The most educated and indebted generation ever – Average student debt has tripled since 1990 while earnings have gone stagnant for college graduates. How much is the college rite of passage worth?

- 3 Comment

Most have very fond memories of their college going years. Going off to college is one of the few rites of passage that we have in the United States ushering future generations into official adulthood. Yet the cost to attend this passage has gotten astronomically expensive. College has now turned into a very large business funded by deep levels of student debt. In the past, the state took on a larger role with public universities but with state budgets in shambles these are now becoming much more expensive options. We speak of the student debt problem as a nationwide issue but this crisis is really a burden largely shouldered by our young. Poor Americans aspiring to go to college have to walk cautiously on this passage and avoid paper mill for-profits and going into massive student debt. This rite of passage is now turning into a debt filled nightmare.

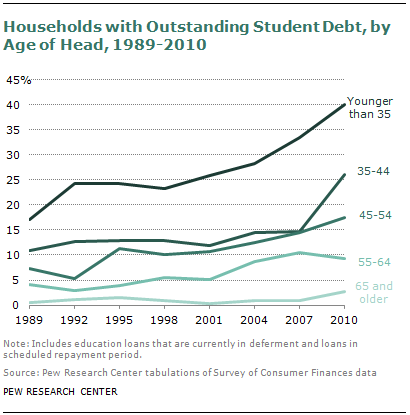

Student debt by age

While we speak of student debt as some sort of “we†problem, it largely falls on the shoulders of the young:

Of baby boomer households, less than 10 percent carry any sort of student debt. Not only do they carry a lower debt load they also went to school at a time when college education was affordable and people were graduating into a healthy job market. Take a look at the chart carefully and you will see that over 40 percent of households under the age of 35 have student debt. There is a big difference between carrying $5,000 in student debt and $50,000.

The burden has only gotten larger in recent years as incomes have gone stagnant:

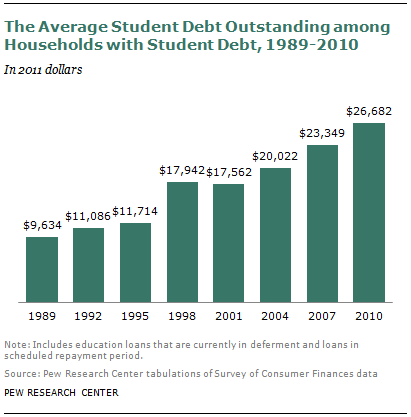

The average student debt has more than tripled since 1989. A good way to measure this is by looking at median household income:

1990 median household income:Â Â Â Â Â Â Â Â Â Â Â Â Â $30,000

Average student debt:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $9,634

Ratio:Â Â 3.11

2012 median household income:Â Â Â Â Â Â Â Â Â Â Â Â Â $50,000

Average student debt:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $26,682

Raito:Â Â Â 1.8

The real cost of going to college has gotten much more expensive. If incomes kept pace with college costs the median household income would be above $90,000.

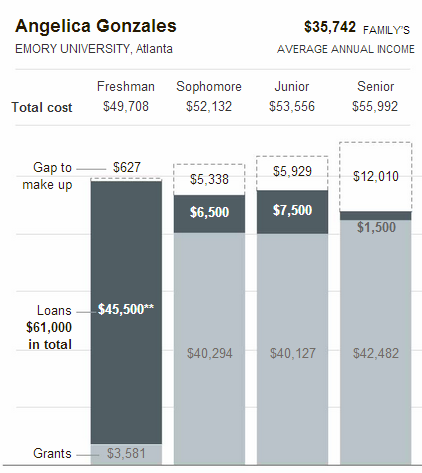

Student debt example

Many lower income students are lured into the for-profit machinery that simply survives courtesy of Federal government student debt. These institutions are mired with poor outcomes and are largely designed as efficient operations to draw in students and extract as much federal loan money from them as soon as possible. Yet this is only one part of the higher education market making up one out of ten students. Even at good institutions students can fall between the cracks. The New York Times did an in depth piece on college and the pitfalls for many lower income Americans. Here is one example given:

While the article explores the pitfalls for poor students, it does not go into the details of how middle class students are crushed on these sliding scale financial aid models. In the above example, the student did not clearly report her financial situation and because of this, ended up needing to take $45,500 in loans for year one of her education. Once things were clarified most of the funding was covered by grants.

Yet look at the actual cost. From the first year of attendance at $49,708 the cost went up to $55,992 by the student’s senior year. This is a recent story. What in the last few years has justified a more than 10 percent increase in cost to attend Emory? The answer is that all institutions are simply hiking costs up and adjusting the true cost at the back end. For example, a middle class family with an average student might end up paying the full bill while a lower income student like the case above will have grants covering most of their costs. Colleges do this because it gives them more leeway to extract funds from loans and other forms of payment.

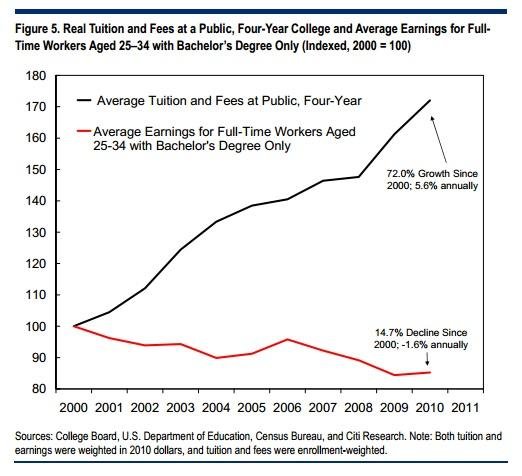

Earnings

It would be one thing if earnings were keeping up with the rise in tuition and other costs to attend college:

This is probably one of the more telling charts. Since 2000 average tuition and fees at public institutions has gone up by 72 percent while earnings for those with a college degree between 25 and 34 has fallen by 14.7 percent. This is the age group that is carrying the heaviest burden of the $1 trillion in outstanding student loan debt.

One of the more frustrating aspects of the coverage on the student debt bubble is that you hear facts about lifetime earnings for college graduates. Sure. This makes sense because these are people that went to college during very affordable times, graduated into a healthy economy, and didn’t have to worry about entering a for-profit paper mill that would drain out $20,000 a year for a piece of paper. There is little risk when you receive a B.A. in English from a state school years ago and graduate with say $1,000 in debt versus coming out today with $75,000 in debt and trying to find work in our low wage economy.

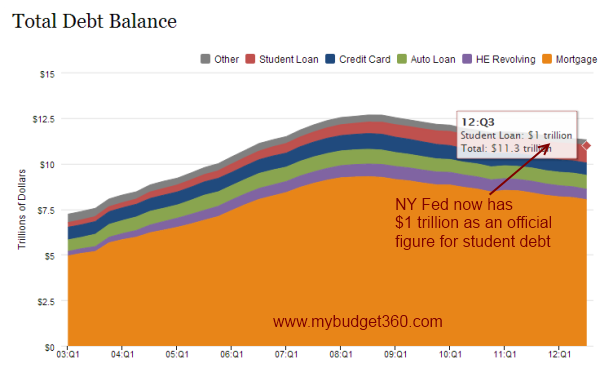

Total debt

Averages are incredibly misleading. Most of the $1 trillion in student debt has come after 2000. We went from roughly $200 billion in student debt to over $1 trillion in about a decade. A big leap has also occurred since the crisis hit:

While overall households have been deleveraging because the crisis student debt has gone from $600 billion in 2008 to a startling $1 trillion in the last quarter (the Fed now officially has the $1 trillion mark on their own charts). This is a raging bubble. It will pop. There is a limit now as to how high prices can go without any discernible increase in wages. Bubbles are hard to spot but common sense needs to prevail at times. Like with housing, just because people had access to easy debt with no income verification prices kept being pushed higher as long as the debt market was there. What happens when it pops? The government basically is the higher education market for public institutions and certainly the for-profits. Elite schools will draw from many that can pay and others that are willing to go into debt for the experience. Yet this rite of passage is now starting to have the signs of a mania. More and more students are defaulting. Many are unable to service their debt payments. Income based repayment plans may defer payments deep into the future but that only means that problems are pushed out a few more years. We have about ten cans that we are now kicking down the road. At a certain point, you run out of cans and with $1 trillion in student debt floating in the market the clock is ticking on this bubble.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!3 Comments on this post

Trackbacks

-

stephen verchinski said:

If the elite in this country don’t get real with wage depreciation, they will cause another crash. With wages declining downward due to Right to Work and corporate giveaways it is not getting easier to discharge the debt but harder. Many graduates, since bankruptcy is out of the question some.may not renounce citizenship but could.be leaving for countries like OZ and New Zealand where the skills are needed and gaining citizenship is easy. What are those countries positions on those escaping paying off student loans would be a good question to research. Have we stopped anyone from coming back to the USA after failure to pay off a student loan?

December 26th, 2012 at 6:52 am -

Celia S. said:

Big government has inflated the costs of college by providing billions in taxpayer funded subsidized loans and grants to colleges and universities. $1 trillion in student debt has come after 2000? It’s crazy!

December 26th, 2012 at 1:28 pm -

Dagny said:

I see the young, indebted, low wage earning folks as a growing force for yet more inflationary action from the USGov+USFed.

December 27th, 2012 at 7:04 am