What goes up, must come down: The façade of the current stock market rally.

- 2 Comment

Do you remember what you had for lunch yesterday? Probably. What about two weeks ago? Probably not. Our mind isn’t designed on remembering every single detail of every single event but has adapted itself into remembering important events. Our brain is designed to look forward and for the most part is resilient. This is why the stock market rally starting in 2009 has washed away the memories of the market crashing down for many people. This also gives us a financial blind spot. The stock market has had a nice run since 2009 rising 168 percent as measured by the S&P 500. Many of the reasons for the crash were never fully addressed including too big to fail, debt strapped consumers, and a national debt that is getting to a level that is simply unsupportable. This market rally has occurred under the guise of favorable policies to the banking system. The Fed has punished savers and has created massive incentives for large pools of money to flood into every corner of the economy including the real estate sector. This has crowded out many regular households.  Yet the stock market is turning and a modest correction is coming over the horizon. I have seen no articles that give a clear reason as to why the stock market should be up 168 percent in five years despite the underlying weakness in the economy.

The rally and the coming correction

The rally since 2009 has been pushed by a few key areas:

-1. Fed banking policies

-2. Ignoring common accounting rules

-3. Cutting wages

-4. Slashing benefits

-5. Increased productivity

A few of these items are already maxed out. The Fed’s QE programs are already reaching the end of their rope. The bond market is already pricing in a taper to QE. Wage cutting has already impacted the bottom line of the American consumer. Gains in productivity have not trickled down to the balance sheet of most Americans. In the end this rally has been about generous banking policy and basically cutting fixed expenses in a time of economic uncertainty. Corporate welfare and austerity for the public. Take a look at the stock market:

The market is up 168 percent from the low reached in 2009. What is surprising is that we have yet to have a modest correction of say 20 percent during this time. It isn’t a prerequisite to have a strong rally with no modest corrections. Yet this rally has been juiced by the Fed. Every time the market seemed to be entering a correction phase the Fed entered with QE or some of other banking stimulus.  In other words market participants almost expected the Fed to step in at any sign of a modest correction. With the Fed now having a stronger commitment to tapering what is the next move to keep this rally going?

Year to date the S&P 500 is down 1.77 percent. The Nikkei is down 15 percent. Corn is up 18 percent and gold is up 9 percent. We are getting into mid-April and the market is looking weak.

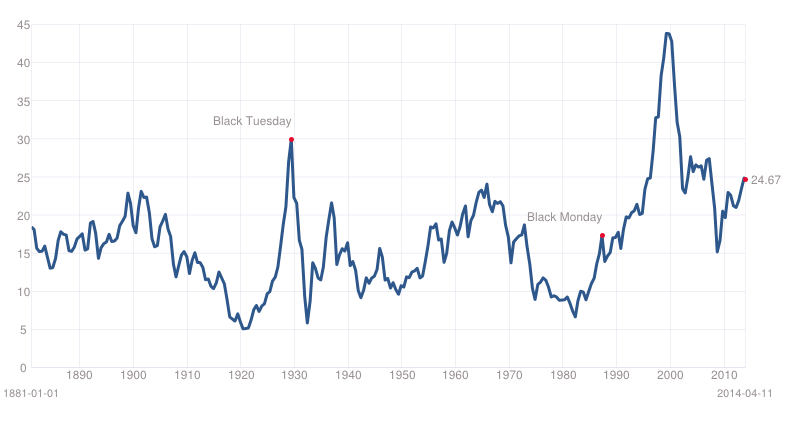

The Shiller PE ratio for the S&P 500 is at 24.67. The mean going back to 1881 is 16.52. We are due for a correction. Stocks are overvalued based on their earnings. This rally has largely been one of banks feeding into the whims of the financial sector followed by the financial sector plowing digital money and debt back into stocks, real estate, and anything that has a better chance of doing well instead of a dollar that is being devalued.

Here is how the Shiller PE ratio on the S&P 500 looks:

We are due for at least a 20 percent correction. Cash strapped Americans are still running on fumes. Debt growth is largely going into autos and student debt. What usually goes up has to come down. It would be one story if wages were rising nicely and consumer spending was occurring because of natural growth in household disposable income. That isn’t the case. This is a digitally printed banking rally. It is hard to see how we don’t escape a strong correction this year as the markets wakeup to the unsustainable nature of the current rally.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!   Â

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!    If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

2 Comments on this post

Trackbacks

-

Walter Ruggieri said:

The valuation in stocks does not reflect the reality in the rest of the economy. Thus, the current value can’t be sustained. So I agree that we are due some kind of correction. Will it be a dip (0-10%)? Will it be a correction (10-20%)? Or will it be a panic and a crash?

April 13th, 2014 at 1:04 pm -

Chris said:

stocks rising and rising actually makes sense…think about these factors…

1- corporations are borrowing at next to nothing to buy their own stock and are doing so well in excess of new issuance (shrinking outstanding float in excess of $1T)

2- Fed loans money for nothing to PD’s who buy T’s and then Fed buys back T’s removing $2.5T of Note/Bond assets but leaving all the new cash in need of a leveraged home somewhere.

3- Foreign CB’s appear to also have purchased $4T since ’09 in Notes/Bonds US Treasury removing an entire asset class…

4- US institutions (ex-Fed) have not added to their holding of US Notes/Bonds since ’00 (maintaining about $2T) while Fed and Foreigners bought all new issuance.

This simply means there are lots of new dollars and increasingly fewer assets with which to choose from.

April 15th, 2014 at 10:54 am