Bankrupt Consumer: Chapter 7 Bankruptcies up. Credit Card and Consumer Credit Crisis: Americans were Using Consumer Credit as a Lifeline and it is now drying Up Pushing Bankruptcies Upward. $2.5 Trillion in Loans at Risk.

- 5 Comment

Credit cards have been around for many years with Bank of America creating the BankAmericard in 1958, which eventually evolved into the modern day Visa system. MasterCard has been around since 1966 and received significant backing from Citibank. These names are familiar with the current credit crisis. Credit cards have been one component of the approximately $50 trillion in debt we have as Americans. Now credit by itself isn’t necessarily an evil. Initially, credit was given to those who had the 3 C’s; capacity, character, and collateral.

Capacity meant you had the means to pay the loan back. Character meant a lender usually vouched for your habits and economic lifestyle as a good credit risk. Finally, collateral meant that whatever the loan was secured to would ideally hold its value should you default on the loan. Yet in our current crisis, all these 3 areas were completely ignored. First, capacity was never examined. Just think of the no-doc no-income loans made to borrowers who never had a chance of paying a mortgage back. Character was never really examined as well. In fact, think of all those multiple credit card offers you get in the mail. Do you really think American Express, Chase, Citi, or any other major credit issuer really knows your character? And collateral was essentially made up. Just think of the global housing bubble and you’ll realize that creditors now have collateral that isn’t worth the loan amount.

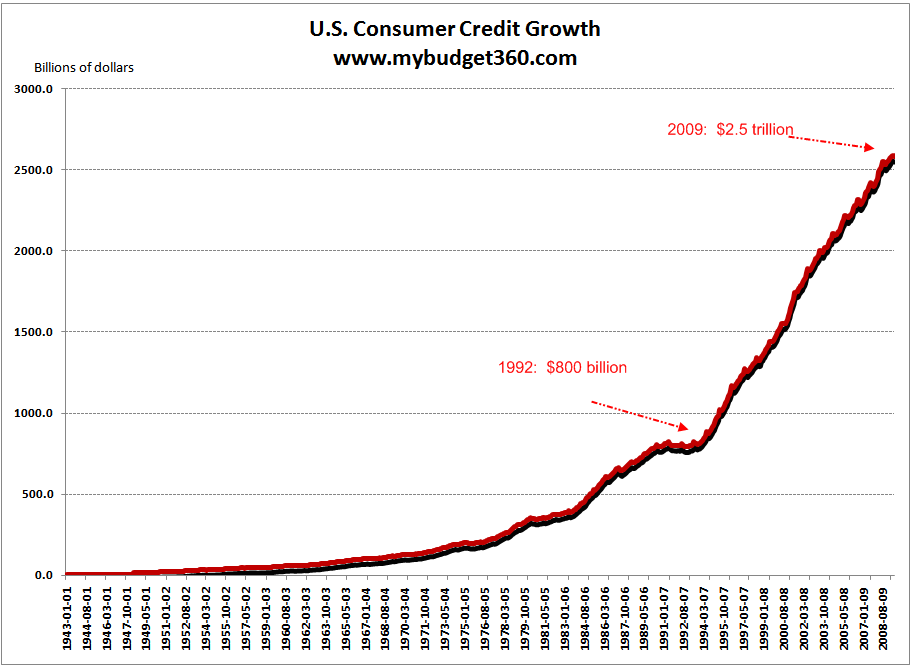

In this article, we are going to focus on consumer debt. We won’t focus on mortgage debt since we have already discussed that at great length in a couple of articles. It is also the case that much of the focus has been on the housing market and the credit markets that relate to that area. But not much has been devoted to the credit card and installment loan markets. First, let us look at the size of this market:

The massive growth in consumer credit is astounding. Since 1992, consumer credit has grown by $1.7 trillion. This stunning number is even more breathtaking when you realize that most of this current decade, Americans have seen stagnant wage growth. This chart really highlights the reliance on credit via credit cards and loans to keep our economy humming. Let us be more precise with the numbers:

American Households:Â Â Â Â Â Â Â Â Â Â Â 112,377,977

Credit Card Debt:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $973 billion

Non-revolving loans:Â Â Â Â Â Â Â Â Â Â Â Â Â Â $1.59 trillion

Credit Card debt average per household:Â Â Â Â Â Â $8,658

Total consumer debt per household:Â Â Â Â Â Â Â Â Â Â Â Â Â Â $14,148

Of course, not all households have credit card debt or installment debt so keep that in mind. Even if you have zero credit card debt and no installment loans, this is the average if all the debt was disbursed evenly across American households. Installment loans include auto loans, mobile home notes, and education loans and that is partly why the amount is larger. Yet the amount of credit card debt is staggering. However, it is interesting to note that actual credit card debt has contracted in recent months:

The contraction is rather significant and shows that households are simply reaching a peak in their borrowing capabilities. Remember the 3 C’s above? Now credit issuers are being more diligent and actually using these criteria and as it turns out, the balance sheet of many Americans is deeply in debt. To a certain extent, this was encouraged by a government channeled by the Fed and U.S. Treasury who have been for decades trying to discourage Americans from saving. The game is quickly coming to a stop here.

Some of the average debt amounts are astounding. Take a look at the terms for the average car loan:

Interest rate:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â 6.43%

Maturity in months:Â Â Â Â Â Â Â Â Â Â Â Â 63.2 months

Loan-to-value ratio:Â Â Â Â Â Â Â Â Â Â Â Â 88

Amount financed:Â Â Â Â Â Â Â Â Â Â Â Â Â Â Â $25,041

Interestingly enough, in 2003 the interest rate was 3.81% and the loan-to-value was 95 percent. What this means is we had an automobile bubble as well. With low rates, little down, and massive demand the cost of cars went through the roof spurred by easy access to installment loans. Now, with automakers suffering the price of cars will be falling just like that of homes. All of this was fueled by easy credit and without access to credit, prices will have to come down to more stable levels that reflect the balance sheet of the average American family.

The average interest rate on credit cards is 13.36%. If you are looking for a guaranteed investment let me tell you what to do. Pay off your credit cards if you can! Even Ponzi expert Bernard Madoff was pumping a steady rate of 11% so 13% is should be obvious. If you are worried about the stock market and have credit card debt, just pay off your debt.  It’ll give you a much bigger assured return. In addition, now that we are facing the menace of deflation debt is your worst enemy.

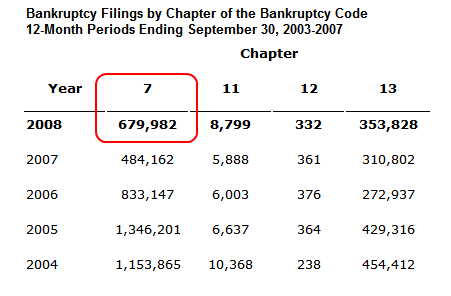

The major holders of credit card debt are commercial banks. They hold $376 billion of credit card debt on their books. But you’ll be surprised that $449 billion is in pools that are securitized assets. So once again, with the rise of bankruptcies we are going to see the same issues with mortgages. That is, it is hard to tell who is the ultimate holder of the note since it has been sliced and diced so many times it is difficult to distinguish true ownership. Yet the thing with credit card debt is that it is easier to get rid of in bankruptcy:

Bankruptcy cases filed in federal courts totaled 1,042,993 for the 1-year period ending on September 30, 2008. This is a 30 percent increase from the last fiscal year ending in 2007 where only 801,269 cases were filed. What is more troubling is the rise of Chapter 7 bankruptcies which are liquidations (instead of Chapter 13 reorganizations):

Expect this number to explode in 2009 with the amount of debt outstanding and the housing market continuing to deteriorate. The reason the number has been lower is possibly that consumers have been relying on installment and credit card debt to stay afloat for the last few years. Now, that is ending and with that, more bankruptcies will inevitably occur.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market! If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!5 Comments on this post

Trackbacks

-

Jimbo said:

We are in very serious troubles.

January 21st, 2009 at 9:52 am -

Marge said:

If greed, listed as one of the seven deadly sins, was punishable by immediate death, we’d have no rich folks left in this country…

January 22nd, 2009 at 9:18 am -

Gloria said:

WELCOME BACK TO THE PIONEER DAYS! ARE YOU READY?

January 22nd, 2009 at 4:52 pm -

Kashyap said:

Could you please cite the data source for the last table (Bankruptancy filing by chapter)?

January 28th, 2009 at 5:09 pm -

matthew demaria said:

I am doing some research for something concerning the mortgage industry and part of it is using overall debt for consumers on a monthly basis. Where did you obtain the information for the car payments, etc? Hopefully your data source has a breakdown of each type of debt etc.

thanks

matt

February 19th, 2009 at 7:46 pm