Crony capitalism and the cult of borrowing: As the banking sector is fully bailed out, Americans push aside history and begin to leverage into debt to compensate for stagnant wages.

- 1 Comment

Banking should operate as a utility by providing businesses and consumers a source of funds for projects that will add real growth in the real economy. Unfortunately, the current banking system favors speculation and banking for the sake of banking. It also favors creating a non-working class that merely lives off of speculation and their easy access to debt. For example, many banks used special privileges with the Federal Reserve to borrow cheaply, take over other firms with incredibly generous benefits, and ultimately were never made accountable to the public by being saved. There have been multiple examples as to how these bailouts have failed the American public. Americans continue to face a dwindling middle class. We have a plethora of low wage jobs, little benefits, and a financial system that forces people into massive debt. Going to college has put Americans into $1.2 trillion of student debt. Buying a home is only feasible for most Americans with a low down payment since they hardly have any savings. Banks are paying ridiculously low interest rates on savings accounts making it unattractive to save and plan for a rainy day. It is no surprise that borrowing on credit cards is up again. Yet many banks are seeing peak bonuses, peak profits, and peak cronyism.

Household debt and wages

It is hard to pinpoint a time when the middle class started collapsing but the late 1970s is a good starting point. At that time, household debt was equivalent to annual wages paid out. This is a good indicator of ability to pay. For example, say a family makes $50,000 a year the total debt they would have is $50,000 in debt. This figure has been blown out of the water starting a generation ago as the system became fully financialized. People started borrowing more than they made.

Banks turned housing into a speculative commodity. Going to college for most is only feasible by going into debt. The days of “I worked mowing lawns to pay for my school†are long gone. How many lawns will you need to mow for $25,000 in tuition per year?

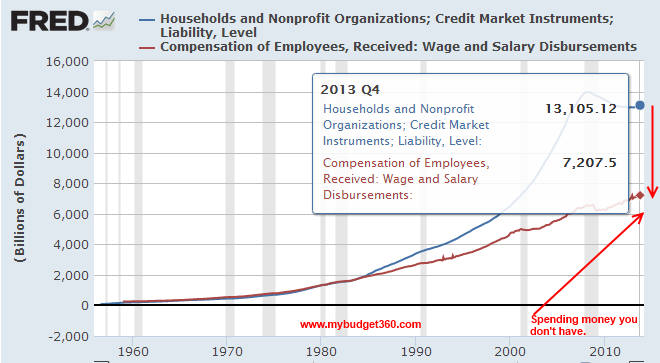

If we look at wages and debt we realize many Americans simply are borrowing (from banks) to keep up a middle class life:

While total wages earned came in around $7.2 trillion Americans are in debt to the tune of $13.1 trillion. We are borrowing way more than we are making. Of course, the financial system is betting on keeping the stock market hot and actions taken by the Fed have made it disastrous for a regular family to save in a regular traditional savings account.

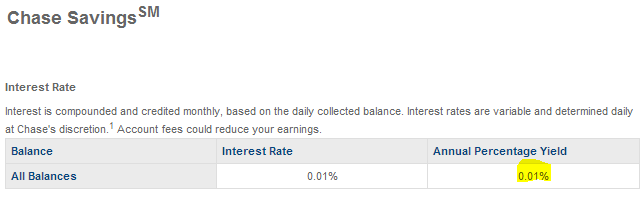

Take a look at the current interest rate on one savings account which is similar to most major banks:

With inflation running at 2 to 3 percent based on headline numbers, you are actually losing money by keeping it in the bank. 1 out of 3 Americans actually has no savings which is a bigger problem in itself. So why are Americans going into so much debt?

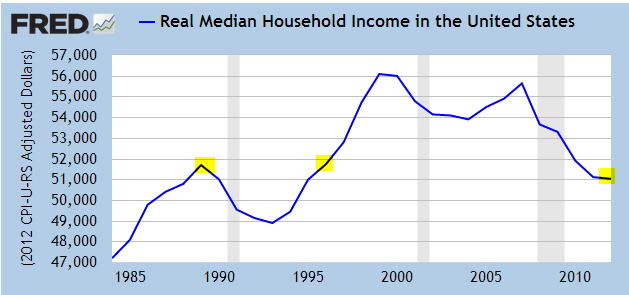

Americans are going into debt because of stagnant household wages:

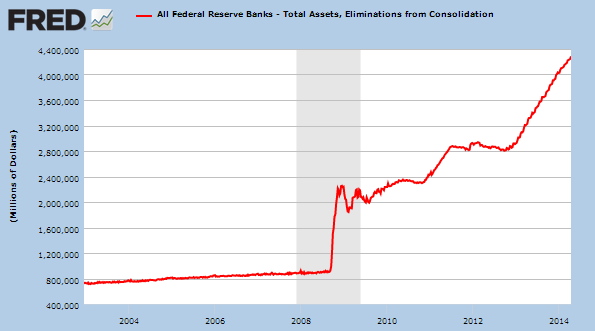

Then what big benefit was brought on by the banking bailouts? Many banks including JP Morgan Chase now see their stock price at levels higher than they were during the banking insanity of 2007. Multi-million dollar bonuses are being handed out as if they have done something great for the economy. Do you need to be a genius to offer a 0.01 savings account interest rate and then turn around and offer a 14.99 interest rate credit card? You have high rates on auto loans and mortgages since you are basically being guaranteed by the government. Yet mortgages today are all backed by the Fed and the risk is being transferred to their balance sheets, not banks:

In essence, banks have a hedge where they can’t lose but the public is eating the cost through inflation, lack of access to quality credit, and now having to compete for houses against big bank investors. Many of these bank investors just want to buy homes to rent out or flip at higher prices but how does this really help the economy? Higher home prices including higher rents only suck more money out of the pockets of Americans without putting anything back. It is dubious to see what benefit this does aside from increasing their wealth that is already aggregated in the hands of a few.

We are in an era of crony capitalism. The bailouts were politically structured to help banks for their major benefit and the public was only a secondary thought. Now that banks have eaten at the trough, they are allowing Americans to borrow again but wage growth is non-existent so what use is that? That is what led us to the first crisis. Massive banking speculation, a public borrowing money they don’t have, and rampant cronyism in our financial system. The political system is broken and most Americans have little faith in it. The current system appears to be setup as a way to funnel money into politics to keep some legislatures paid and powerful firms in power for the sake of protecting their own interest even if their interests are bad for the country overall. In other words, we are seeing the structure that led us into the Great Recession still in place and replaying the same old card.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!1 Comments on this post

Trackbacks

-

rolf said:

bring back the OTTOMAN EMPIRE

June 18th, 2014 at 5:03 pm