One-third of working Americans support two-thirds of the population: The hidden figures of those not in the labor force and transfer payments.

- 2 Comment

There still seems to be little acknowledgement of the massive army of people now falling into the category labeled as not in the labor force. Some of this growth is predictable like many older Americans hitting retirement age. But this only explains a small portion of the change since many older Americans are needing to work much longer since they have paltry retirement savings. The unemployment rate dropping dramatically has largely been driven by this category expanding and labor force participation is at generational lows. You also have spending growing in the form of military, Medicare, and Social Security that are now eating up a larger portion of the budget. Deficit spending continues to occur in the face of a booming economy. Why? The math shows that one-third of private sector workers are supporting two-thirds of the population. We have over 92 million Americans that are now part of the not in the labor force category. Let us dig into the numbers even further since some tend to think this is only happening because of older baby boomers.

Not in the labor force demographics – not just old people

People tend to think that those in the not in the labor force category are largely older people. That is true but we’ve seen a large growth of those in their prime working years landing in this category. That is not a good thing. We’re also seeing more students go to college which is positive as long as you are not going into massive debt and are pursuing a quality education. Sadly, many are going into deep debt for a mediocre education.

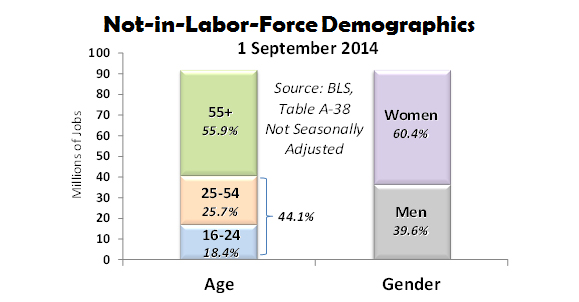

Let us look at the not in the labor force category carefully:

Source: BLS, Jobenomics Blog

This is a very high number of people not in the labor force. Nearly one-third of the country falls in this category. And what we find is more older people are making up a larger portion of the labor force.

Labor force participation rates – the boost in unemployment figures

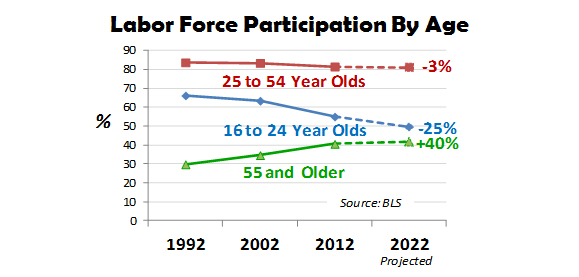

There has been some dramatic shifts to the labor force. Take a look at the following chart:

Source: BLS, Jobenomics Blog

Over the last two decades, the largest growth to the labor force has come from those 55 and older. For younger Americans the labor force hasn’t been so kind. Part of this is more people going to college and taking on massive student debt. Another part of this is a growing number of part-time workers that land in transient positions creating many people that enter and exit the labor force on a routine basis. There has also been an argument that many older workers are locking up positions that would once go to younger workers.

Ultimately the numbers are not as great as the headline unemployment figures report. And what we have is now a large portion of transfer payments hitting the economy.

Transfer payments

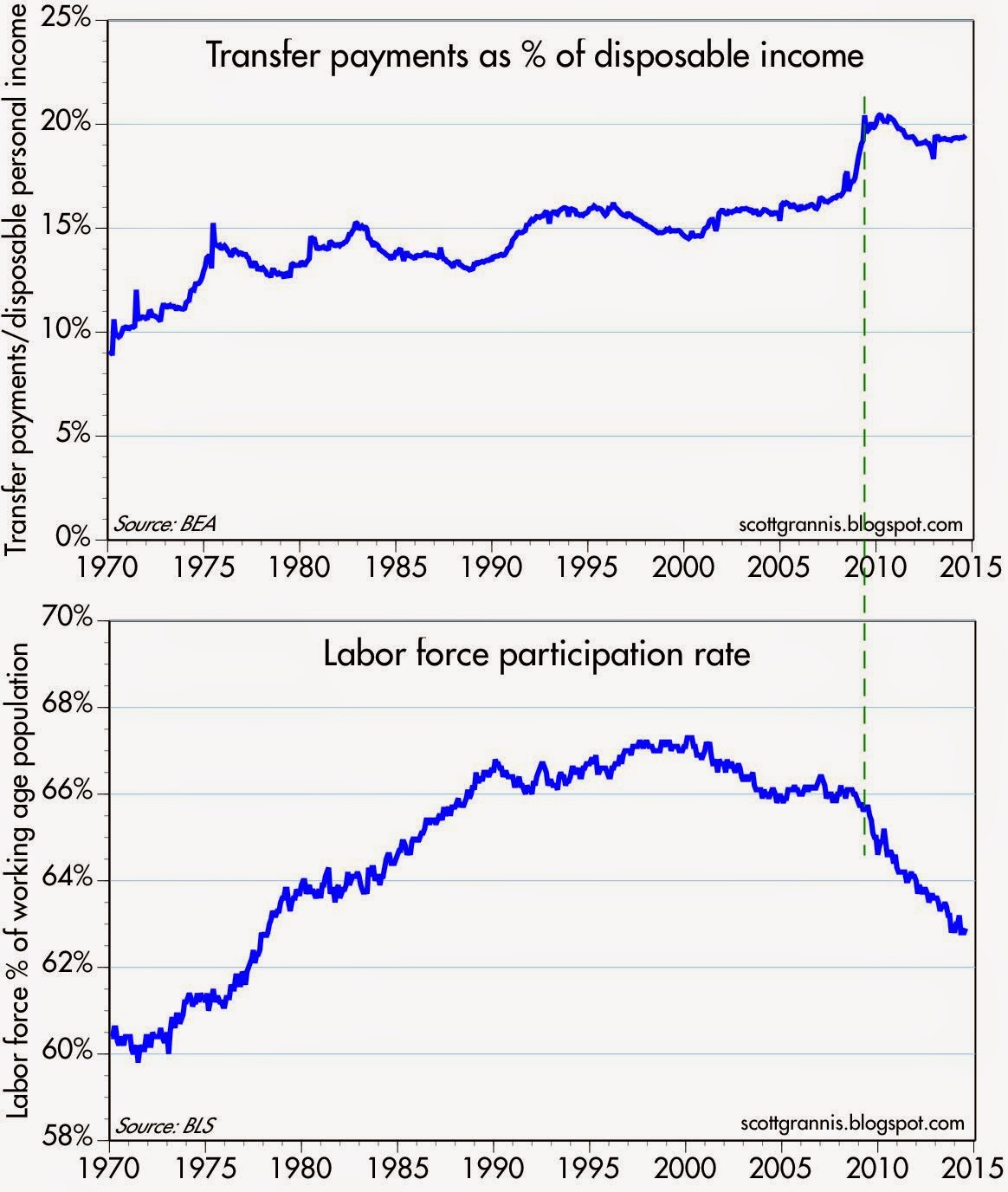

Here is an interesting chart regarding transfer payments:

With an aging population and more people drawing on government programs, more disposable income is going to transfer payments while the labor force participation rate falls to generational lows. This simply puts more pressure on the current workforce.

One-third working for two-thirds

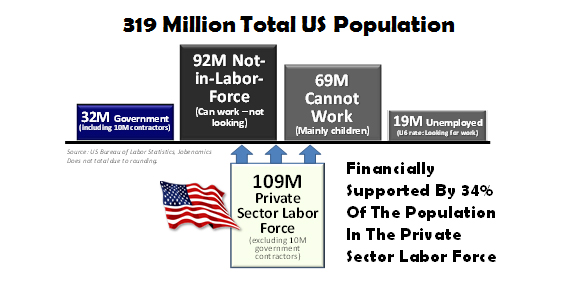

One of the most startling facts is that one-third of the nation’s workers are supporting two thirds of the population:

Government workers are paid via funds that come from taxes. 92 million are simply not in the labor force. Another 69 million are not working, mostly children. And 19 million are unemployed. Is it any surprise why we are running big deficits? These are mega trends that won’t reverse anytime soon. It also helps to explain why millions of Americans are completely unprepared for a long retirement. I’m not sure if the mainstream press will cover this issue more carefully but it is very important and helps to explain why our rosy unemployment figure isn’t as great as it appears.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!Â

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! 2 Comments on this post

Trackbacks

-

Hajo said:

“One of the most startling facts is that one-third of the nation’s workers are supporting two thirds of the population”

Its never been otherwise. Two working adults support two children too young and two grandparents too old for work plus the disabled and sick.

Then this distribution was arranged in family, clan, tribe etc. Nowadays via state, social insurance, privat insurance, savings (in debt), rent-yielding assets.

Bottomline: nothing new under the sun.

Regards

October 21st, 2014 at 10:21 am -

Dowless said:

The only new thing about this phenomenon is that one of the two thirds being supported (the ones drawing government funds, welfare, etc) could be out working, if there existed real self supporting job opportunities, as there once were forty years ago, before NAFTA, astonishingly increasing prices combined with ridiculous taxes, ETC, and the death of the apprenticeship school, entry level jobs in career fields, and on-the-job training, which can never be replicated in a classroom, which attempts to replace hands on experience/pretend to offer employment opportunity when the fact is that none actually exists! Need I say more about how today’s scenario is vastly different than any other ever experienced here in America before?

January 5th, 2015 at 6:24 pm