The Millennial Conundrum: Millennials are bogged down by massive student debt and confiscatory housing prices.

- 2 Comment

Millennials are a critical group in terms of where the economy goes in the next few years. The economy largely relies on younger people to spend and purchase consumption items. Think of a young couple buying their first home. That in itself is a big purchase. Then comes big ticket items like refrigerators, a family car, bed, television, and all the trappings of filling a home. Baby boomers followed a very clear script when it came to this consumption behavior. Millennials on the other hand have not. They are largely constrained by a couple of major things that simply were not tied to the previous generation. And what could those be? Millennials are bogged down by student debt and confiscatory housing prices.

Housing

Millennials seem to get blamed for a lot in the media. Yet this just seems to go hand in hand with the typical practice of blaming younger people that has occurred for a centuries. One of the big challenges Millennials face is that of purchasing a home. Well how can someone make the biggest purchase of their lives if they don’t have a good paying job or money saved up?

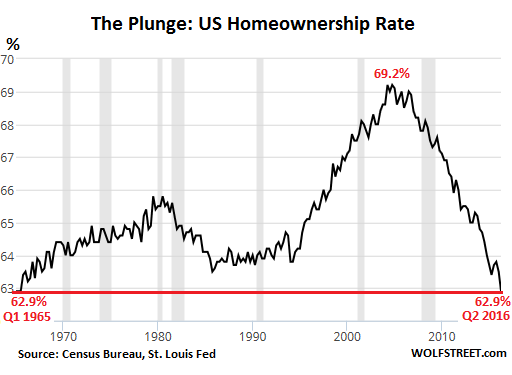

This trend is deeply problematic to the market since housing drives a good portion of GDP. Many younger Americans are having a tough time paying rising rents and home prices have been inflated by short supply and investor activity. The end result is a generationally low homeownership rate:

Many Millennials live at home because rent is too high and they have another large albatross around their necks. That heavy weight comes in the form of student debt.

The college albatross

There is now $1.4 trillion in student debt outstanding. That number is simply mind boggling. When Millennials get blamed for not stimulating the economy the media largely forgets to mention that many younger Americans are carrying a heavy burden of debt already. This is the equivalent of having 20 maxed out credit cards before you even have your first job.

And college has become a gateway into many middle class jobs: computer programming, accounting, nursing, teaching, and engineering just to name a few. There simply isn’t the massive amount of blue collar work that pays well like it did during the baby boomer generation. This ties in directly to home buying and purchasing other consumer goods.

But Millennials seem to be out and about and spending money right? Well how much does eating out stimulate the economy versus buying a big ticket item or buying a home? How many times would you have to eat out to make the economic impact of buying a $225,000 home, which is a standard new home cost? That is the fundamental problem here. Millennials are having a tougher time buying the expensive life purchases that seemed to be commonplace in their parent’s life.

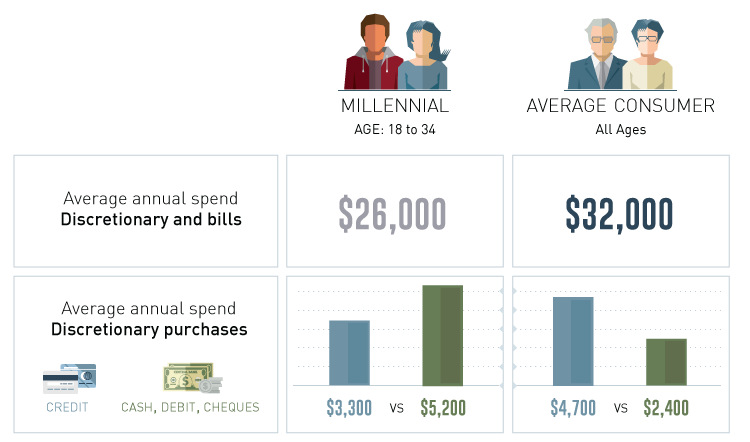

And their spending habits do cause some to pause in terms of future economic growth:

This lower spending rate might make for slower economic growth and this is looking at only two factors. What about rising healthcare costs or the burden of retirement benefits for older Americans? When you factor these things in you can only see costs rising for Millennials. That is a conundrum not only for Millennials, but the rest of the U.S. economy.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! Â

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!  2 Comments on this post

Trackbacks

-

Stephen Verchinski said:

Hey great legacy there a Boomers for the Millennials have you no shame the wars in Iraq and Afghanistan now are approaching 5 trillion dollars of debt left to the Millennials doesn’t include the aspect of the other unfunded bankster bailouts that were doing nationally and more to subsidise the corporate Elite and then there is this how do they expect the Millennials to get out from under when the upper echelon in this country are so damn greedy

October 16th, 2016 at 8:35 am -

Angle Paisa said:

The today’s era is the era of business entrepreneurship and selling own ideas and creativity. Gone are the days when people just had to rely upon their salaries, now people with good ideas and investments are diving into the ocean of entrepreneurship. What you need is thriving idea, a smart strategy and workforce to execute the ideal plan.

October 20th, 2016 at 5:56 am