Saving Nation: You Know you Have a Fiscal Problem When Saving Money Actually Becomes a Detriment to the Health of our Economy.

- 2 Comment

In George Orwell’s dystopian 1984, doublethink was the ability for someone to hold two mutually contradictory beliefs, and accepting them both. We have now entered into the world when Americans actually saving money is bad for the health of our consumption economy. War is peace. Saving is spending. Our Ministry of Truth is the Federal Reserve and U.S. Treasury telling us that going into debt and devaluing our U.S. dollar is actually good for the health of our country. The only minor caveat is that it is good for a very small section of our country in particular the crew on Wall Street Oceania.

It is hard to utter the following phrase because we haven’t heard it in so long. Americans are abruptly spending less than they earn. As I’ve talked about before with U.S. Savings Bonds the U.S. government is purposely trying to keep you from saving. This is simply one piece of the puzzle but in the middle of 2008, the U.S. Treasury suddenly lowered the ceiling of how much money could be invested in U.S. Savings I-Bonds for each calendar year from $30,000 to $5,000. That is incredibly steep. It isn’t like I-Bonds were garnering 11 percent year over year returns like Bernard Madoff but they were simply keeping pace with inflation. In fact, with the current CPI readings, I-Bonds will probably be yielding 1 to 2 percent on the next readjustment since they adjust bi-annually. My point is, our government is really trying to encourage people to spend beyond their means.

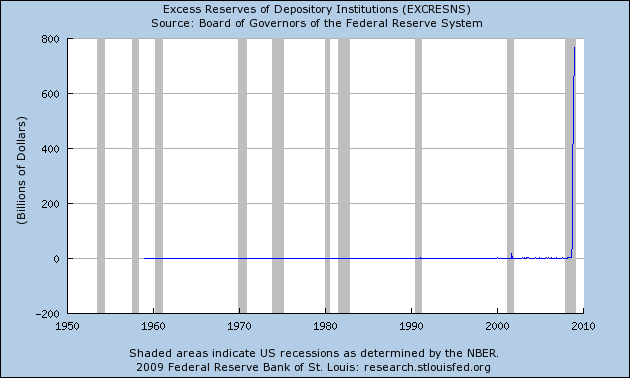

Just think about the entire concept of the Troubled Asset Relief Program (TARP). The first tranche of $350 billion was funneled to banks to help their capital ratios to encourage lending. None of this happened. In fact, banks merely hoarded the money:

So what is happening is banks are simply not lending money. This is the doublethink world we live in now. We are expected to believe that giving money to banks, banks who are part of the reasons for this economic crisis, is going to actually help us in the long run. The problem with TARP is there is no clear objective. First, it was slated as a method of purchasing bad assets from the housing collapse. Next, it morphed into the U.S. taking a stake in many large banks. The last morsel was given to the U.S. auto industry. Now, we are back to square one with the TARP. Another $350 billion but no clear idea of how we are going to spend it since the first tranche was squandered and as you can see above, is simply sitting idly in excess reserves.

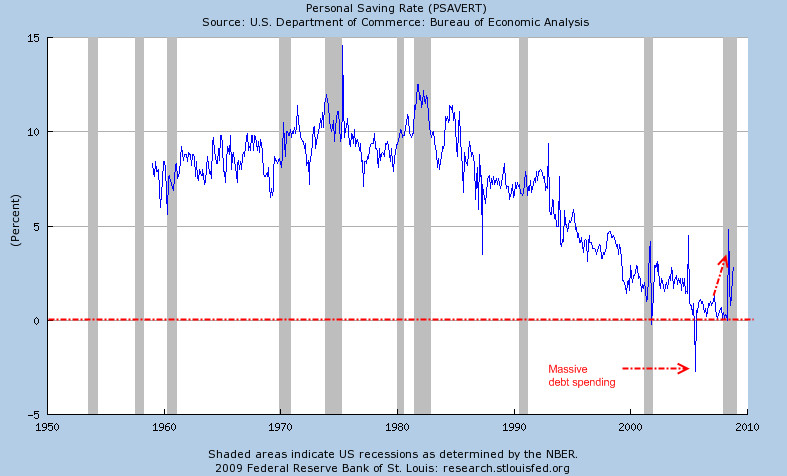

The savings rate for November spiked 2.8 percent. This is up from the amazing zero at the start of 2008. Here is a chart of the savings rate:

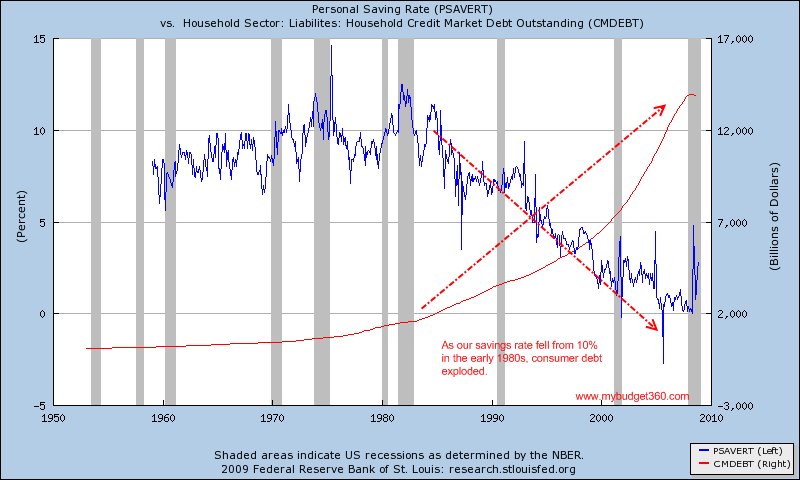

This decade we actually went negative for the first time since data started being gathered in 1959. This is a reason why this recession is already giving us signs that it will be the most prolonged recession since World War II. Many Americans have no buffer of savings to protect them from a job loss. That is why many states are seeing their unemployment insurance funds being depleted at astronomical rates. But let us show this chart with the expansion of debt over this same time:

This also coincides with my analysis that the roots of the housing bubble started way back 30 years ago. It started back then because this is the tipping point where Americans not only became comfortable with debt, but they started confusing debt with wealth. Unfortunately our Federal Reserve and U.S. Treasury are making this same mistake spending money we don’t have on bailing out banks and other projects that will simply harm our country in the long run.

The fact that over two-thirds of our economy is based on consumption does not bode well. In fact, we are now in a debt unraveling spiral. Take a look at the bankruptcy of Circuit City:

“NEW YORK (CNNMoney.com) — Bankrupt electronics retailer Circuit City Inc. said Friday it will close its remaining 567 U.S. stores and sell all its merchandise.

The company said it has 34,000 employees.

The company said the sale would begin Saturday and run until March 31, pending court approval.

The retailer’s Web site and call center will cease to operate after Jan. 18.

Circuit City said employees will receive 60 days notice of the termination.

Employees who are laid off earlier will get pay and benefits for the 60-day period beginning Friday, the retailer said.”

So here is the 1984 scenario at hand. Fundamentally saving money is good for you individually. But the fact that you are not blowing money on plasma TVs or new surround sound systems will cost 34,000 employees their jobs. These people will not be able to spend at local restaurants, will have a harder time making their bills, and ultimately have a hard time coping in this environment. This isn’t to say you should go out and spend but this shows the tragedy which our government has set us up with when they proclaimed 30 years ago that deficits don’t matter.

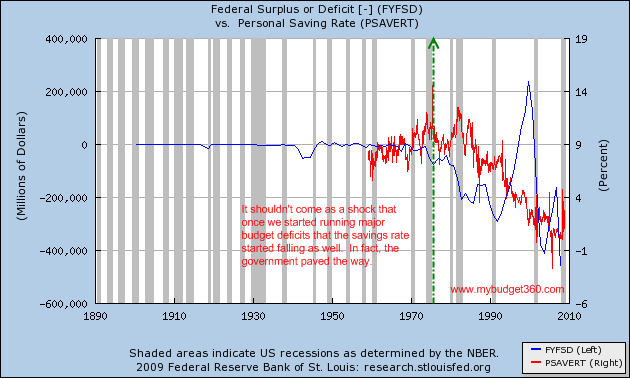

They do because now, we are big borrowers from Japan and China and they will not be content keeping our gig going when their countries are accumulating savings with a growing middle class that wants to see their homegrown currency appreciate. If you don’t think this 30 year debt mindset is correct, let us look at our federal surplus or deficit:

This is why history is so important. What we’ve been living in is a debt induced hyper charged economy that has saddled our nation with $49 trillion in various forms of debt. And this debt will be growing with more TARP spending, further bailouts, and major fiscal stimulus. This is money we do not have. We are now relying much too heavily on foreign nations to keep our spending going. In this case however, Americans are being forced to save and this is the only way to correct our damaged balance sheet. The government looks to be spending more than we have for the foreseeable future. If our foreign borrowers get tired with low rates, there will be economic havoc and a run on the U.S. dollar isn’t completely out of the question.

On an individual level, you should save. We can’t speak for everyone but it is time to get our budget in order and protect what has made this country strong. I doubt that any of us believes that one of our inalienable rights is to spend beyond our means.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!2 Comments on this post

Trackbacks

-

The trueth said:

Great article

December 25th, 2016 at 10:42 am -

The trueth said:

The elites and billions want every last penny for themselves, and they want the masses on their knees.

So far they been winning hands down.

So far its been a class war like a baby fighting godzilla. Not much of a fight.

December 25th, 2016 at 4:20 pm