The new subprime is in auto loans: One third of all new auto loans are of the subprime variety. Repossession are up 70 percent.

- 5 Comment

Leave it to Wall Street to resurrect the subprime loan. This time, subprime has found a comfortable home in the automotive industry. In the car addicted US culture, subprime debt is back in a massive way. Subprime auto debt is the new risky debt product. This is a big deal. $924 billion in total auto debt is rummaging around the economy. What is even more disturbing is that delinquencies on auto debt are surging. Repossessions are up 70 percent because people simply can’t make their auto payments. What do you expect when you are pumping out subprime debt trying to churn more sales on marginal buyers? Most Americans are living paycheck to paycheck so taking on another debt payment isn’t necessarily a wise move. How big is this market? The latest data shows that a stunning one third of new auto loans are in the form of subprime debt. This is telling given that FICO is planning on being more lax with credit scores. Also, it should tell you about the underlying health of the economy when a large portion of your borrowers have marginal credit.

The new-new with subprime

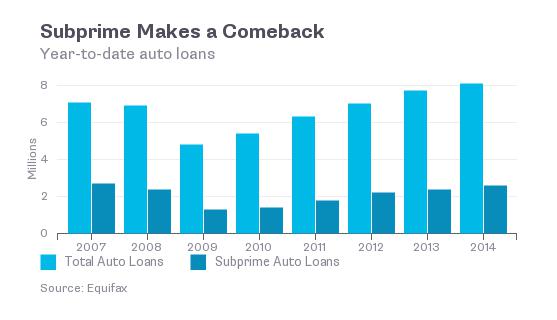

Subprime debt is the new-new in the credit markets. What is telling here is that much of this debt growth has occurred under the umbrella of recovery. If things are going so well, then why are so many loans being made to those with bad credit? Bad credit at least by the measurement tool we use, typically reflects an inability to meet payments or manage money. Yet here we are, expanding more debt to those to lease or purchase cars beyond their means. At least with a home, you had the chance to build some sort of equity but a car loses value the instant you step into the driver’s seat. Take a look at this market:

Notice how the growth is occurring during the supposed recovery? So it should come as no shock that repossession are surging:

“(NBC News) The repo man is getting very busy as a growing number of car and truck owners are struggling to make their monthly auto loan payments. Experian, which analyses millions of auto loans, said Wednesday that the percentage of those loans that were delinquent or ended up in default with the vehicle being repossessed surged in the second quarter of this year. The rate of repossessions jumped 70.2 percent in the second quarter, with much of that increase coming from finance companies not run by automakers, banks or credit unions. Even with that rise, the percentage of auto loans that end in default is just 0.62 percent of all auto loans.â€

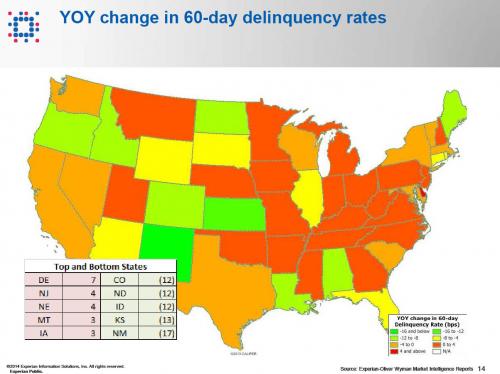

This is to be expected. Riskier loans. Riskier payoff. And when we look at the underlying data we will find that many states are seeing troubling delinquency rates:

“(Equifax) The total number of new loans originated year-to-date through June for subprime borrowers, defined as consumers with Equifax Risk Scores of 640 or lower, is 3.9 million, representing 31.2% of all auto loans originated this year. This is a slight decrease in share from this same time in 2013.â€

Essentially a core group of borrowers on new auto loans is coming from the subprime variety. Of course some pundits would like to point out that this is a “small†portion of the total auto loan market. This argument has parallels to what we heard about subprime debt in housing. These are your super marginal borrowers. But don’t think the typical American with a job making roughly $26,000 per year is in good shape either. Problems cascade from the bottom up. The economy for most Americans is struggling so it should be no surprise that the new growth market is subprime auto debt. Now, most can’t afford a home so at least you’ll get a car, even if you can’t afford a car as well.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

5 Comments on this post

Trackbacks

-

Ame said:

Let’s just hope for the sake of those who took out these sub-prime loans in order to have a car to get to a job, that they were able to save enough from that job to purchase a used car outright before the repo guy shows up! Public transportation isn’t the answer for most when it comes to getting to a job (and daycare and the doctors and home) on time.

Has anyone seen the movie, “The Pursuit of Happyness”? It stars Will Smith. Watch how well public transportation works for him.October 8th, 2014 at 8:36 am -

Archy Don said:

With all these bubbles in play, I’m reminded of the old Laurence Welk show where champagne bubbles abounded.

October 8th, 2014 at 10:11 am -

Tom said:

Credit scores are becoming more and more irrelevant every year.

How can you factor in a “global economy” into a credit score?

Looking at the big picture we need to get O-U-T of all those rotten “free trade” deals that *The American People never asked for!*October 8th, 2014 at 9:37 pm -

james said:

Go on give me a job,look at my car.

October 9th, 2014 at 3:46 am -

nicholw said:

Quite ironic to see so many more bums begging on major roadways while everyone else is listening to their favorite tune behind the wheel of their new car. How different are they really?

October 21st, 2014 at 9:25 am