How to live on $25,000 a year in low wage America:Â A guide to living on the per capita income.

- 11 Comment

Most Americans live paycheck to paycheck. We hear stories of people waiting until midnight at the end of the month so accounts can get filled with funds simply to buy food. This shouldn’t come as a shock given the per capita income of a working American is roughly $25,000. Does that seem like a lot or a little? Well we are going to find out in this article when we actually look at a full monthly budget at this level. Most Americans don’t have money saved for retirement because most of the living expenses are already eaten up by simply being alive.

Living on $25,000 a year

It feels like budgeting has a negative connotation in our society. It almost feels like it fits into the category of dieting or exercising when these things should be embraced. It is rather apparent that budgeting is simply one of those things that people choose to avoid or ignore when they probably would benefit if they took the time to it.

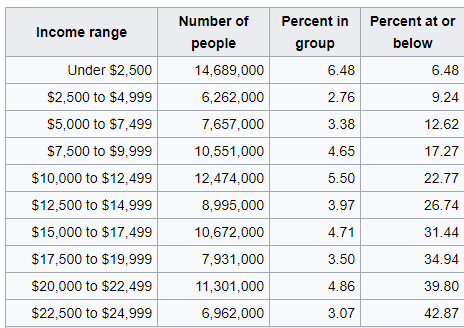

Looking at income data, we find that nearly half of individual workers make around $25,000 a year or less in reportable income:

Source:Â US Census Bureau

That is a big portion of our country. We are looking at nearly 100 million workers in this country having reportable income of $25,000 a year or less. So it might be difficult to save for retirement or even buy a home when you are simply trying to get by.

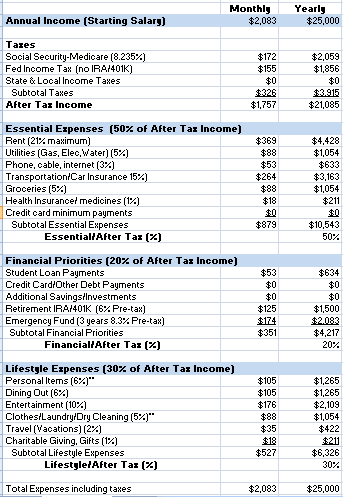

Now let us say you earn $25,000 a year. How does your monthly spending look like? Here is a sample budget for someone making $25,000 a year:

Let us go through the sections above.

Annual Income: After taxes, you are probably going to take home $1,757 a month. So right off the bat your pool of funds has lowered.

Essential expenses: You probably need to get a roommate here if you want to keep your housing expenses down. Car expenses are necessary for many just to get to work and it should not be a surprise that subprime auto debt has been one of the fastest growing debt sectors in the last few years.

Financial Priorities: Many young people now carry student debt. The nation has $1.4 trillion in outstanding student debt. We are also putting a tiny bit away into an IRA or 401k and some money for an emergency fund.

Lifestyle expenses: We’re trying to keep these things to a minimum here. We’ve discussed that for the first time last year, people are spending more on eating out than on groceries.

You hear nonsense like young people are living off of avocado toast and expensive lattes but does the above seem excessive? I really don’t see it. But then again, you have people thinking that $250,000 of income a year is middle class when it clearly puts you in the top 2 percent of earners.

The above budget should give you a line by line item of where money goes for most workers. 100 million people don’t need a budget to tell them this since they are living it today in America.

![]() If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!   Â

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!   Â

11 Comments on this post

Trackbacks

-

Princess Luna said:

That budget is unrealistic for someone making $25k/year. Most people in that low income bracket spend 33% to 50% of their income on housing (mortgage payment or, more often, rent). They have NO emergency fund and do NOT save for retirement. The cost of housing is way too high for them to be able to do such “frivolous” things. Such things seem “frivolous” because when the choice is between saving for retirement and living under a bridge or not saving for retirement and living in a ghetto apartment, most people choose the second option.

If someone is making $25k/year they need to rent a place with roommates while they ALL try to save for a down payment on a house. Unfortunately this is beneath most Americans. When you’re living in a hole, you’ve got to do EVERYTHING you can to climb out of that hole. That includes making sacrifices. If 5 people making $25k/year rented a crappy house or apartment for $1,000/month then they could afford to all save up for a down payment on a house. Then they would ALL buy the house together and start building equity while putting everything down on the house that they could. Then once there was enough equity build up, they would use that equity as a down payment on another house and rent out their old one, making their living expenses FREE. Rinse and repeat. In 20 years they would all be making at least $5k/month in passive income.

July 9th, 2017 at 3:09 pm -

Cindy Long said:

Some folks are using Uber instead of owning a car,riding a bicycle or motorcycle.Depending on how far you live from your job(s).

Eating out has increased,restaurants stay busy-breakfast,lunch and dinner.

For me,I dont have cable,internet nor student loans.Went to work right out of high school,invested in company 401k plan,shop at thrift stores,Aldis etc.

Got laid off to corporate restructuring,lived off of savings,sold off stuff I didnt need and one month later-get another job.As far as unemployment –still waiting for it to kick in….July 10th, 2017 at 4:40 am -

roddy6667 said:

It can be done. Five years ago my wife and I were getting ready to retire. We lived in CT, not the cheapest place. We lived on $30K a year (2 people) and saved the rest of our net income. We had a reliable, presentable used car with no payments, we lived in a decent apartment, and took vacations to China every other year. We were also generous to family members in China. We ate well, almost never outside the home, bringing lunches to work. We don’t drink or smoke. On weekends we would often go antiquing in Vermont or New Hampshire. We had absolutely no debt.

It can be done. Now we are comfortably retired and have money to travel.July 10th, 2017 at 5:50 pm -

Randy said:

Are you nuts rent $369, utilities $88, groceries $88. When are you living in the eighties. You better double that rent. Triple that utilities and quadruple them groceries. I see your out of touch of reality.

July 12th, 2017 at 6:10 am -

CJS said:

Based on SSA data “about 67.2 percent of wage earners had net compensation less than or equal to the $44,569.20 raw average wage. By definition, 50 percent of wage earners had net compensation less than or equal to the median wage, which is estimated to be $28,851.21 for 2014.†And “about 67.4 percent of wage earners had net compensation less than or equal to the $46,119.78 raw average wage. By definition, 50 percent of wage earners had net compensation less than or equal to the median wage, which is estimated to be $29,930.13 for 2015.” A 3.74% increase in paid wage earnings of medium wage earner.

The source of the numbers: [ https://www.ssa.gov/OACT/COLA/awidevelop.html ; then you must click “Go” to see the numbers. Data for 2016 will be available in mid October 2017. ]. For the math challenged, this will be difficult to realize. The $55,775 is the national median HOUSEHOLD income. The point being, most of you did not missout when you consider real wage earnings.

Earned income is the income of an individual, the household income is the income of the family and that also explains the difference between household income and earned wages.

♡ The following are some of the numbers that really stood out for me…

ⶠ38 percent of all American workers made less than $20,000 last year.

â· 51 percent of all American workers made less than $30,000 last year.

⸠62 percent of all American workers made less than $40,000 last year.

â¹ 71 percent of all American workers made less than $50,000 last year.Earned income is the income of an individual, the household income is the income of the family and that also explains the difference between household income and earned wages.

July 12th, 2017 at 7:17 pm -

Carlos said:

Really do need help to make it on 25k. Median house hold income at $55k just about covers the bill.

July 12th, 2017 at 8:01 pm -

Abrams said:

As Randy said, this budget only works for a single college age types..lol Here in lower Alabama, $12/hr is not an uncommon wage. (LPN with 10 years of experience gets you about $15/hr) Double it for two adults and add two kids.

Wally world store brand groceries for 4 run at least $600/mo. Healthcare for $18/mo.? … Thats a bottle of Advil and some cough syrup, not to mention less than the copay on a doctor visit. I’m pretty sure even $25k puts you above most of the welfare healthcare options. Our insurance for my family of 4 is about $1150/mo this year. I could get it for less, but risk being bankrupted if anyone gets sick or has an accident.

Bottom line… $25K will pay for the ‘Monk Life”, which is fine if you are moving your way up in the world , but there are a huge number of folks making a similar wage as thier “living wage” who have no place to go. Thier budgets look very different… lol

July 13th, 2017 at 7:10 am -

Someone said:

The rent and grocery numbers are not realistic. If you could find someone on the same page as you it is doable to save some money for something in the future. I don’t think its an issue of beneath someone to have a roommate but its had to find someone with some sense at times.

July 14th, 2017 at 4:23 pm -

roddy6667 said:

Why are people who make $25K a year having children? They can’t support themselves. Don’t they know where babies come from?

July 14th, 2017 at 6:19 pm -

wilton said:

hi……can you give me a sample of Budget Plan and Budget Analysis

July 19th, 2020 at 3:47 pm -

Donna c said:

I live in a paid for rv in a rv park. lot rent includes utilities $420 a month. car was $1700 and is paid for. I am 47 husband is 56 (on disability)kids are grown.his vehicle is paid for. we get $400 a month in food stamps. i make about $28,000 a year. if we lived in a house $1500 month we would have a hard time paying all the bills.

November 6th, 2020 at 5:50 pm