Commercial Real Estate Reality Check: 2007 Commercial Real Estate Valued at $6.5 Trillion with $3.5 trillion loans. Today, Commercial Real Estate Valued at $3.5 Trillion with $3.5 Trillion in Loans. Can you spot the Problem?

- 4 Comment

Commercial real estate is dealing with the neutron bomb effect. The buildings still stand but the inside is gutted as if vultures had devoured a carcass. What we are seeing, like in many other sectors of our economy, is a distinction between reality based economics and the inflated prices of Wall Street. If we look at the stock market, you wouldn’t know that people are lining up at Wal-Mart at midnight at the end of the month waiting for paychecks or government assistance to clear simply to buy food. You also wouldn’t know that 27 million people are either unemployed or underemployed. The irony of this is banks do know how bad the economy really is including the disaster that is commercial real estate. Banks are building up reserves to brace for what is going to be a long and hard road ahead.

To understand commercial real estate, we first have to see the actual damage. In 2007, commercial real estate values came in at approximately $6.5 trillion backed by $3.5 trillion in loans. Today, the $3.5 trillion in loans are still on the books, but the values have fallen to about $3.575 trillion. This is how it looks:

We should spend some time examining the chart above because $3 trillion in supposed equity has vanished. As we now know, banks had questionable valuations on properties during the peak bubble years. Most realize that if they had to mark to market the properties, they would yield 40 to 50 percent less if they are lucky. Banks would like to play this game that all is fine but if all is fine, why don’t they liquidate the properties? They won’t because they would have to realize the loss. So instead, the U.S. Treasury and the Federal Reserve are monetizing this excessive debt and are going to destroy the U.S. dollar. This is the bet. They think, that at some point values will once again reach those peak valuations. How will that happen? Ideally through controlled inflation. But this isn’t a guarantee. If we face true demographic shifts in our nation and the baby boomer wave is one, then we may never see those peak valuations again. What will happen is the average American is going to see a weaker currency and wonder why their once stronger dollar is so weak. The reason for this is the Fed and U.S. Treasury have decide to bailout the entire banking industry on the backs of the average American with no benefit to them.

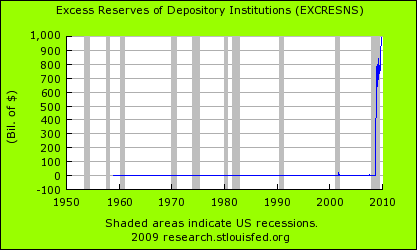

Walk through the logic however. The pretense of all the bailouts has been that financial Armageddon would hit if the banks didn’t get exactly what they wanted and no loans would be made. The actual destruction was really just with the banks because our economy is still hurting but apparently banks are back to record profits. Banks got their money yet loans are still hard to find for average Americans. Banks are holding back enormous reserves because in the reality based economy, they know that commercial real estate is imploding internally on their balance sheet. Take a look at the excess reserves at banks:

Banks are now holding roughly $1 trillion in excess reserves. This is up from $724 billion in March since the “recovery” has started. Do banks know something we don’t? Of course. They know that many of the commercial real estate borrowers are now insolvent. In many cases, banks are simply rolling over loans and giving six month extensions playing kick the can down the road. Why? Because banks can still claim high valuations even though the current borrower is basically a non-payer. This is the kind of game we are currently in. Commercial real estate is imploding on the balance sheet of banks. Banks and Wall Street have completely disconnected from economic reality that even SNL is cracking jokes about this.

In a recent Deutsche Bank presentation, the delinquency rate on commercial loans is at 4 percent. Deutsche Bank expects 70 percent of CRE loans to not qualify for refinancing. That comes out to about $2 trillion in commercial real estate that will mature from now until 2013.

The Fed through TALF has tried to take some of this debt out of the system but now their books are over burdened. Also, many of the commercial real estate loans are junior and don’t even qualify for TALF and these are the real problems. Either way, the reality of the situation is many of these commercial loans are now imploding and many banks are failing on Friday’s like flies running into the light. Unlike the residential real estate bubble, most commercial real estate loans are backed by shorter term financing that is based on 5 to 7 year terms. If prices have fallen by 40 to 45 percent, refinancing becomes impossible:

If we look at the above, some of the more distressed properties are down by a stunning 56 percent. In other words, banks are insolvent. Unlike the average American, they have Wall Street and the proxy of Wall Street, the U.S. government as their life line. While most Americans deal with the realities of a crashing economy via unemployment or disappearing wages, these banks are playing games with their balance sheet and claiming to put out wicked profits quarter after quarter. Where are these profits coming from? Well if you can claim that you have $6.5 trillion in CRE values when in reality, it is closer to $3.5 trillion then you are embellishing the books by $3 trillion. To be more concise, the banking sector is largely insolvent if it had to reflect reality. Instead, it is preparing for clandestine bailouts that will be shouldered by the American public.

The commercial real estate disaster reflects a deeper problem in our economy. The strip mall and perma-growth world. People started believing that we could basically cut each other’s hair and flip houses to one another and this was somehow a good diversified economy. As it turns out, we do need to make things. If you look at the recent CPI, rents have fallen by over 1 percent but food and other necessities have gone up. Imported items have also increased. Expect this to happen over and over.

The Fed is vigorously fighting any audit because we are going to see empty strip malls and failed condo projects on their books. Lender of last resort was probably not designed to bailout late night infomercial tanned gurus that bombed out on their dream of everyone owning a Florida condo. Is this really what our central bank has become?

And to highlight how good the economy is, foreclosures keep growing:

“(Yahoo!) About 4 million homeowners were either in foreclosure or at least three months behind on their mortgage payments as of September, according to the mortgage bankers group. Even if a quarter of those borrowers are able to stay in their homes, “there’s a lot of potential inventory coming into the market next year,” said Jay Brinkmann, chief economist with the Mortgage Bankers Association.”

Homeowners that can’t even pay their mortgage or find work are not going to be spending money. Condos, hotels, and reality based businesses are already seeing this play out but don’t look to Wall Street for what is really happening in our economy. That $3 trillion in CRE values is long gone like smoke in the wind.

If you enjoyed this post click here to subscribe to a complete feed and stay up to date with today’s challenging market!

{kind=link}

4 Comments on this post

Trackbacks

-

WT said:

throw the bums out mid election; the one’s who’ve allowed this distruction of our economy and theft of our hard earned savings.

November 21st, 2009 at 4:08 pm -

Mr Morphed said:

This looks like a hellova mess.. Max the credit cards, buy supplies and hold on.. Tell the banks you are taking your bailout and ..bailout. Don’t pay them back, put no trespassing signs up and tell the banks any collectors will be met by extreme force. It works for me, they will quit calling quickly if you let them know you are not to be messed with and when the collector asks for the money, turn the tables and ask them how they can justify working for the monsters they do.

November 22nd, 2009 at 11:23 am -

salome said:

morphed—i love it ! tell the banks you’re takin’ your bailout–lol !

but same as yerself and common sense—stock up on what you CAN,little by little –get together with like minded folk,network,pay attention and pray.

aaaaaand of course get viable candidates petitioned/on the ballots and vote THEM ALL out 2010–yeah,all of them–WHY are they wasting our time with all this dimOgenic sheiss ? they constructed the fuel “shortage” and mortgage meltdown etc etc and now this bs for health “care”

what happened to the 47million shmoes that SUPPOSEDLY are uninsured…and sure—-billions to insure them aaaaaaaand it’s such a crisis and emergency that it doesn’t kick in till 2013???? right.

this is simply anothEr scam/slush fund.hey,with so many unemployed and needing to be kept occupied –this is a wonderful opportunity for many.

GOOD LUCK !November 22nd, 2009 at 8:34 pm -

Terry said:

The US economy will be spiraling out of control in the coming months and will reach critical point by the end of the 1st quarter 2010 and implode by the 2nd quarter.

The truckload trillions, “aka dollars stimulus” has failed to turn the economy around. We’ve come to a tipping point and the economic patient is about to flat line. I hear a code blue…

There will be the greater wave of foreclosures in residential and more importantly commercial properties by the end of December and early 2010. All of these foreclosures will accelerate price deflation once they come through the pipe. Commercial property values will continue to decline and the balance sheets of banks will continue to erode.

Given the above situation, will the Fed continue to buy mortgage-backed securities to prop up the markets? The Fed has already spent trillions buying toxic mortgages with no potential buyers in sight. Will the Fed continue to pursue buying mortgage backed securities? How about the CMBS market? The Fed’s balance sheet is more toxic than the “too big to fail†banks that it rescued.

There are no green shoots and it doesn’t make any sense to assert that the worst is over and that we are on the road to recovery.

November 24th, 2009 at 8:53 am