The Fed has built a financial pyramid based on unsustainable low rates. How the Fed is running out of economic curtains to hide behind when it comes to monetary policy.

- 3 Comment

The markets are pulling back dramatically because the Fed sneezed. The Fed essentially said they would begin tapering off their experiments in quantitative easing by pulling back their bond purchases from $85 billion a month to $65 billion. That is it. Not a shocking revelation. So why then are the markets plunging on this news? The entire market is being driven by artificial stimulus that is largely helping the top one percent in society. This is a primary reason on how we can have a peak in stocks while we have a peak in food stamp usage all at the same time. A large part of the recovery has been fabricated by giving banks access to trillions of dollars in easy debt via the monetizing machinery while the working public has to grovel for any crumbs that are left over after the banks have their feast. The Fed merely hinting at pulling back is slamming the market because many financial institutions gorging at the trough of low rates are sensing the 135 percent rally in stocks is coming to a close.

The financial market delusion

You can tell how delusional the market has become when you see ads like this:

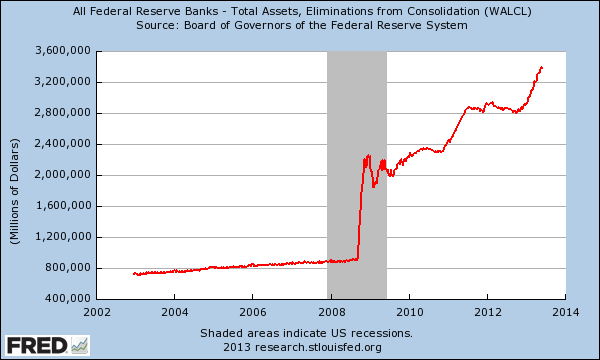

Dow at 60,000? Really? How is that going to happen when many working and middle class families are seeing their incomes decline? Most families do not have any sizable amount of money in the casino known as the stock market. The Fed has essentially monetized debt to an unprecedented degree and that is why their balance sheet looks like this:

$3.3 trillion. And this isn’t made up of clean securities but a mixture of oddities that banks have stuffed into the Fed as some kind of bad bank. Freeing up bank balance sheets has allowed these institutions to gamble once again in the stock market but also to crowd out regular families in the real estate game which used to be a relatively safe investment before the financialization of America took place as Wall Street has now swooped into markets in Arizona and Las Vegas creating another bubble in these and many other markets.

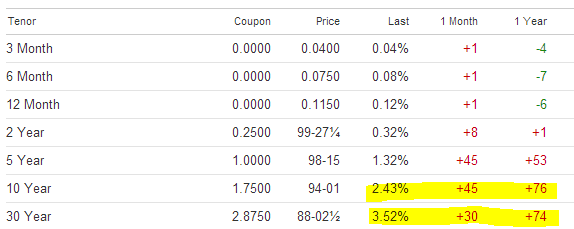

The bond markets of course have gone haywire with this minor announcement:

The problem with the Fed’s dance is that it needs to be an infinite dance. The entire pyramid was built on low rates. Any hint that rates will be rising will send ripples through this entire weak edifice. By the way, interest rates are still near historical lows yet the stock market is facing its first real shock in a long time because much of this system is built on perpetually low rates. Risk has been mispriced for many years.

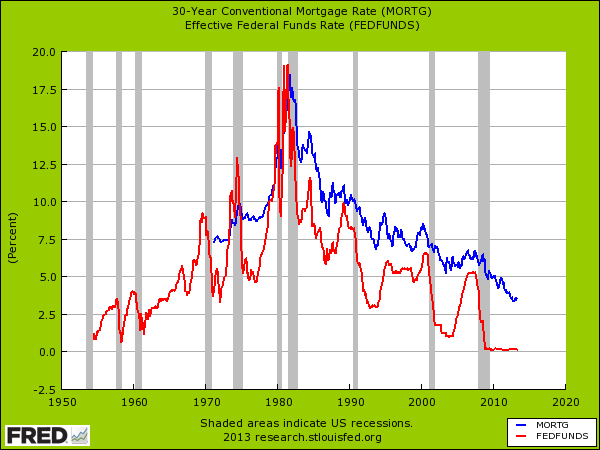

The Fed has been holding the Fed funds rate artificially low for many years. This combined with aggressive QE actions has pulled the 30 year fixed rate mortgage to all-time lows:

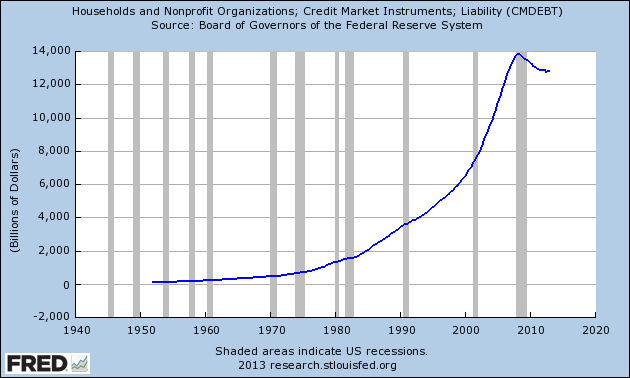

How sustainable was that? Well we are already seeing what happens when you build an entire financial pyramid on unsustainably low rates. It isn’t like the public has been benefitting from this either. Most Americans are still facing tight credit conditions as the deleveraging continues in the household sector:

All the while the Fed balloons their own balance sheet and gives easy access to banks. In a system where access to debt is wealth, those with political connections like the banks will win. The rush to convert debt into real assets has been happening for years now with Wall Street buying rental property, high priced homes in key locations, collectibles, and other items for the one percent. Yet this was done with the implicit backing of the Fed that with their actions has hurt the income growth of most Americans. In essence, the Fed has facilitated the biggest banking bailout in history with no vote in Congress.

Many think they can dance with the Fed on this poorly built pyramid. Many are now realizing that without low rates, the new financial paradigm is unsustainable.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!3 Comments on this post

Trackbacks

-

Ken Cherry said:

The 30 year Bull Market in bonds is over ! Wait till you see what happens to the stock market, profits, unemployment and world economies when rates “normalize” around 5% !

June 21st, 2013 at 4:40 pm -

The CURMUDGEON said:

We’ve been commenting on the reckless and destructive monetary policy all this year. Our last 2 posts document our argument with graphs and quotes from a Federal Reserve paper which mainstream media has ignored

How the Fed Starves the Economy While Inflating Assets

http://www.fiendbear.com/Curmudgeon34.htmFed’s QE Fattens Financial Markets, but the Economy Still Starves

http://www.fiendbear.com/Curmudgeon33.htmJune 22nd, 2013 at 5:45 pm -

john said:

The stimulus is no more “artificial” than the credit expansion during the boom times, or the equity bubble (which puts money into the economy) or the Reagan era debt spending. It’s real money in the economy.

The market burped on the news because they think a lot of the economy is just government spending and low rates driving up personal debt. While there’s a lot of truth to that, it’s probably not the whole truth.

June 23rd, 2013 at 10:34 pm