Paycheck to paycheck and food stamp to food stamp: Study finds 3 out of 4 Americans are one financial emergency away from being out on the street.

- 3 Comment

The latest food stamp usage data was released with very little attention from the media. 47.7 million Americans are on food assistance spanning a record 23.1 million families. Americans on food stamps reflects deep structural issues in the way our economy employs our population. The recovery in many parts of the US is anything but. What we are seeing is a growing (and permanent) class of people that will be part of a working (and growing non-working) poor segment of our population. You would think with the proliferation of information that more opportunities would arise but many people are not keeping up. There was also a survey showing that 3 out of 4 Americans are basically living paycheck to paycheck with 1 out of 4 living without any savings at all. You would think this economic dilemma would make headline news but it doesn’t. Is a paycheck to paycheck and food stamp to food stamp nation worth reporting on?

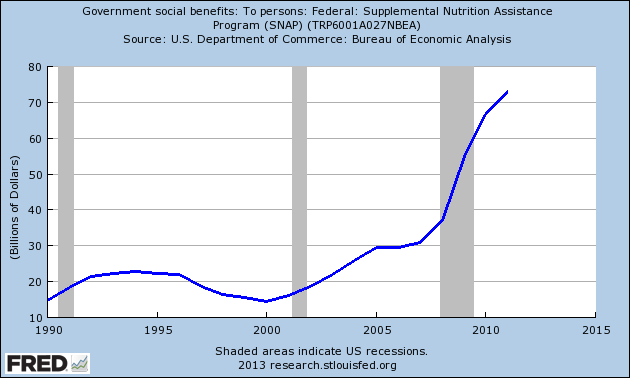

Food stamp payouts at record levels

I’ve been tracking the nominal amount of money being paid out to food stamp participants and we are at a record level:

Over $70 billion a year is going out in food stamps. The high elevation of payouts is showing that many people simply cannot get off of this because of the lack of employment or the lack of opportunities in the current marketplace. A large number on food stamps are also going to the working poor. Tracking this data shows that the recovery has largely been a no show for a giant section of our population. Many of these people camp out at dollar stores or Wal-Mart waiting at the end of the month simply to see their debit cards refill so they can purchase food for their family. The typical payout per family? $276 per month.

Paycheck to paycheck

Another recent study on the ridiculously low amount of savings for Americans was released:

“(CNN Money) Fewer than one in four Americans have enough money in their savings account to cover at least six months of expenses, enough to help cushion the blow of a job loss, medical emergency or some other unexpected event, according to the survey of 1,000 adults. Meanwhile, 50% of those surveyed have less than a three-month cushion and 27% had no savings at all.â€

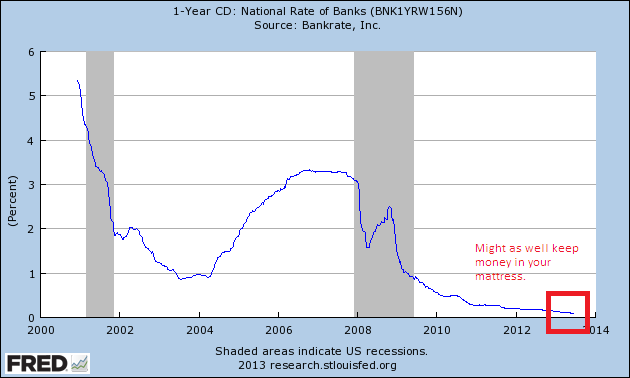

50 percent have just enough for three months of expenses while another 27 percent are literally living paycheck to paycheck. One of the main reasons for this lack of savings is the current banking environment we are living in. There is very little incentive to save when banks are paying nearly zero percent on deposits and CDs:

This is done purposefully. The Fed is setting up an environment where savers are punished and it should be no surprise that people are not saving because they can’t or simply have very little incentive to do so. We now find ourselves in an economy where living paycheck to paycheck is very common. What does that say about the recovery however?

We discussed this market and how it has setup a two-income household trap for many:

The vast majority of Americans have two-income households not because they want to but because of economic necessity. Over the last few decades with more people working the household income figures have gone up but strip this out and per capita wage growth has actually fallen inflation adjusted for over a decade.

Is this paycheck to food stamp recovery really a recovery? Â The Fed has ensured that as long as people have access to insane levels of debt (more directed to the banking system and their speculation) then the wheels will keep on turning.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

3 Comments on this post

Trackbacks

-

Terry Pratt said:

Food stamps are based on income minus (out of pocket housing + medical expenses), which a 20% disregard of earned income, which helps the working poor.

Because very few of the working poor own homes, food stamp payments tend to rise with rents, and rents in many area have soared since the so-called housing recovery started, so I see more increase before food stamp usage starts to fall.

June 26th, 2013 at 10:51 am -

nubwaxer said:

the war on the poor has gutted the middle class and driven wages down across the board for half of america.

June 26th, 2013 at 12:28 pm -

Gary Reber said:

Surprised? Oh really. This is more bad news for the propertyless masses, who are faced with decreasing JOB opportunities and the worth of labor devalued as the productiveness of the non-human contribution exponentially grows, but owned by a wealthy minority.

The reality is that the notion that JOBS ONLY is the solution to America’s economic decline is mis-guided. Why, simply because the function of technology is to “save” labor ––eliminate unnecessary labor costs and employ people at the lowest possible cost. Full employment is not an objective of businesses. Companies strive to keep labor input and other costs at a minimum. Private sector job creation in numbers that match the pool of people willing and able to work is constantly being eroded by physical productive capital’s ever increasing role.

There is no solace in the statistics. Researchers at the American Enterprise Institute and the Center for Economic and Policy Research shows that a worker between the ages of 50 and 61 unemployed for over a year has only a 9 percent chance of finding a job in the next three months and only a 6 percent chance if he or she is 62 years or older. According to the Economic Policy Institute, there are approximately 3.3 unemployed workers for every job seeker.

Because for the vast majority of Americans a JOB is their ONLY source of income, millions of families are one layoff or family emergency away from going into bankruptcy, and then what? Start over with nothing and extremely poor JOB prospects.

The American Dream is fast disappearing as people experience fewer opportunities to earn an income, and as a consequence cannot act as “customers with money” necessary to support a vibrant economy. The result is a permanent national recession at the brink of a second Great Depression.

Unfortunately, our political leaders, academia, and the national media offer up ONLY the same old conventional won’t-work suggestions for the government to take the lead and arrange the marriage of private and public capital to regenerate real growth without the realization and requirement that the ownership of FUTURE wealth-creating productive capital must be broad. No longer can we be able to achieve growth the old-fashioned way, by investing in projects that enrich our productive capacity in the name of JOB CREATION, which is expected to have a multiplier effect, when in actual reality such investment continues to further CONCENTRATED OWNERSHIP of America’s future productive capital assets.

The ONLY viable solution to the economic decline of America is for our leaders, academia and the national media to recognize that all individuals to be adequately productive cannot do so when a tiny minority (capital owners) produce a major share and the vast majority (labor workers), a minor share of total output of the economy’s products and services. The system must be reformed to create a world in which the most productive factor of the FUTURE—physical capital—now owned by a handful of people––is owned by a majority—and ultimately 100 percent—of the consumers, while respecting all the constitutional rights of present capital owners.

A balanced Just Third Way approach to building a FUTURE economy that supports affluence for EVERY American is presently not in the national discussion. It appears that the President of the United States, the elected Congressional representatives and Senators, academia, and the media are oblivious to this principled solution that has the ingredients to power economic growth at double-digit GNP rates.

This goal requires investment in FUTURE wealth-creating, income-producing productive capital assets while simultaneously broadening private, individual ownership of the resulting expansion of existing large corporations and future corporations. Not only is employee ownership the norm to be sought wherever there are workers but beyond employee ownership the norm should be to create an OWNERSHIP CULTURE whereby EVERY American can benefit financially by owning a SUPER IRA-TYPE Capital Homestead Account (CHA) portfolio of income-producing, full-voting, full-dividend payout securities in America’s expanding corporations and those newly created to produce the future products and services needed and wanted by society.

Those who read this and are in a position of influence should reach out to President Obama and the leadership of his Organizing for Action as well as to other political leaders, and call for them to convene a national discussion using the national media and social media, and our educational institutions, to open up a discussion on EVERY CITIZEN AN OWNER opportunity. We need fresh and inspired leaders who can educate on this issue at this time because academia, the media, and our so-called leaders are not addressing how people make money and the significance of OWNING income-producing productive capital assets. We need to get people to understand that as with today, in the FUTURE we will continue to experience tectonic shifts in the technologies of production, which will destroy and devalue the worth of jobs. This is a crucial understanding because at present for the 99 percent of the nation a JOB is the ONLY source of income to support themselves and their families. We need political leaders who will commit to a government policy focus on OWNERSHIP CREATION, not JOB CREATION, which will result and naturally follow as the economy revs up to double-digit GDP growth and fully applies technological innovation and invention to shift from unnecessary labor toil to human-intelligent machines, super-automation, robotics, and digital computerized operations. The Federal Reserve needs to stop monetizing unproductive debt, and begin creating an asset-backed currency that could enable every child, woman and man to establish a Capital Homestead Account or “CHA” at their local bank to acquire a growing dividend-bearing stock portfolio to supplement their incomes from work and all other sources of income. Steadily over time this will create a robust economy with millions of “customers with money” to purchase the products and services that are needed and wanted.

Our leaders need to put on the table for national discussion this SUPER-IRA idea and the necessary reform of our tax policies that would incentivize corporations to pay out fully their earnings in the form of dividend income and issue and sell new stock to grow. The CHA would process an equal allocation of productive credit to every citizen exclusively for purchasing full-dividend payout shares in companies needing funds for growing the economy and private sector jobs for local, national and global markets,

The shares would be purchased on credit wholly backed by projected “future savings” in the form of new productive capital assets with future marketable products and services produced by the newly added technology, renewable energy systems, plant, rentable space and infrastructure added to the economy.

Risk of default on each stock acquisition loan would be covered by private sector capital credit risk insurance and reinsurance (ala the Federal Housing Administration concept), but would not require citizens to reduce their funds for consumption to purchase shares.

Essentially, the pressing need is for everyone in a position of influence to encourage President Obama to raise the consciousness of the America people by making his NUMBER ONE focus the introduction of a National Right To Capital Ownership Bill that restores the American dream of property ownership as a primary source of personal wealth.

This is the solution to America’s economic decline in wealth and income inequality, which will result in double-digit economic growth and simultaneously broaden private, individual ownership so that EVERY American’s income significantly grows, providing the means to support themselves and their families with an affluent lifestyle. The Just Third Way Master Plan for America’s future is published at http://foreconomicjustice.org/?p=5797.

Support the Capital Homestead Act at http://www.cesj.org/homestead/index.htm and http://www.cesj.org/homestead/summary-cha.htm

June 28th, 2013 at 11:18 am