New Retirement Model of Working into Old Age – Baby Boomers hitting retirement age with little to no savings.

- 10 Comment

The fiscal issues facing the country are troubling for a variety of reasons but one big reason is the reality that many older Americans simply do not have enough money to retire. The idea of entering your golden years without the need of working is a relatively modern one. In fact, it was the generation that grew up after World War II that enjoyed this middle class ideal. A secure job, a paid off house, and the ability to send your children to a good college. That was the dream. Yet that dream is now largely gone in a puff of smoke. It has been gone for sometime but the ability to access unsupportable debt kept the party illusion going a decade or so longer. Today, Americans are now entering retirement at a time when the stock market has given zero returns over a decade. Government debt is tipping over and we continually spend more than we earn. For millions of older Americans, retirement means continuing to work.

The evaporation of a pension

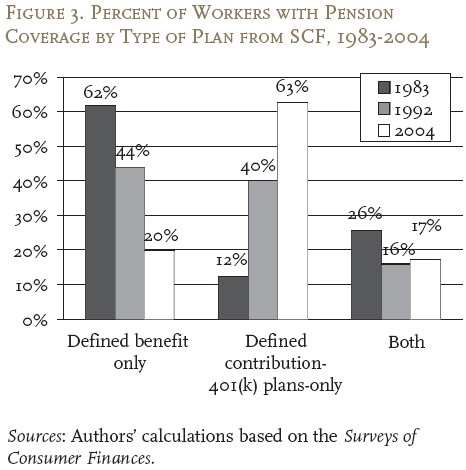

Back in 1983, not too long ago 62 percent of Americans had what we would call a pension. Today that figure is down to 20 percent:

That rate is now much lower if we had data on it since this research was done prior to the 2007 meltdown. The meltdown also brought to the forefront that unrealistic returns of 8 to 10 percent per year were mostly pipe dreams. The 2000s were largely a decade fueled by high debt spending. The real estate bubble created a sugar high that really did not add any deeper value to our overall economy. Many in fact tapped into their equity, a thought that would seem sacrosanct in the previous generation, and will now have to pay it back. In the past the ability to have a paid off home provide added security. Many then with a modest Social Security check had the ability to make ends meet. Many today continue to carry a mortgage well into older age.

This becomes even more troublesome because the majority of retirees depend on Social Security as their largest source of income. This ties in with the earlier chart. Even in the 1980s those with pensions likely had a bigger cushion when they combined this with Social Security. That is no longer the case. Today, most have the access to 401k plans and as we have seen, the market is back to levels last seen in the late 1990s. Also, those that built portfolios up during this time will need to sell to withdraw funds to live. Who will buy these funds? Younger Americans? Younger Americans are massively in debt and half are either working at jobs that don’t require college degrees, are underemployed, or have not job. The 401k is the least of their worries.

Less work and more college debt

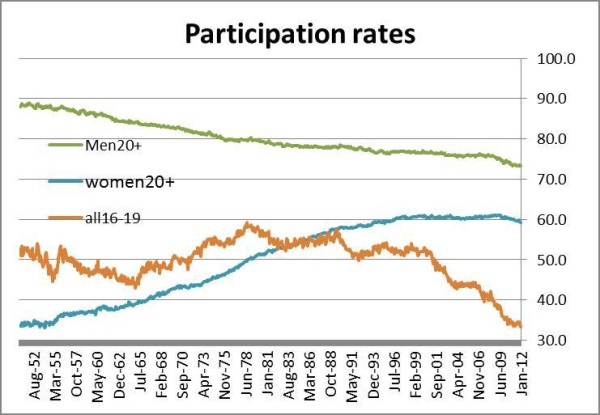

It is clear that education is valuable for many reasons. Yet with tuition costs being so high you have to ask whether it is worth it. Our overall participation rate in the workforce is dramatically lower for younger Americans:

Many are now competing with older Americans for lower level positions. You also have massive numbers of students going to college yet overall, a college degree has been watered down.  You might ask, if younger Americans are poorer how can they afford record levels of college costs? They can’t. But what they can do is go into massive student debt. This is why today, total outstanding college debt is well over $1 trillion.

So think about this. You have an older population with 10,000 Americans hitting retirement age each and every day. Many will rely on Social Security at a time when we keep going into deeper debt. You then have younger Americans with a large portion already in deep college debt working jobs that largely do not pay a good wage and the days of a pension are all but gone. It should be no surprise why we now have 47.7 million Americans on food stamps.

How will America adjust to this world with no retirement or with the idea of what we once thought of as retirement? It isn’t a question we need to ponder much since we are going to find out in real-time.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!10 Comments on this post

Trackbacks

-

Tony W said:

This is all true, but the other side woulde say while U.S. is high as a percent of GDP it is low, suggesting the debt is somewhat manageable. We’ve been hearing nightmare-like scenarios for now, and yet the rest of the world keeps buying up our debt, seeing us as teh best bet in a bad lot. How would you respond to that?

December 15th, 2012 at 3:48 pm -

M said:

For the generation who told me from day one at job in the 80’s. You will never see a dime of social security or medicare taxes. Then smugly repeated this jibe for the next 3 decades. Lets just sympathy for generation screw you me first is somewhat lacking in me. Hope every one of you that said that chokes on your own vomit ).

December 15th, 2012 at 5:20 pm -

James Hammers said:

I am 76 and am one of those who is still working part time at almost minimum wages but I am thankful that I am getting SS. I have paid into SS for 60 years, paying into the fund with every dollar I earned (except during those early years when one would hit the wage limit somewhere during the year. But that does not happen anymore unless one makes over $110,000 or thereabouts and not many do) And even though I am receiving SS and Medicare, I am also paying about 10% of every dollar I make into SS and Medicare without any increase in benefits. So I am receiving from SS and Medicare with one hand, and returning a painful sum with the other. But even though I do not make enough to warrant an increase I do make too much to pay income taxes on some of it. So I give some of it back directly and then at income tax time I pay in again with no increase in benefits. That is a 10%+ tax that I, and the army of elderly workers like myself, pay before we pay our regular income tax when we need more not less to continue to provide for the basic necessities like food, shelter and medical care. Government programs help but corporate America and their representatives in government cannot abide that “their” money is being given away to the likes of us. The wealth Americans generate is our money and we deserve to get at least enough of it to live on. Why is it ok for someone to feel justified in taking as big a chunk of that wealth as they can get their hands on but it is not ok for someone to say, “I am hungry. Please give me some money for food. I am about to lose my home, please help me keep the shelter I have. I need medical help, please help be get it.” What makes America different is that supposedly we help one another out. We pull together. Anyway that is what we hear in campaign slogans. I surely wish that were true.

December 17th, 2012 at 2:13 pm -

M said:

A lot of us young folks would have been ecstatic to pay only 2% of income in SS tax. For the first 24 years that we worked , ho ho go eat cat food and like it .

December 18th, 2012 at 7:56 am -

runman said:

Yes your goverment has f up. So the questoin is why do people still vote for them. If i came in and destroyed your life and ripped you off while claming i am doing an excelent job. Would you support me, i think knot so why support these crettins. A true free man has no goverment.

December 19th, 2012 at 9:46 pm -

Lady Liberty said:

On top of this they now want to throw Granny under the bus

The Great American Retirement Scam: Why The Wealthiest CEO’s In America Want To Take Away Your Social Security

http://awesomescreenshot.com/00dqell6b

SOCIAL SECURITY SELL-OUTS

http://www.huffingtonpost.com/2012/12/19/nancy-pelosi-social-security_n_2333285.html

December 19th, 2012 at 9:59 pm -

guy said:

Feminism,another hoax perpetrated by the globalists that destroyed the middle class -socially and economically: http://www.mybudget360.com/wp-content/uploads/2012/12/participation-rates.jpg

December 19th, 2012 at 10:57 pm -

Ken said:

For those who oppose massive legal and illegal third immigration and, above all else, the changing demographics, you will have to speak out loudly: join an immigration reform group, like FAIR (strength thru numbers); when you get a political fundraising letter, return it, with no money, and state your opposition to the immigration tragedy; call a radio talk show to let thousands of listeners know we exist; write/e-mail your local newspapers to express your opinion (so far, three item were printed in The York Post); and, finally, fax your rep in congress. I am sure they delete e-mails concerning this subject very quickly. More can be done on this front. Do your own gardening; don’t go to restaurants. You would be amazed at how money you save. PLEASE FORWARD…..

December 20th, 2012 at 7:04 pm -

mike said:

James, not all of us are as shortsighted as M. I wish you the best – we’re all in the same boat, whether we realize it or not.

December 20th, 2012 at 9:07 pm -

Roger said:

The Truth is concerning social security is and was never designed to provide for so many people especially those that live to be in their late 80’s and 90’s . The average death cost at tend of life is about 40 grand in medical care includeing ambulance rides, emergency care and hospice . Also the staggering amounts of medicine needed to keep people alive longer is costing billions. The average person on social security is takeing more than one medication and even reports that takeing 20 pills a day is normal . The cost of medicine is off the hook and ever growing . The cost of living is a lot more, when some people retired gas was 50 cents a gallon now its over 3 bucks and flexes up to 4 bucks . cost of living is not keeping up with what social security gives out . The system was never designed to serve so many and pay out so much in benefits .Most people today only pay in about up to 200,000 out of their salaries over the years while those 10 to 20 years ago paid in less than 150 grand in total but are useing about 500 grand in benefits before death . Common sence says if your paying out more than you putting in that a hugh problem occurs .I do not blame people who have paid into social security as myself i am still paying and will probably be paying well into my years , maybe even age 68 to 70 as they must increase the ages( im sure the employers will be hireing us up lol ) . Im 45 years old now and i have over 168 grand paid into social security thus far.Will i see it or not,Im not banking on it because i know currently it is unsustainable .People seem to think that their is giant Government bank vault with trillions of the peoples money in it but the truth is each social security check is just printed into exsistance from a machine and paid out every month . The end game is coming for America folks .Like human beings , we have a limited life span on earth and so do Governments and Nation’s .They rise and fall .We are based upon a fiat monitary system that is debt based and through out mankinds history this particular system in time always fails , notice the word ALWAYS !

December 25th, 2012 at 2:52 pm