chart highlights the widening gap from the top to the bottom. Even within the top, the gap is growing dramatically. For example, to be in the top 10 percent of households you would need an AGI of $120,136. To be in the top 5 percent, you would need an income of $167,728. Not a major difference here. However, to reach the top 1 percent you would need an AGI of $388,905. The top 10 percent of households pay 45.4 percent of all income taxes. Since many of these households control the bulk of stocks and wealth, a banner year for 2013 will mean tax collections should be healthy for the upcoming year.

What is startling is the lower range of the curve. The bottom 50 percent of AGI households has an income cutoff of $34,823. Over 68 million US households live on an AGI of $35,000 or less. This is telling given the rising costs of college education, healthcare, real estate, and food.

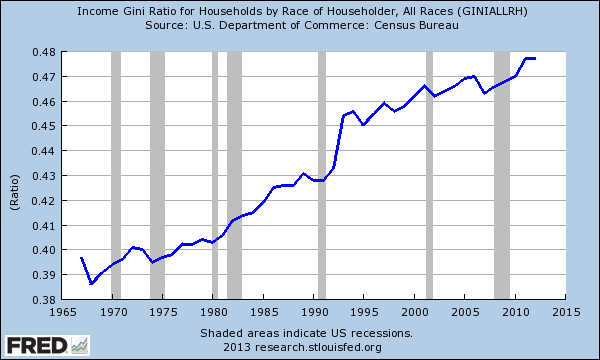

The rising income inequality in the nation is no secret or mystery. In fact, this growing income inequality dates back many decades ago:

Since the 1950s the trend has only moved in one direction. People often talk about top tax brackets and how high income taxes are but if you look at the above chart, the average tax rate for those in the top 1 percent is 23.5 percent. How is that when the top tax bracket is 39.6 percent? First, many people have better methods of tax avoidance: IRAs, 401ks, dividend income, real estate deductions, etc. Since the bulk of wealth is in the hands of the top 10 percent, this group is already lowering their tax burden via these deductions and beneficial tax structures. Since the typical American is living paycheck to paycheck with little saved for retirement these tax reducers don’t really help. Besides, their income tax burden share is minimal. However, their other tax burdens are large as a proportion to their income. This is usually ignored when people talk about how little the working class pay in this country as they try to scapegoat the disappearing middle class.

More to the point, the middle class by definition should be well, the middle. In this case, being middle class is a household making $35,000 or more. We often hear about $250,000 being middle class by the media but by the IRS tax data, this is closer to being in the top 2 percent of AGI. Not exactly middle class when 98 percent are below you. Even if we look at the bottom 75 percent, the cutoff here is $70,492; certainly a far away cry from $250,000. Or even the top 5 percent starting point of $167,728.

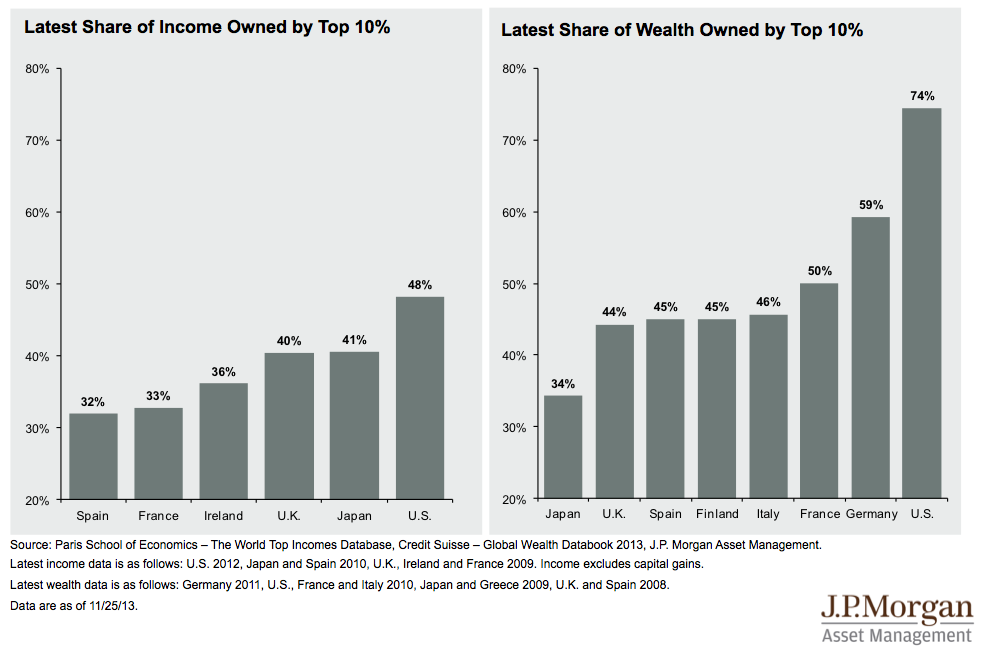

The growing income and wealth divide in the US is problematic. The top 10 percent control nearly 75 percent of all wealth in the country, the true sign of economic prowess:

This also means the other 90 percent of the population has 25 percent of the remaining wealth to divide up. You would think a banner year for stocks and real estate would leave everyone feeling happy. But when you look at income data, you begin to understand why regular American families are still dismayed at the state of the current economy.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!2 Comments on this post

Trackbacks

-

Rainwaterrunningdog said:

THE ENTIRE SITUATION IS IN SPIRAL DOWNTURN. LUCKALLY, SO MANY AMERICANS OF THE 90% OWN ALOT OF FIREARMS LEGALLY AND ILLEGALLY. THE CLEANSING WILL BE BLOODY BEAUTIFUL!

January 1st, 2014 at 9:09 pm -

stephen verchinski said:

Lets see the figures with all payroll taxes including SS included. Will it make a difference?

January 2nd, 2014 at 12:29 am