The two trillion dollar towers of student and auto debt: As Americans are unable to afford homes, many go deep into debt to finance their education and cars.

- 4 Comment

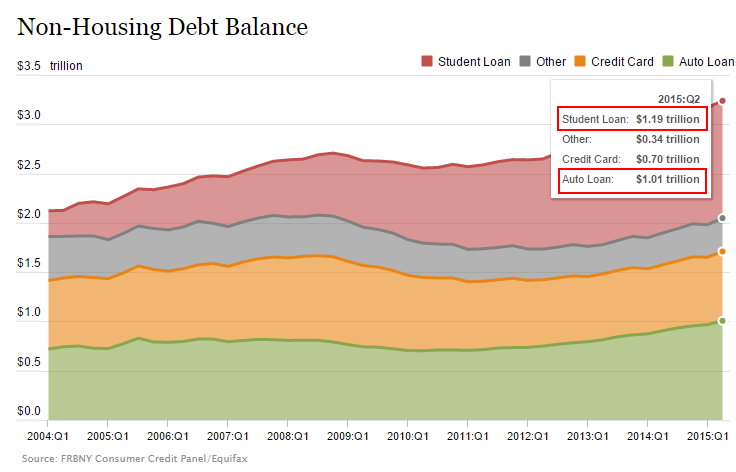

As Americans continue to see their income lag inflation, many are unable to purchase homes in a market driven by hot money and a crowding out effect brought on by investors. But people want to spend money, even money they don’t have. So instead of buying homes, Americans have been on a car buying spree and also going into deep debt for college. The end result is that we now have two trillion dollar towers of debt. Student debt outstanding is at $1.36 trillion and auto debt is now over $1.01 trillion. A large part of the rise in auto debt has come in the form of subprime auto debt. A car is not an investment. And with your typical new car costing $30,000 this is no tiny purchase given the median annual household income of $50,000. So Americans are doing what they do best and that is financing big ticket purchases to grasp at the illusion of being middle class. Let us look at what has changed in the last decade.

How we now have two trillion dollar debt sectors outside of housing

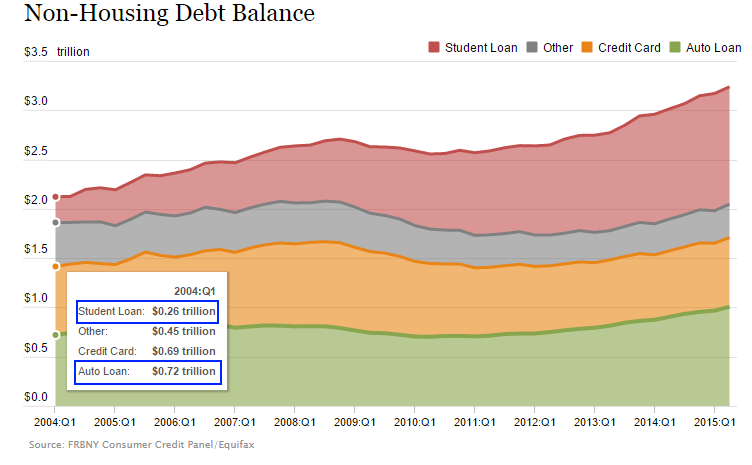

Go back in time to 2004. Every segment of non-mortgage debt was well below the $1 trillion mark. In fact, the numbers were substantially low relative to where we are at today. For student debt, in 2004 there was “only†$260 billion outstanding and auto debt stood at $720 billion. At the time this seemed high but over the next 10 years student debt grew by a stunning $1 trillion.

Now, student debt outstanding is at $1.36 trillion and auto debt is at $1.01 trillion:

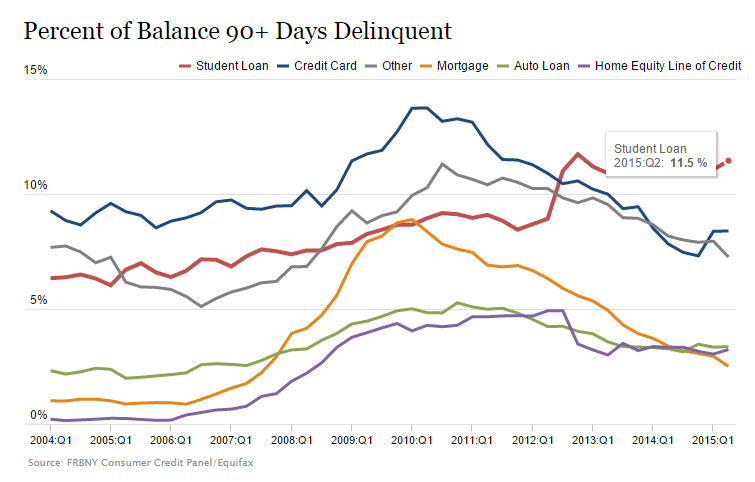

There are two important things to focus on here. The growth of auto debt did pause during the Great Recession. This was not the case for student debt which seemed to accelerate as millions decided to ride out the great crisis by going to college. Unfortunately many are finding their college degrees are simply not yielding the expected income that they thought they would earn after getting their newly minted diplomas. This is why we have seen a shift in delinquencies for various loan products.

In 2004 the worst performing loans were with credit cards and “other†kinds of loans. Today the worst performing non-mortgage debt category is clearly with student loans:

There are a variety of reasons as to why this is much more problematic today:

-1. The amount outstanding is much higher than before.

-2. Student debt is at $1.36 trillion.

-3. There is no bankruptcy exit clause for student loans.

-4. Student loans are accessible to anyone and there is no clear education on the front-end as to what the true cost of borrowing will be. And this is for 17 and 18 year old “adults†who are likely making the biggest financial decision of their lives.

-5. A large portion of auto debt growth has come from subprime loans.

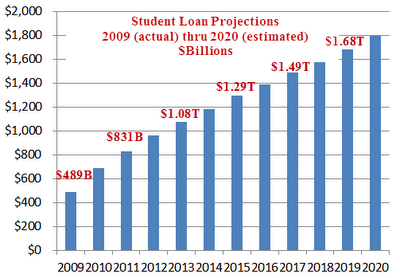

There is no slowing down the student debt juggernaut. If we continue down this path we are looking at $2 trillion in student debt outstanding by 2020:

If it is bad now, how will it be in the future? Income growth has to come in a meaningful way to justify current debt loads. Many are realizing that an expensive college degree is simply not worth it if your first job is in the low-wage sector of our economy. What this runaway debt expansion in auto loans and student debt suggests is that Americans are borrowing large amounts with the hopes of holding on to the dream of the middle class lifestyle. In reality, many are just assisting in building the twin trillion dollar towers of debt. People do realize our last crisis was largely brought on by people and banks taking on too much debt right?

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!Â

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! 4 Comments on this post

Trackbacks

-

generation welfare said:

a lot of these folks buyin new rides are on welfare,record numbers of folks on public assistance drivin new rides,malinvestment in it’s purest form

October 16th, 2015 at 4:07 pm -

Rascal said:

Just a war on the middle class like Lou Dobbs’ book said.

Sad thing is, people who were and are in the middle class don’t realize war has been declared. Until they do, they won’t understand what is happening to them. And that is just fine with the corporations that run this country. They are making billions in profits all while telling the lowly worker they need to take a cut in pay.

October 22nd, 2015 at 12:38 pm -

Rachel said:

First off, in response to “generation welfare” one cannot use welfare to purchase a car. Secondly, those who do not thoroughly investigate the benefits and drawbacks of the industry and their college major prior to committing to the expense of college bring their headaches and setbacks on themselves.

October 22nd, 2015 at 9:47 pm -

c said:

Loan originators no longer have to perform due diligence. It used to be if an originator made a bad decision on a creditor they would lose. Now with student loans and many other loans there is no recourse for the creditor, so the originators dont care who they lend to. More of the risk of making a bad decision should be on the loan originator.

It a way to put the pedal to the metal on borrowing.

Same thing with credit cards, anyone with a pulse can get one. Loan originator doesn’t care if they made a bad decision

October 23rd, 2015 at 5:47 pm