The two-income trap for Americans: How dual income households are a financial necessity in a time when the median per capita wage is $27,000.

- 5 Comment

Recent Social Security data released this month revealed that income disparity is only growing in the United States. The released figures show that the median per capita wage in the US is $27,519. Given the costs for college, healthcare, and housing many households are simply falling out of the middle class. The two income household is now the common default for Americans. However, in many cases the two income household has arisen primarily for economic necessity. Many households today simply cannot get by on one income earner. Especially if a family has children, childcare is expensive and a good portion of any additional income is diverted into this expense. The decline of the middle class household would be more dramatic if it were not for the emergence of the dual income household. Given demographic trends, it appears that we have peaked in this category and many young Americans have no choice but to live in households with multiple streams of income. Many Americans learn the hard way that the two income household may actually be a trap.

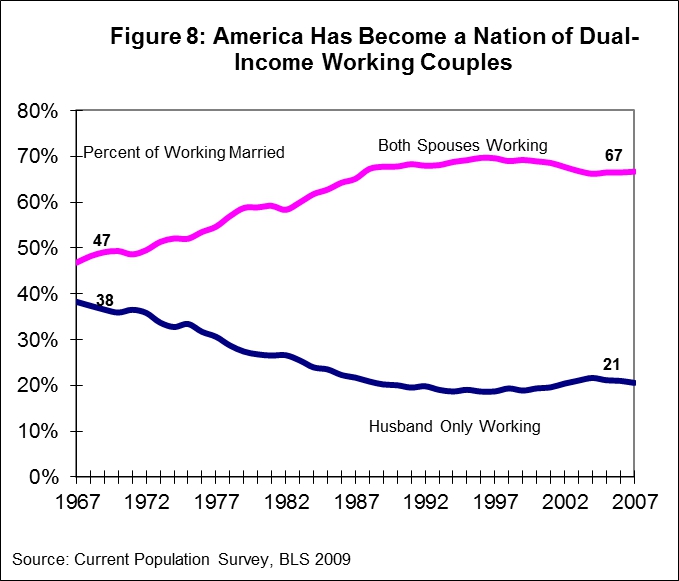

Two income trap

Inflation is an insidious form of money destruction. The Fed would like you to believe that there is only very little inflation going on but I would ask you to look at the costs of higher education, housing, cars, food, and healthcare and ask yourself if inflation is absent. Primarily because of this destruction of purchasing power a single-income household in 1970s was better off than a dual-income household in the 2000s:

This is an interesting perspective. While the nominal amount of income for a dual-income household is higher, fixed costs are also much higher. In fact, the household in the 1970s had more disposable income adjusting for inflation than the dual-income household of today. How is that possible? You have to realize that many middle class families have gone into massive debt just to keep up with what they perceive to be a middle class life. If both spouses are working and children are involved, childcare is not a cheap expense. This can eat up a good portion of any additional earned income. Also, children are not cheap and require added expenses (i.e., healthcare, school, food, etc). So you are left with this situation where a household may be earning more but in the end, discretionary income is less after expenses are factored out.

Many of these dual-income households are now witnessing their kids going off to college. There is a massive student debt bubble raging in this country. Parents are largely unable to fund the cost of their kid’s college education so many simply go into massive debt. Another trap given that many recent young graduates are finding it difficult to manage their large debt loads.

While the rise of dual-income households is not a new trend what is new is that we seem to be reaching a peak here.

Both spouses working

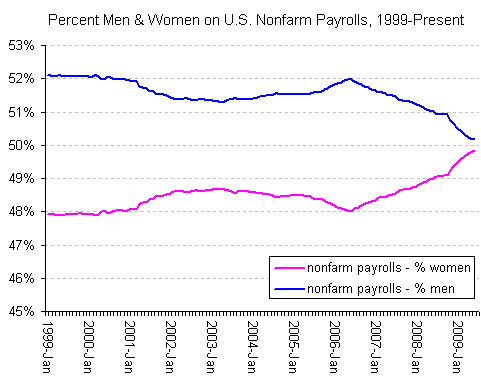

Of married couples, 67 percent are in dual-income households. This is a large jump from the 1960s. However as the chart above highlights this may have peaked sometime in the last decade. The recession has been tough on households. Given that the 2000s were the decade of the real estate bubble, many of the jobs that were lost after the crash came from fields where the majority of workers were men (i.e., construction, etc). Because of this shift after the recession, men and women are nearly equally represented in the workforce:

Many households have but no choice to have two workers. The fact that the Social Security data shows that the median per capita wage is $27,519 we then begin to realize that many Americans are simply treading water. We then have stats showing that 1 out of 3 Americans have zero saved up and that 53 percent of Americans own no stocks.

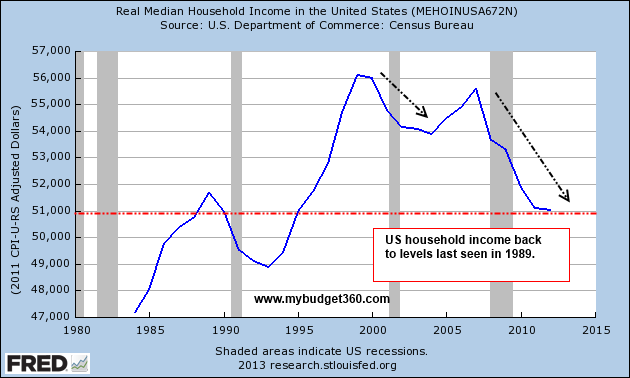

The two-income trap is real and has only become a larger phenomenon after this financial crisis. If we look at household income, adjusting for inflation it is back to where it was nearly a generation ago.

Household income

Inflation has ravaged household balance sheets especially when it comes to income:

US household income is now back to where it was in the late 1980s adjusting for inflation. Try sending your kid to a private college that costs $50,000 per year when you are only earning $50,000 a year as a household. Is it any wonder why student debt is now over $1.1 trillion? The two-income trap is a part of life for many and only reveals the slow demise of the middle class in the US. We’ve highlighted the alarmingly high number of Millennials living at home because of the current economy. Some are working thus creating households with three (or more) income streams. Yet even then, many are still just getting by. Welcome to low wage America. This dual-income trap makes sense considering the fastest growing employment sectors come in the low-wage food and entertainment fields.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

5 Comments on this post

Trackbacks

-

D Ross said:

Yep … and this two-income trick was imposed on Americans under the facile guise of feminine equality. Well, Americans, you can see what that foolery bought you.

Broken homes

Dysfunctional families

High school dropouts

An every man/woman for themselves societyIn short, the death of the “American Dream.”

November 12th, 2013 at 5:22 am -

Gary Reber said:

This is all about income, or more precisely the decline of income necessary to support oneself and a family household unit. Conventional wisdom says there is only one way to earn a living, and that’s to work. Yet job opportunities, especially that pay decent wages and salaries to support a family household unit, are constantly disappearing. Furthermore, the reality that is ignored by leadership and academia is that tectonic shifts in the technologies of production are exponentially destroying jobs and devaluing the worth of labor as “machines” replace people as the means of producing products and services.

Binary economist Louis Kelso stated: “Conventional wisdom effectively treats capital (land, structures, machines, and the like) as though it were a kind of holy water that, sprinkled on or about labor, makes it more productive. Thus, if you have a thousand people working in a factory and you increase the design and power of the machinery so that one hundred men can now do what a thousand did before, conventional wisdom says, ‘Voila! The productivity of the labor has gone up 900 percent!’ I say ‘hogwash.’ All you’ve done is wipe out 90 percent of the jobs, and even the remaining ten percent are probably sitting around pushing buttons. What the economy needs is a way of legitimately getting capital ownership into the hands of the people who now don’t have it.â€

The solution is to educate people about the source of income and wealth accumulation that makes one rich––capital ownership. Conventionally, most people do not have the right to acquire productive capital with the self-financing earnings of capital; they are left to acquire, as best as they can, with their earnings as labor workers. This is fundamentally hard to do and limiting. Thus, the most important economic right Americans need and should demand is the effective right to acquire capital with the earnings of capital. Note, though, millions of Americans own diluted stock value through the “stock market exchanges,†purchased with their earnings as labor workers, their stock holdings are relatively miniscule, as are their dividend payments compared to the top 10 percent of capital owners.

Structural reform is needed in America to significantly expand private sector individual capital ownership financed with the future earnings of investment. We need to embrace “full production” rather than “full employment.” As a result, in the relative short term “full employment” will occur because every person willing and able to work will be needed to build a future economy that will support general affluence for EVERY citizen. At the same time corporations will benefit from the populous support to keep labor input and other costs at a minimum in order to maximize profits for the owners––which will consist of both the current ownership class and a new, ever expanding ownership class that ultimately comprises EVERY citizen. With such structural reform America will be able to compete more effectively on a global basis as American corporations will be able to operate far more efficiently with less costly overhead. Such structural reform will put us on a path to prosperity, opportunity, and economic justice without taking from those who already own and destroying the principles of private property, and without having to rely on redistribution of wealth and income to support the masses needing taxpayer-supported government welfare sourced from tax extraction and national debt .

Other necessary structural reforms in addition to encouraging corporations to pay out all their profits as taxable personal incomes to avoid paying corporate income taxes and to finance their growth by issuing new full dividend payout shares for broad-based citizen ownership, would include:

• Eliminate all tax loopholes and subsidies,

• Provide an exemption of $100,000 for a family of four to meet their ordinary living needs,

• Eliminate the payroll tax on workers and their employers, but

• Pay out of general revenues for all promises for Social Security, Medicare, Medicare, government pensions, health, education, rent and subsistence vouchers for the poor until their new jobs and ownership accumulations provide new incomes to substitute for the taxpayer dollars to fill these needs.

• The tax rate would be a single rate for all incomes from all sources above the personal exemption levels so that the budget could be balanced automatically and even allow the government to pay off the growing unsustainable long-term debt, but the poor would pay the first dollar over their exemption levels as would the hedge fund operator and others now earning billions of dollars from capital gains, dividends, rents and other property incomes which under some tax proposals would be exempted from any taxes.

• As a substitute for inheritance and gift taxes, a transfer tax would be imposed on the recipients whose holdings exceeded $1 million, thus encouraging the super-rich to spread out their monopoly-sized estates to all members of their family, friends, servants and workers who helped create their fortunes, teachers, health workers, police, other public servants, military veterans, artists, the poor and the disabled.

• The Federal Reserve would stop monetizing unproductive debt, including bailouts of banks “too big to fail” and Wall Street derivatives speculators, and

• Begin creating an asset-backed currency that could enable every man, woman and child to establish a Capital Homestead Account or “CHA” (a super-IRA or asset tax-shelter for citizens) at their local bank to acquire a growing dividend-bearing stock portfolio to supplement their incomes from work and all other sources of income.

• The CHA would process an equal allocation of productive credit to every citizen exclusively for purchasing full-dividend payout shares in corporations needing funds for growing the economy and private sector jobs for local, national and global markets,

• The shares would be purchased on credit wholly backed by projected “future savings” in the form of new productive capital assets as well as the future marketable goods and services produced by the newly added technology, renewable energy systems, plant, rentable space and infrastructure added to the economy.

• Risk of default on each stock acquisition loan would be covered by private sector capital credit risk insurance and reinsurance, but

• Would not require citizens to reduce their funds for consumption to purchase shares.

The end result is that citizens would become empowered as owners to meet their own consumption needs and government would become more dependent on economically independent citizens, thus reversing current global trends where all citizens will eventually become dependent for their economic well-being on our only legitimate monopoly –– the State –– and whatever elite controls the coercive powers of government.

This is the Just Third Way (http://foreconomicjustice.org/?p=5797) advocated by the Center for Economic and Social Justice (www.cesj.org) and the essence of the proposed Capital Homestead Act at http://www.cesj.org/homestead/index.htm and http://www.cesj.org/homestead/summary-cha.htm. See the full Act at http://cesj.org/homestead/strategies/national/cha-full.pdf

November 13th, 2013 at 9:18 am -

Ametrine said:

The real dual-income trap is taking out a home mortgage using both incomes to qualify.

November 14th, 2013 at 5:28 pm -

Stephen said:

Perfect article and completely true.

August 12th, 2015 at 5:43 am -

Tom said:

I am a foreigner living in Europe.

The reason Americans are becoming poorer is because all your companies have uprooted themselves and moved elsewhere.

Lots of middle class people here now living the American Dream in Europe.

Wonder how long it will last for them?

August 30th, 2015 at 12:19 pm