Inflation by any other name – Central banks around the world increase balance sheets from $2 trillion in 2008 to $6 trillion in 2013. The slow erosion of purchasing power in the US.

- 2 Comment

The Federal Reserve has been trying with all its power to stoke inflation. This is not the stated mission and you will not hear this proclaimed over loud speakers but if actions speak louder than words, this is the policy they are following. Yet the Fed is picking winners and losers with their inflation targeting. The reason the CPI for example is not reflecting major changes is the massive wealth destruction that has occurred in the debt markets, particularly with mortgages. In a system like our own, debt is money and there has been an enormous amount of debt that has been destroyed. Yet the Fed has aided the banking system by forcing rates lower and thus keeping asset prices higher for the mistakes taken on during the bubble years. This provides little support for working and middle class Americans. For example, this hurts fixed income savers including our rapidly aging older population. Also, even a modest amount of inflation is destructive should incomes remain stagnant.

Inflation is very high if incomes are stuck

We only experienced a brief bout of deflation in 2009 but since that point, inflation has been running at a steady clip:

People are so accustomed to inflation that they simply assume this is a naturally occurring process like the sun rising or the fall season. The reason inflation occurs is the money printing that happens in the background. Debt, or access to debt, is now a substitute for real money. With debt being harder to come by for average families, they have lost a source of money. This is why items that can be purchased with debt like a home or a college education now carry heavy premiums.

Since 2009 the annual CPI increases have been running around 2 percent. This might seem modest and nothing to fret about. Yet this is happening during a time when household incomes are stagnant. Given the massive amount of items that we import the impact is being seen from consumer goods, to food, housing, education, and healthcare. Yet when incomes are fixed, more and more money is consumed by the loss of purchasing power.

It would be one thing if this massive amount of central bank money printing were just common to the US but practically every major central bank around the world is following in the same footsteps:

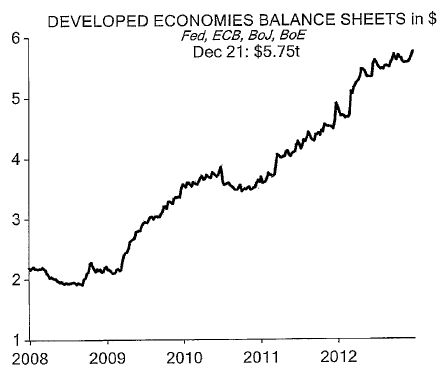

This is a very important chart. It includes the balance sheet of the following central banks:

The Federal Reserve

European Central Bank

Bank of Japan

Bank of England

What you see is that central banks around the world have increased their balance sheets from $2 trillion in 2008 to nearly $6 trillion today. There is little doubt what path central banks are following. While households are deleveraging (losing access to debt/spending power) central banks have ramped up to aid their member banks.

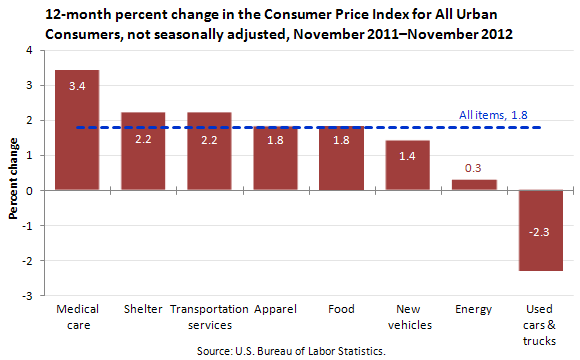

For most people it might be hard to see this in real daily terms. So let us examine inflation in a variety of sectors:

Take a look at what has been going up in price the fastest last year. The three sectors with the most inflation for the last year are medical care, shelter, and transportation. Food is also in the top five. These are all items that impact those on fixed incomes. And what about the 47 million Americans on food stamps? Any slight increase is going to take a deeper cut of the funds they are provided.

In the end, inflation is not a natural occurring event and even a little bit of inflation is problematic when incomes are stagnant.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!2 Comments on this post

Trackbacks

-

johnjasonchundotcom said:

Hard assets on American Soil, aka Oil, Gas, Coal, Minerals, Real Estate, Some Stocks, ETF’s (not bonds, options, futures, options or currencies) & Corporate shares will also hold up while “money shrinks” in purchasing power. This is the same cycle that has been “normal” from WW2. Aka 7-12 years up & 7-12 years down.

January 9th, 2013 at 8:03 am -

therooster of Christ said:

Inflation is “the stick” that’s employed by the “necessary evils” as the marketplace (you and me) gets slowly pushed to the market monetization of real-time bullion-as-money. Monetization of bullion as liquid currency must come from the grass roots, bottom-up for the sake of a comfortable rate of change from a debt paradigm to an asset-money paradigm …. in real-time. You cannot pour new wine into old wineskins.

January 9th, 2013 at 3:37 pm